Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we develop a robust non-parametric realized integrated beta estimator using high-frequency financial data contaminated by microstructure noises, which is robust to the stylized featur...

This paper introduces a unified parametric modeling approach for time-varying market betas that can accommodate continuous-time diffusion and discrete-time series models based on a continuous-time s...

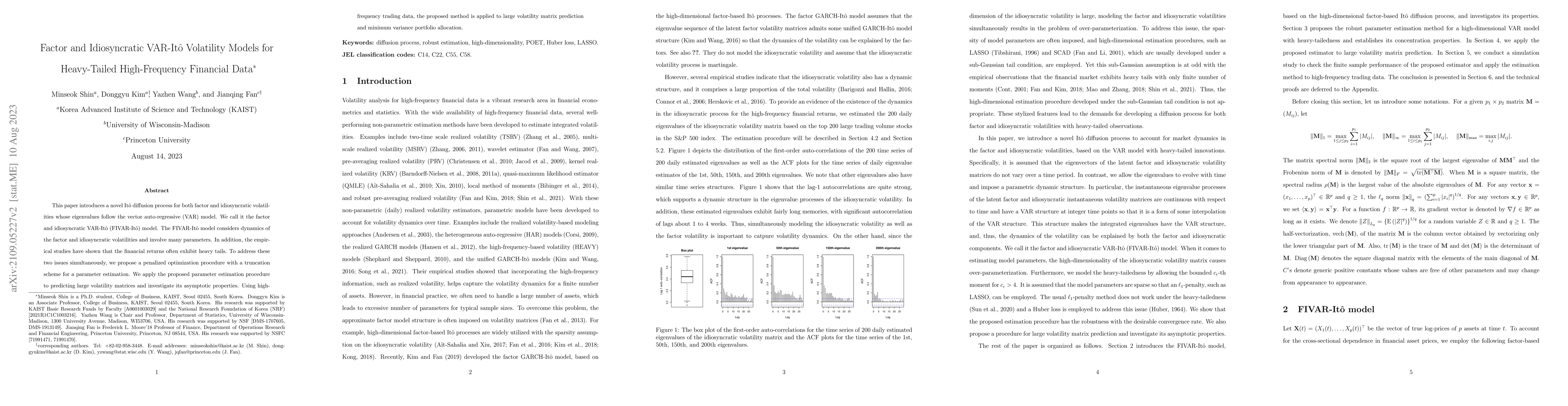

This paper introduces a novel It\^{o} diffusion process for both factor and idiosyncratic volatilities whose eigenvalues follow the vector auto-regressive (VAR) model. We call it the factor and idio...

This paper introduces a novel quantile approach to harness the high-frequency information and improve the daily conditional quantile estimation. Specifically, we model the conditional standard devia...

Quantum computers use quantum resources to carry out computational tasks and may outperform classical computers in solving certain computational problems. Special-purpose quantum computers such as q...

With the rise of big data analytics, multi-layer neural networks have surfaced as one of the most powerful machine learning methods. However, their theoretical mathematical properties are still not ...

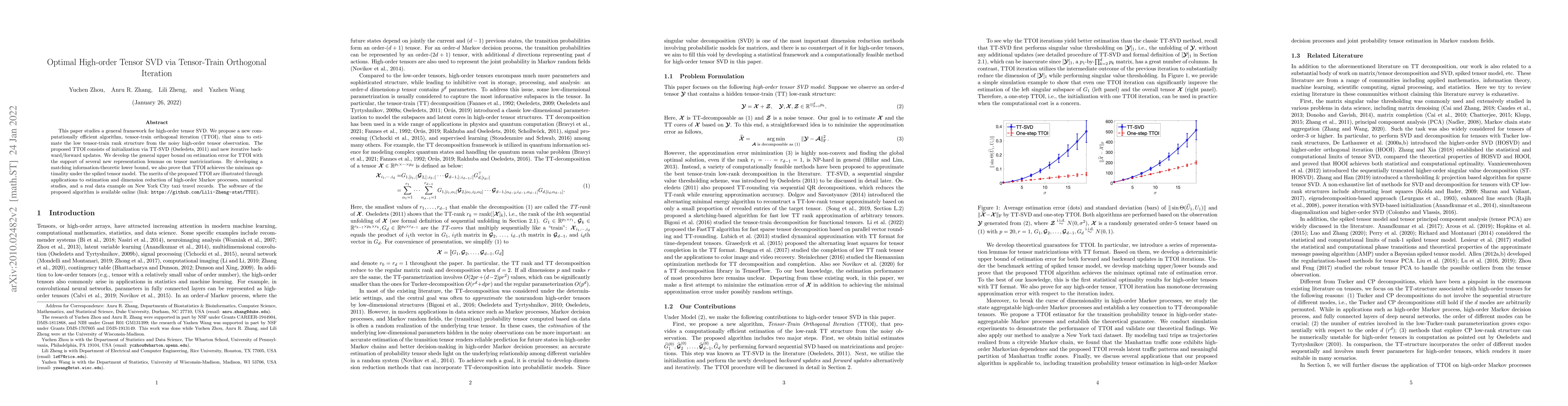

This paper studies a general framework for high-order tensor SVD. We propose a new computationally efficient algorithm, tensor-train orthogonal iteration (TTOI), that aims to estimate the low tensor...

Stochastic gradient descent (SGD) is often applied to train Deep Neural Networks (DNNs), and research efforts have been devoted to investigate the convergent dynamics of SGD and minima found by SGD....

This paper introduces unified models for high-dimensional factor-based Ito process, which can accommodate both continuous-time Ito diffusion and discrete-time stochastic volatility (SV) models by em...

This paper introduces a unified approach for modeling high-frequency financial data that can accommodate both the continuous-time jump-diffusion and discrete-time realized GARCH model by embedding t...

Reinforcement Learning (RL) has proven effective in solving complex decision-making tasks across various domains, but challenges remain in continuous-time settings, particularly when state dynamics ar...

The seminal paper of Jordan, Kinderlehrer, and Otto introduced what is now widely known as the JKO scheme, an iterative algorithmic framework for computing distributions. This scheme can be interprete...

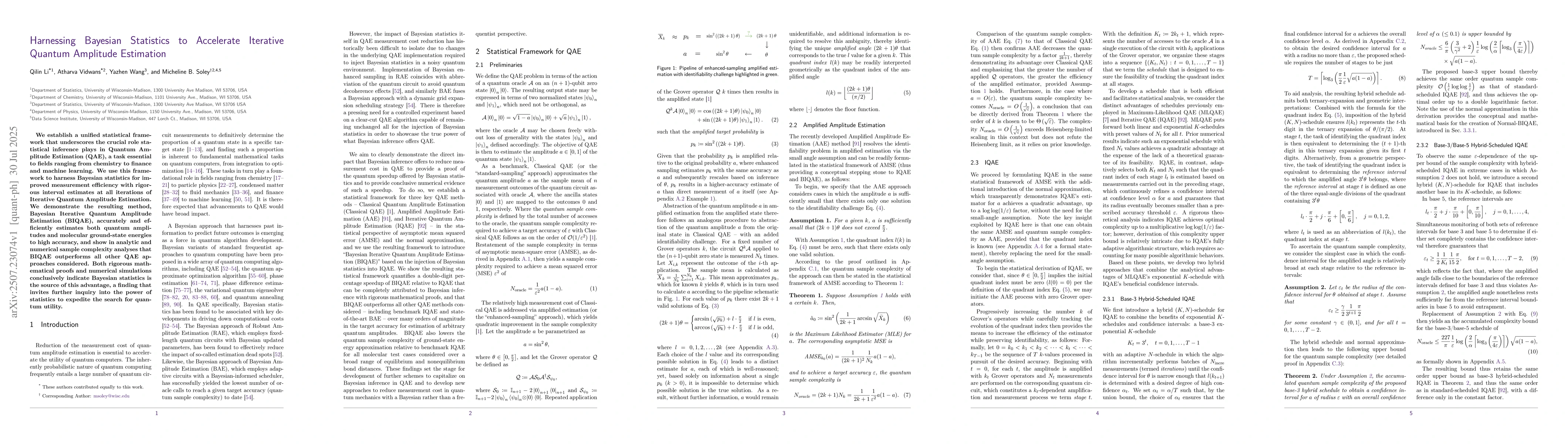

We establish a unified statistical framework that underscores the crucial role statistical inference plays in Quantum Amplitude Estimation (QAE), a task essential to fields ranging from chemistry to f...

Fast computational algorithms are in constant demand, and their development has been driven by advances such as quantum speedup and classical acceleration. This paper intends to study search algorithm...