Academic Profile

Statistics

Similar Authors

Papers on arXiv

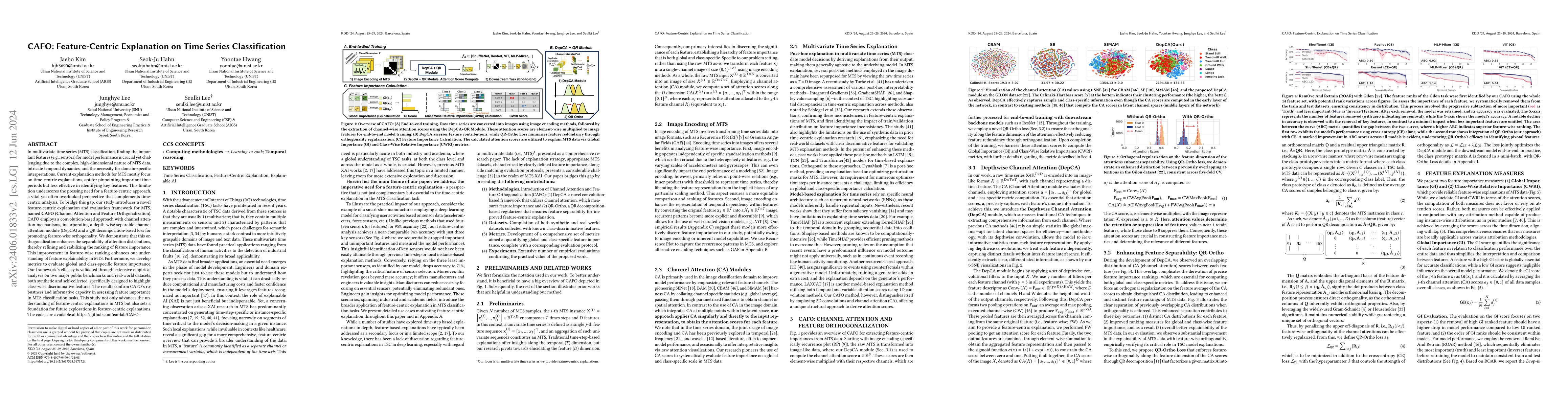

In multivariate time series (MTS) classification, finding the important features (e.g., sensors) for model performance is crucial yet challenging due to the complex, high-dimensional nature of MTS d...

In the era of rapid globalization and digitalization, accurate identification of similar stocks has become increasingly challenging due to the non-stationary nature of financial markets and the ambigu...

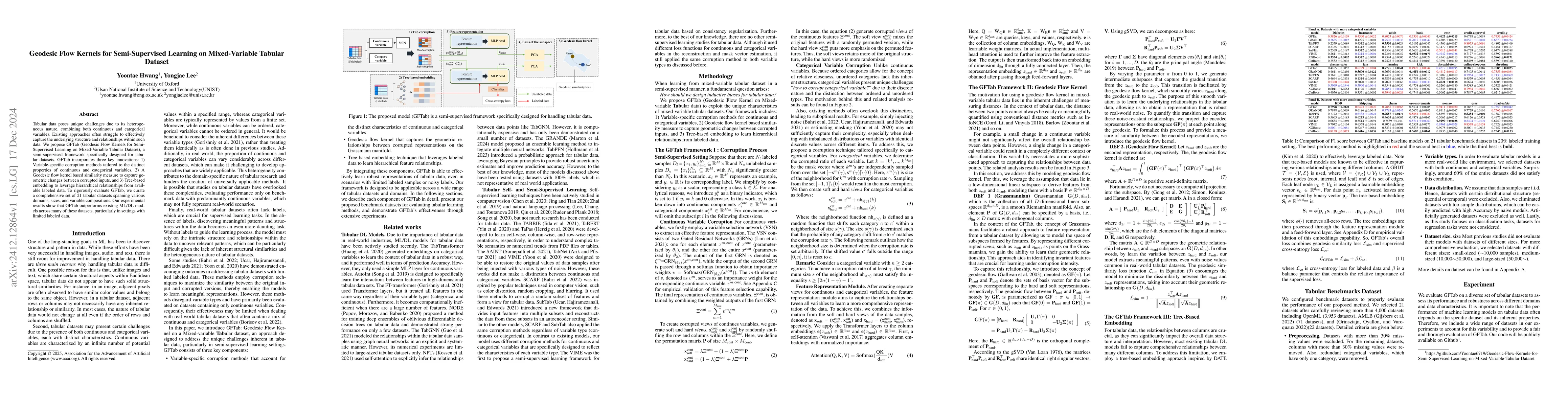

Tabular data poses unique challenges due to its heterogeneous nature, combining both continuous and categorical variables. Existing approaches often struggle to effectively capture the underlying stru...

This paper addresses the critical disconnect between prediction and decision quality in portfolio optimization by integrating Large Language Models (LLMs) with decision-focused learning. We demonstrat...

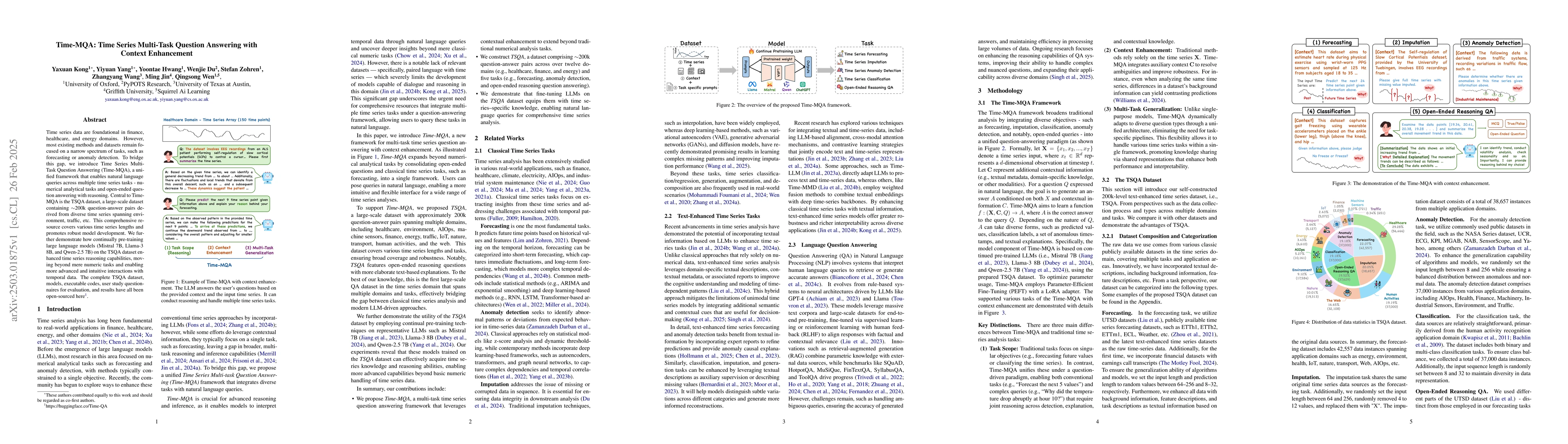

Time series data are foundational in finance, healthcare, and energy domains. However, most existing methods and datasets remain focused on a narrow spectrum of tasks, such as forecasting or anomaly d...

Robust asset allocation is a key challenge in quantitative finance, where deep-learning forecasters often fail due to objective mismatch and error amplification. We introduce the Signature-Informed Tr...

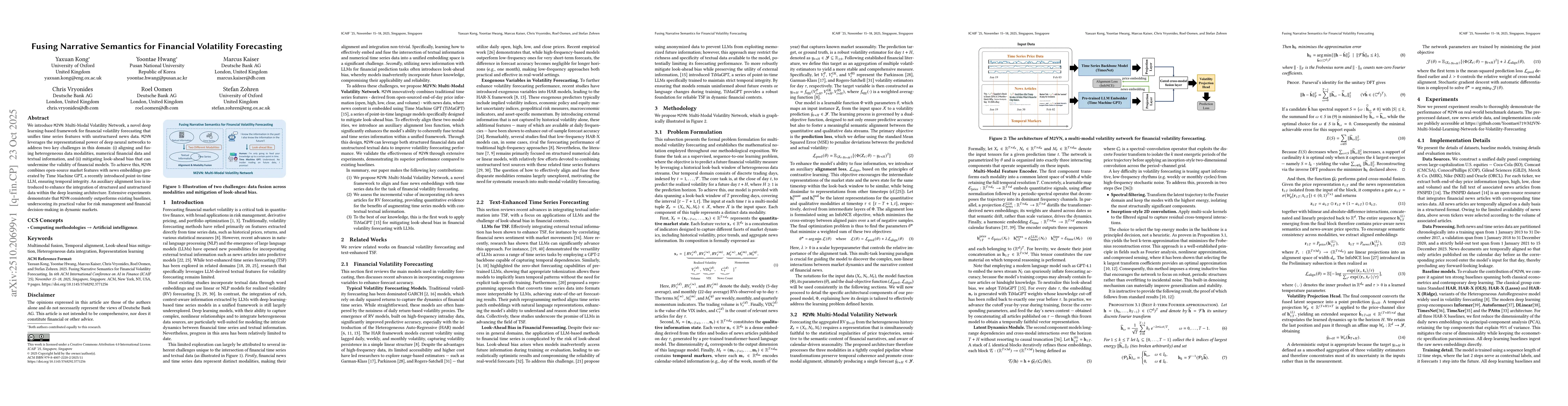

We introduce M2VN: Multi-Modal Volatility Network, a novel deep learning-based framework for financial volatility forecasting that unifies time series features with unstructured news data. M2VN levera...

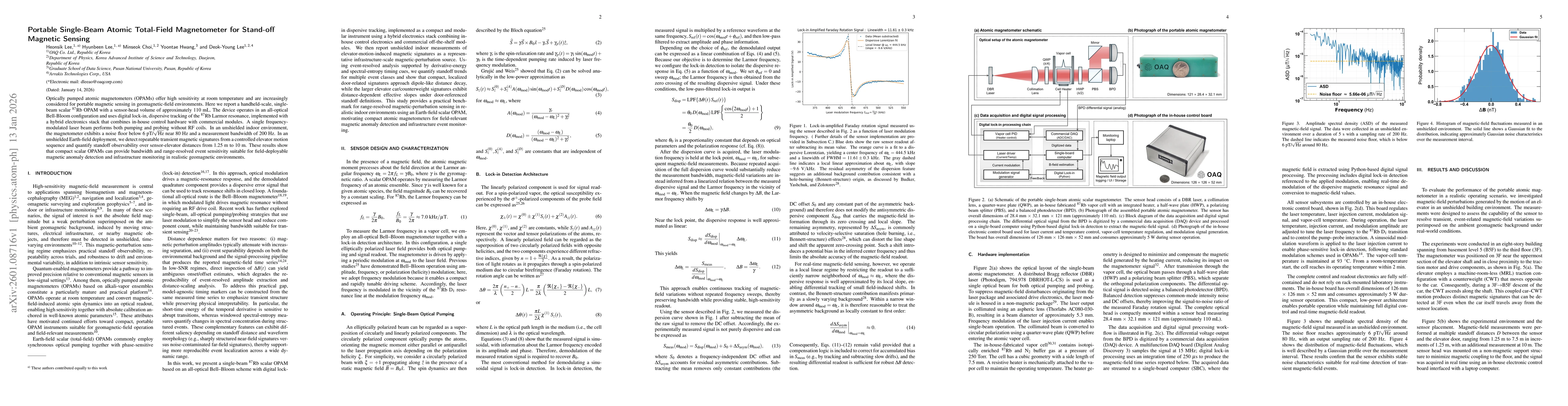

Optically pumped atomic magnetometers (OPAMs) offer high sensitivity at room temperature and are increasingly considered for portable magnetic sensing in geomagnetic-field environments. Here we report...

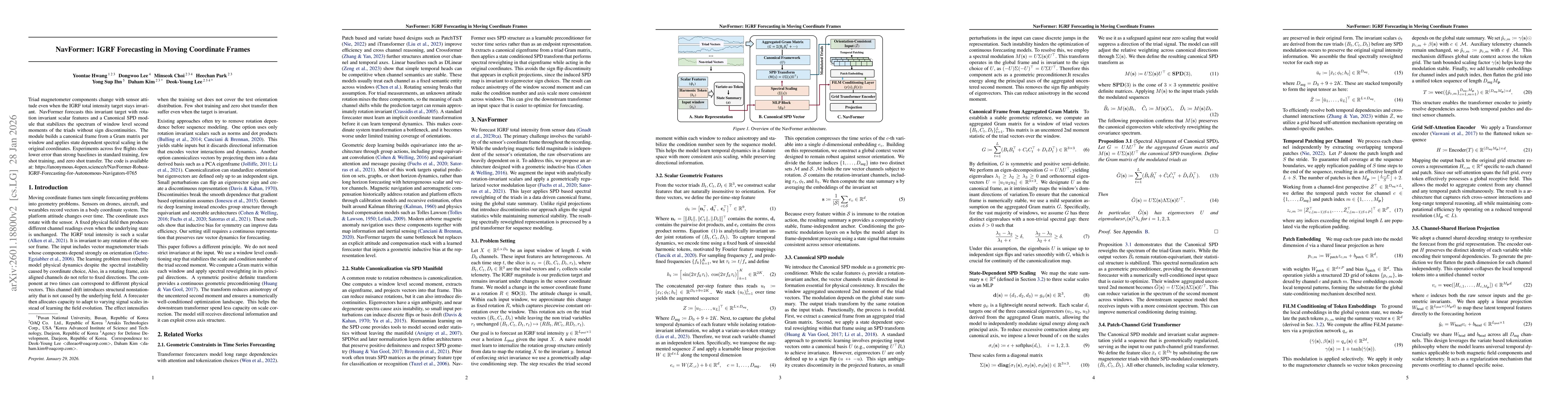

Triad magnetometer components change with sensor attitude even when the IGRF total intensity target stays invariant. NavFormer forecasts this invariant target with rotation invariant scalar features a...

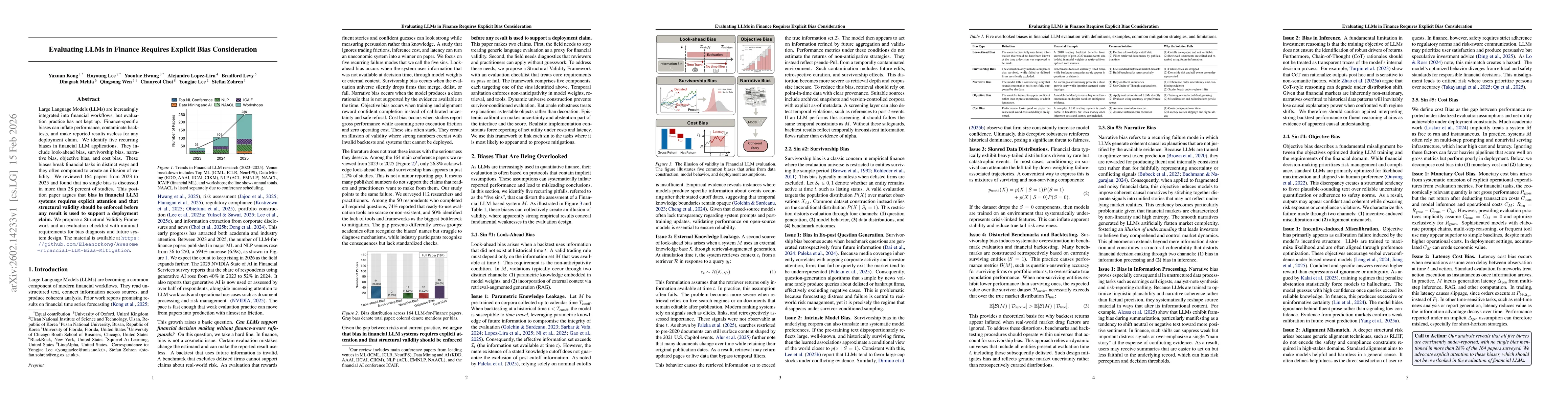

Large Language Models (LLMs) are increasingly integrated into financial workflows, but evaluation practice has not kept up. Finance-specific biases can inflate performance, contaminate backtests, and ...

Mention markets, a type of prediction market in which contracts resolve based on whether a specified keyword is mentioned during a future public event, require accurate probabilistic forecasts of keyw...

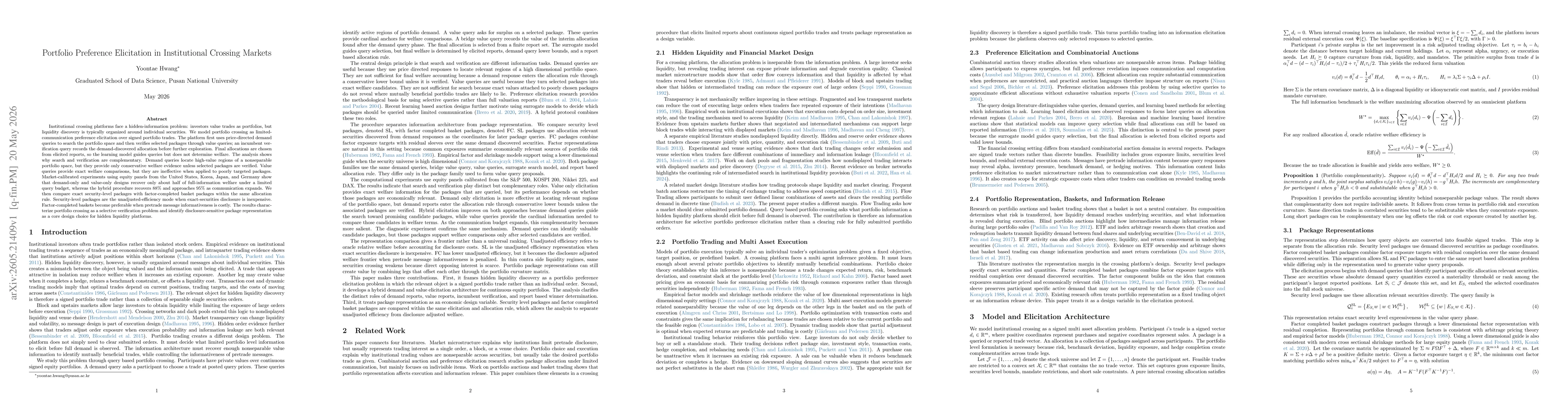

Institutional crossing platforms face a hidden-information problem: investors value trades as portfolios, but liquidity discovery is typically organized around individual securities. We model portfoli...