Academic Profile

Statistics

Similar Authors

Papers on arXiv

Data acquisition, image processing, and image quality are the long-lasting issues for terahertz (THz) 3D reconstructed imaging. Existing methods are primarily designed for 2D scenarios, given the ch...

Sub-terahertz (Sub-THz) waves possess exceptional attributes, capable of penetrating non-metallic and non-polarized materials while ensuring bio-safety. However, their practicality in imaging is mar...

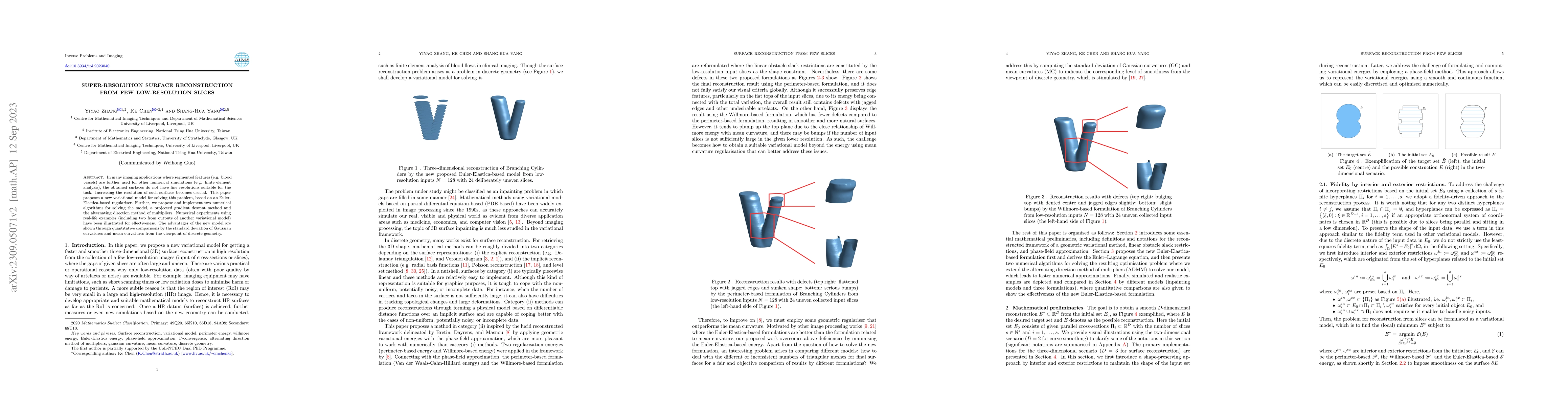

In many imaging applications where segmented features (e.g. blood vessels) are further used for other numerical simulations (e.g. finite element analysis), the obtained surfaces do not have fine res...

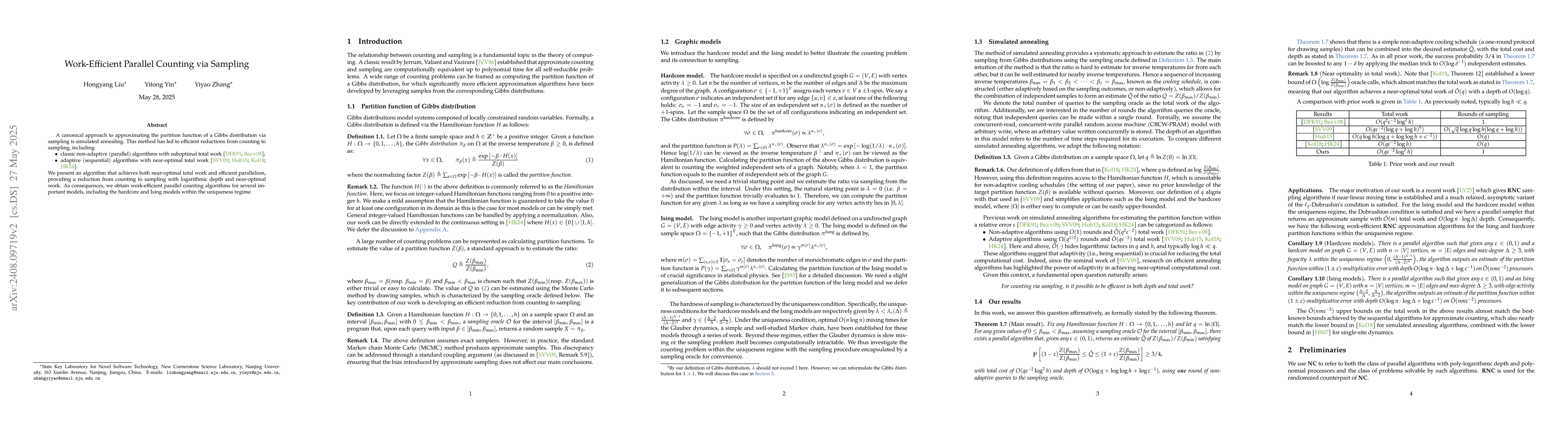

We study the problem of estimating the partition function $Z(\beta) = \sum_{x \in \Omega} \exp[-\beta \cdot H(x)]$ of a Gibbs distribution defined by a Hamiltonian $H(\cdot)$. It is well known that th...

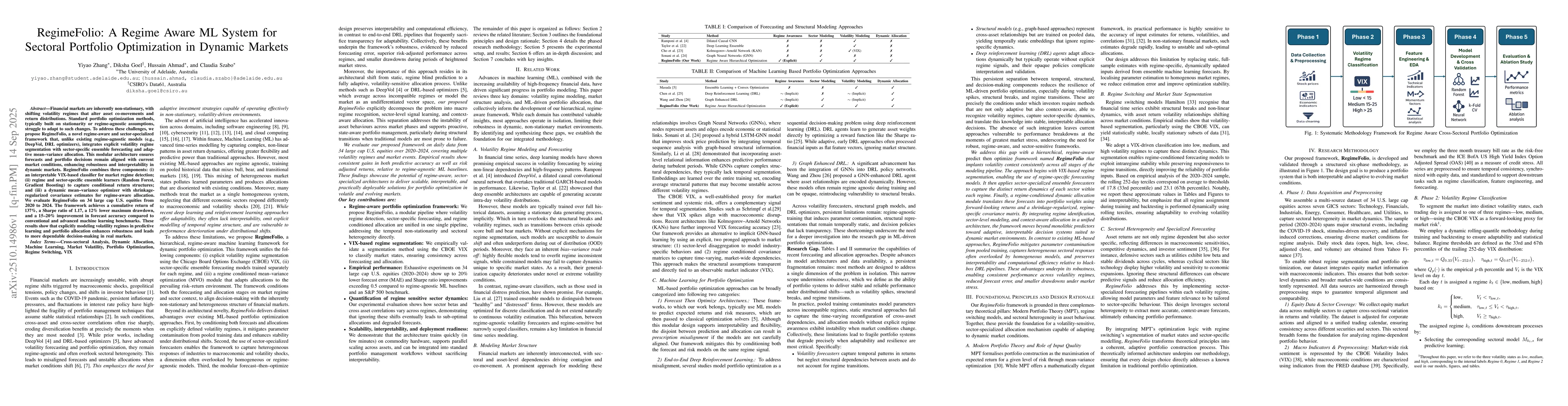

Financial markets are inherently non-stationary, with shifting volatility regimes that alter asset co-movements and return distributions. Standard portfolio optimization methods, typically built on st...

We study the problem of learning a $n$-variables $k$-CNF formula $Φ$ from its i.i.d. uniform random solutions, which is equivalent to learning a Boolean Markov random field (MRF) with $k$-wise hard co...

The computational equivalence between approximate counting and sampling is well established for polynomial-time algorithms. The most efficient general reduction from counting to sampling is achieved v...

Autonomous agents are increasingly deployed in both offensive and defensive cyber operations, creating high-speed, closed-loop interactions in critical infrastructure environments. Advanced Persistent...

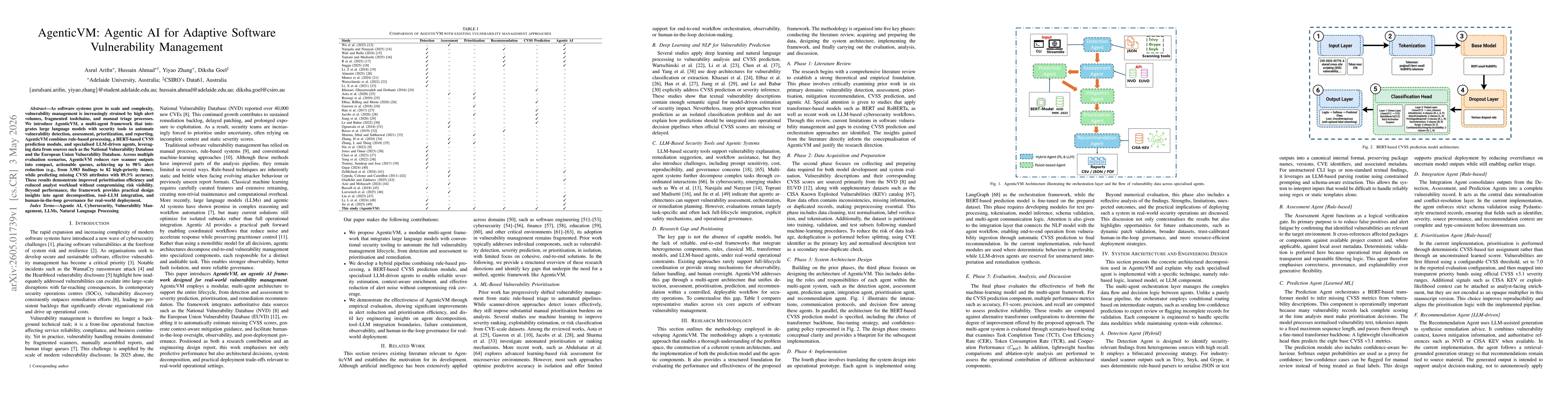

As software systems grow in scale and complexity, vulnerability management is increasingly strained by high alert volumes, fragmented toolchains, and manual triage processes. We introduce AgenticVM, a...