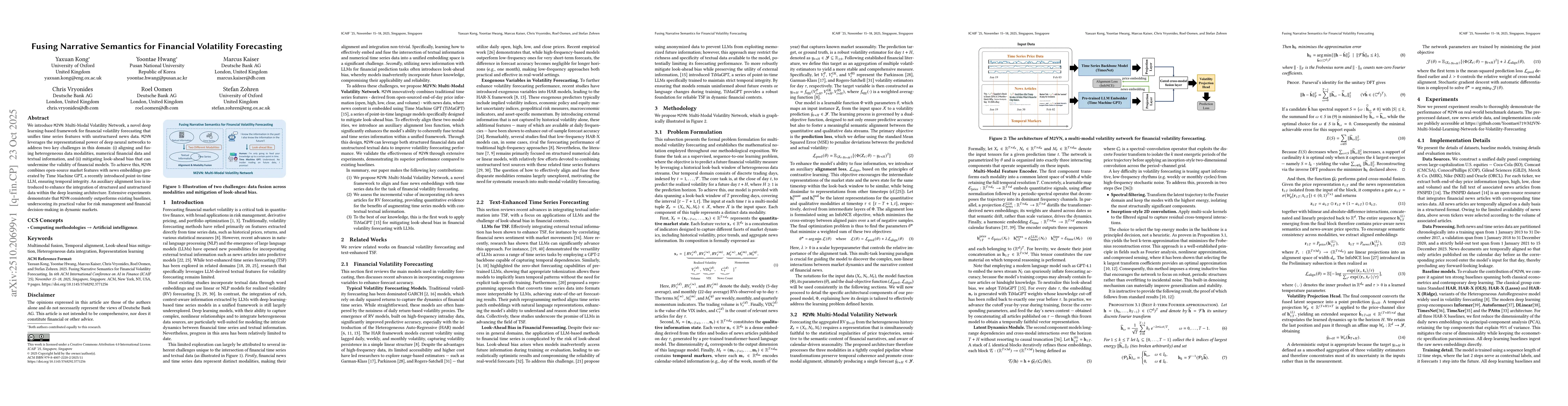

We introduce M2VN: Multi-Modal Volatility Network, a novel deep

learning-based framework for financial volatility forecasting that unifies time

series features with unstructured news data. M2VN leverages the

representational power of deep neural networks to address two key challenges in

this domain: (i) aligning and fusing heterogeneous data modalities, numerical

financial data and textual information, and (ii) mitigating look-ahead bias

that can undermine the validity of financial models. To achieve this, M2VN

combines open-source market features with news embeddings generated by Time

Machine GPT, a recently introduced point-in-time LLM, ensuring temporal

integrity. An auxiliary alignment loss is introduced to enhance the integration

of structured and unstructured data within the deep learning architecture.

Extensive experiments demonstrate that M2VN consistently outperforms existing

baselines, underscoring its practical value for risk management and financial

decision-making in dynamic markets.

Discussion 0