Academic Profile

Statistics

Similar Authors

Papers on arXiv

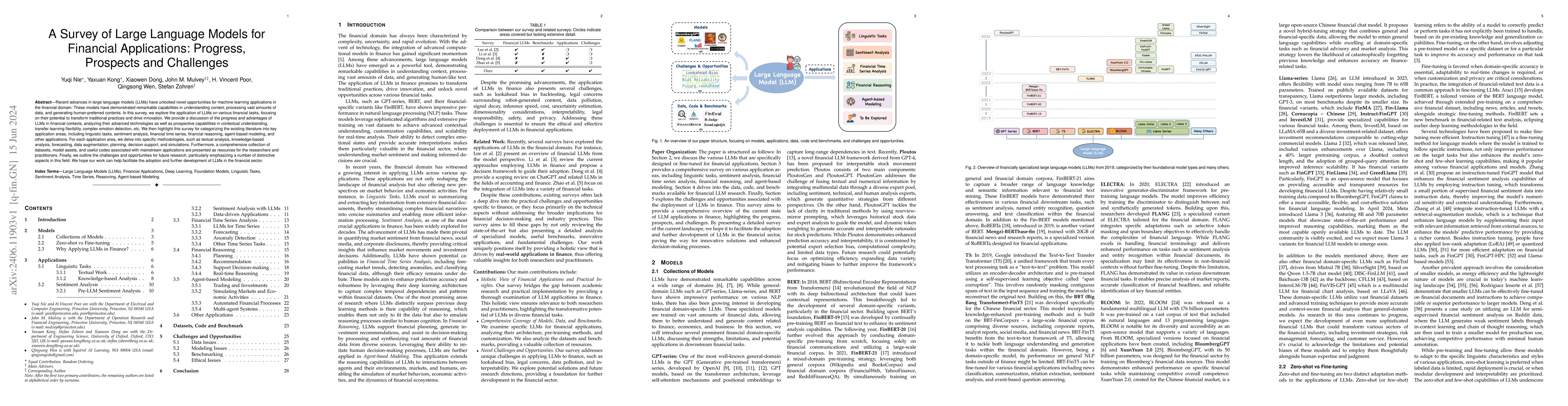

Recent advances in large language models (LLMs) have unlocked novel opportunities for machine learning applications in the financial domain. These models have demonstrated remarkable capabilities in...

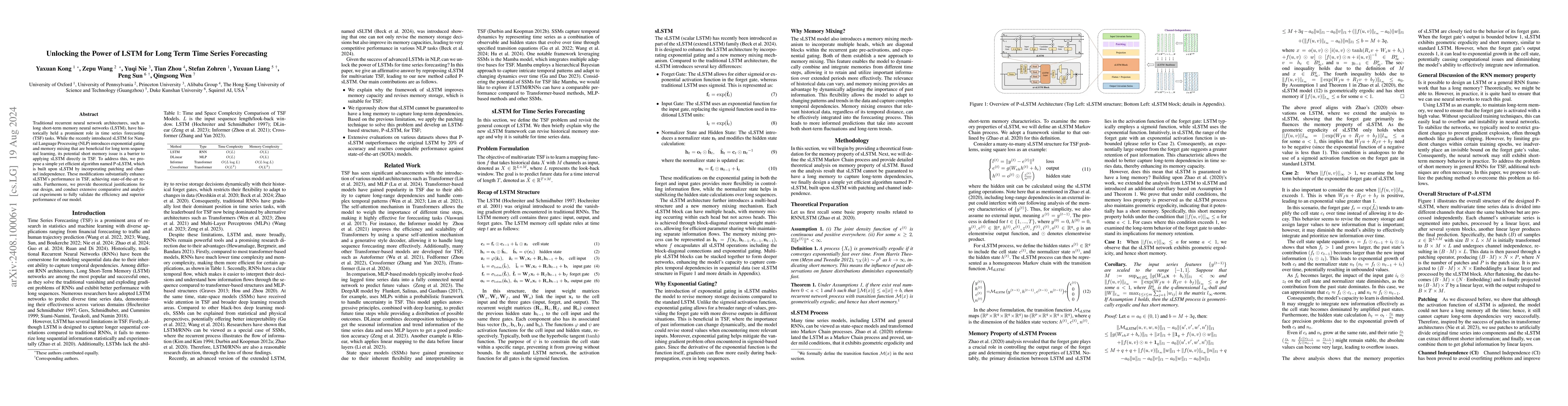

Traditional recurrent neural network architectures, such as long short-term memory neural networks (LSTM), have historically held a prominent role in time series forecasting (TSF) tasks. While the rec...

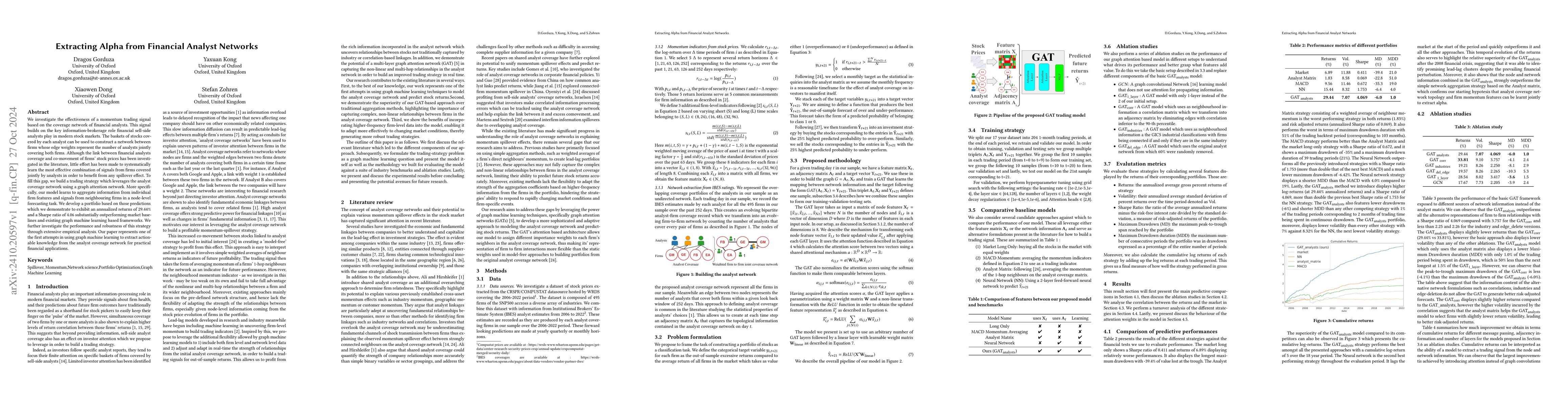

We investigate the effectiveness of a momentum trading signal based on the coverage network of financial analysts. This signal builds on the key information-brokerage role financial sell-side analysts...

This paper addresses the critical disconnect between prediction and decision quality in portfolio optimization by integrating Large Language Models (LLMs) with decision-focused learning. We demonstrat...

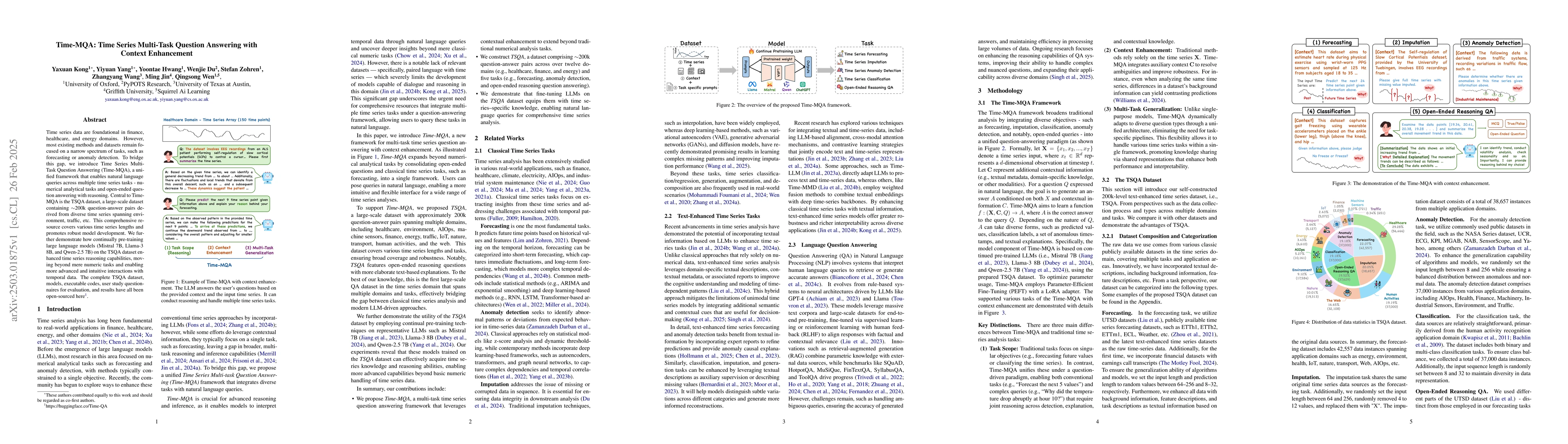

Time series data are foundational in finance, healthcare, and energy domains. However, most existing methods and datasets remain focused on a narrow spectrum of tasks, such as forecasting or anomaly d...

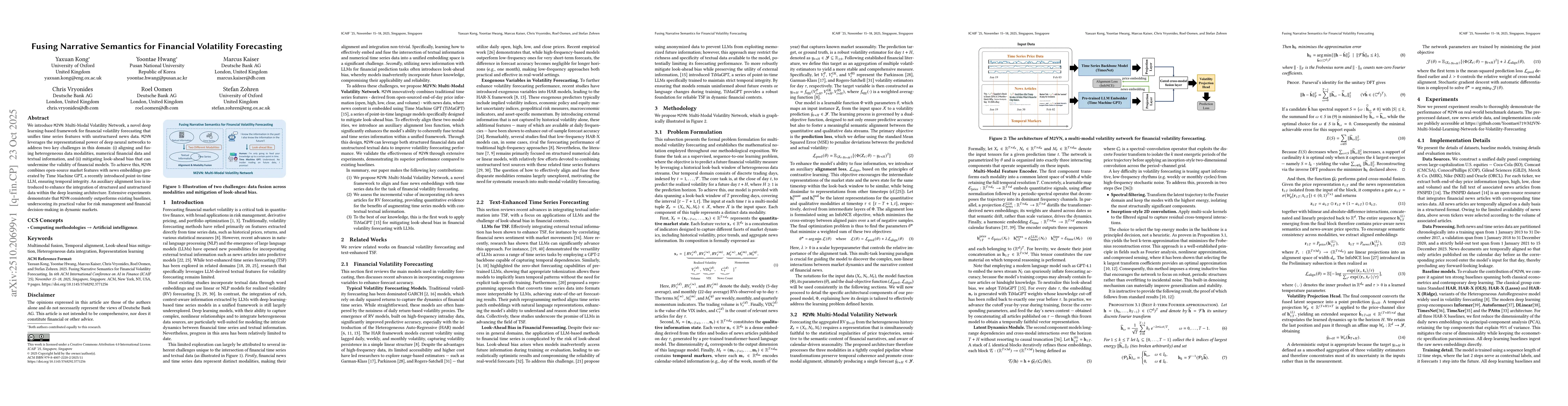

We introduce M2VN: Multi-Modal Volatility Network, a novel deep learning-based framework for financial volatility forecasting that unifies time series features with unstructured news data. M2VN levera...

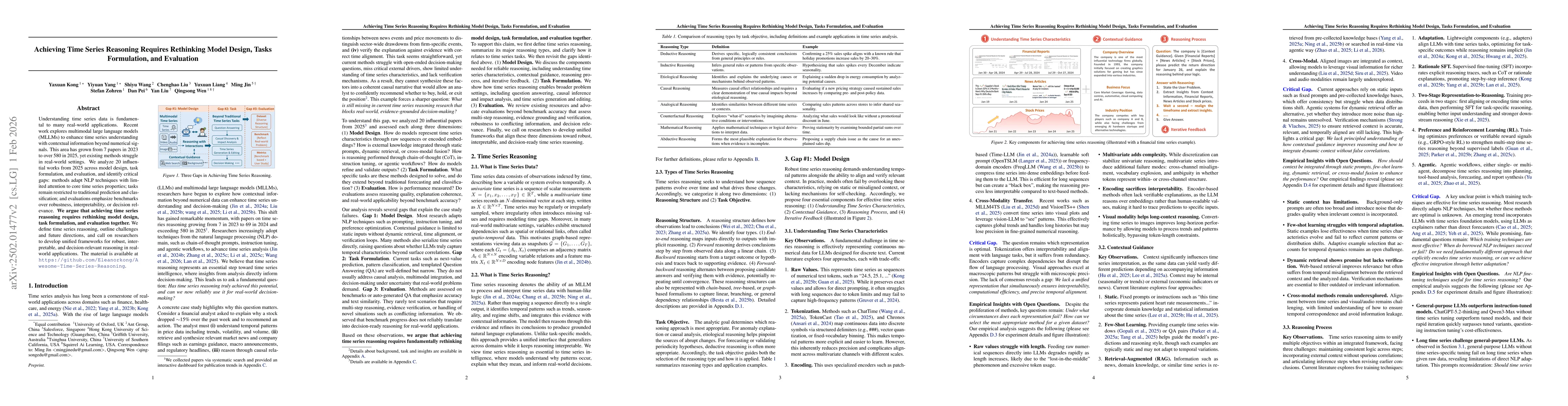

Understanding time series data is fundamental to many real-world applications. Recent work explores multimodal large language models (MLLMs) to enhance time series understanding with contextual inform...

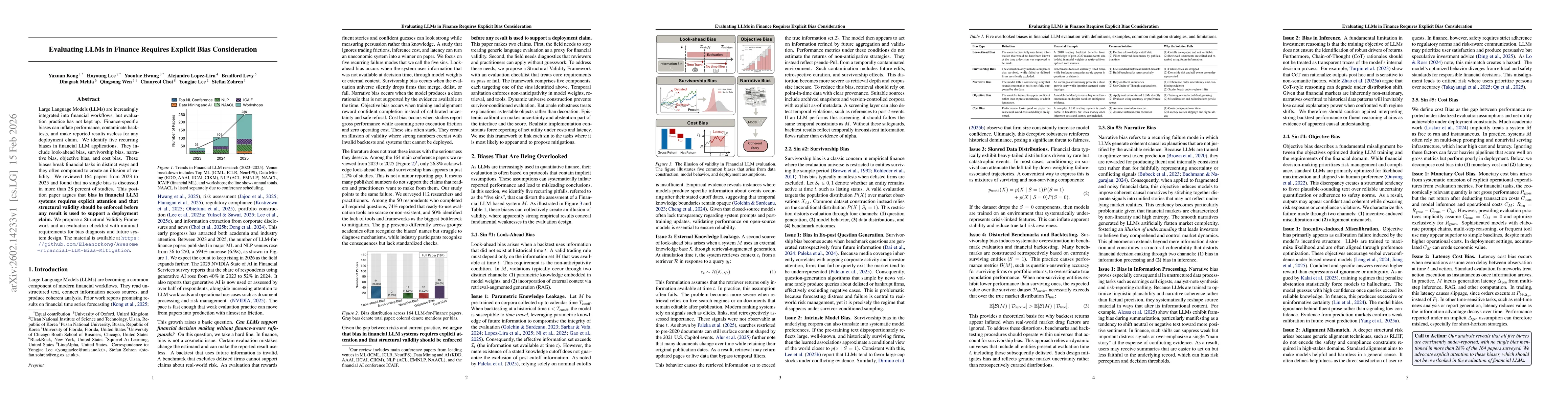

Large Language Models (LLMs) are increasingly integrated into financial workflows, but evaluation practice has not kept up. Finance-specific biases can inflate performance, contaminate backtests, and ...

Time series data inform critical decisions across many real-world domains. While large language model (LLM) agents can analyze data through natural language and tools, it remains unclear whether they ...