Authors

Publication

Metrics

Quick Actions

Quick Answers

What methodology did the authors use?

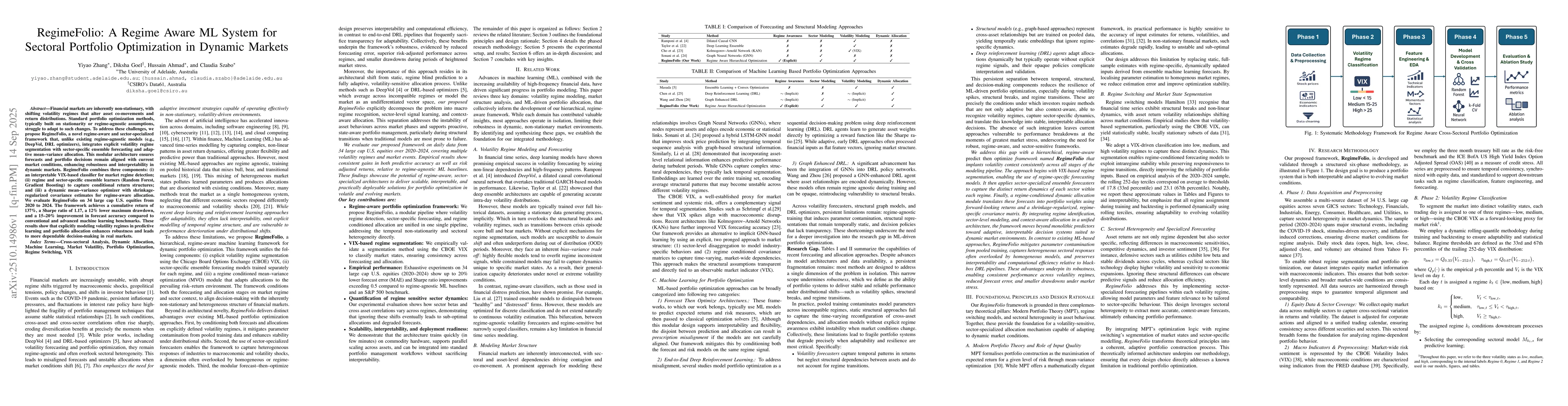

The study employs a regime-aware portfolio optimization framework combining volatility-based regime segmentation, sector-specialized ensemble forecasting, and dynamic allocation with robust risk modeling. More in Methodology →

What are the key results?

15-20% reduction in forecasting error — 137.0% cumulative return over evaluation period More in Key Results →

Why is this work significant?

This research provides a scalable, interpretable framework for improving portfolio performance in volatile markets with significant implications for institutional investment management. More in Significance →

What are the main limitations?

Focus on U.S. large-cap equities — Assumes local stationarity within regimes More in Limitations →

Paper Preview

Abstract

Financial markets are inherently non-stationary, with shifting volatility regimes that alter asset co-movements and return distributions. Standard portfolio optimization methods, typically built on stationarity or regime-agnostic assumptions, struggle to adapt to such changes. To address these challenges, we propose RegimeFolio, a novel regime-aware and sector-specialized framework that, unlike existing regime-agnostic models such as DeepVol and DRL optimizers, integrates explicit volatility regime segmentation with sector-specific ensemble forecasting and adaptive mean-variance allocation. This modular architecture ensures forecasts and portfolio decisions remain aligned with current market conditions, enhancing robustness and interpretability in dynamic markets. RegimeFolio combines three components: (i) an interpretable VIX-based classifier for market regime detection; (ii) regime and sector-specific ensemble learners (Random Forest, Gradient Boosting) to capture conditional return structures; and (iii) a dynamic mean-variance optimizer with shrinkage-regularized covariance estimates for regime-aware allocation. We evaluate RegimeFolio on 34 large cap U.S. equities from 2020 to 2024. The framework achieves a cumulative return of 137 percent, a Sharpe ratio of 1.17, a 12 percent lower maximum drawdown, and a 15 to 20 percent improvement in forecast accuracy compared to conventional and advanced machine learning benchmarks. These results show that explicitly modeling volatility regimes in predictive learning and portfolio allocation enhances robustness and leads to more dependable decision-making in real markets.

AI Key Findings

Generated Nov 01, 2025

Methodology — What approach did the authors take?

The study employs a regime-aware portfolio optimization framework combining volatility-based regime segmentation, sector-specialized ensemble forecasting, and dynamic allocation with robust risk modeling.

Key Results — What are the main findings?

- 15-20% reduction in forecasting error

- 137.0% cumulative return over evaluation period

- 1.17 Sharpe ratio with notable reduction in maximum drawdown

Significance — Why does this research matter?

This research provides a scalable, interpretable framework for improving portfolio performance in volatile markets with significant implications for institutional investment management.

Technical Contribution — What is the technical contribution?

Proposes a regime-conditioned, shrinkage-regularized covariance matrix approach for improved risk estimation stability

Novelty — What is new about this work?

Integrates sector-specific modeling with volatility regime segmentation in a modular framework for adaptive portfolio allocation

Limitations — What are the limitations of this study?

- Focus on U.S. large-cap equities

- Assumes local stationarity within regimes

Future Work — What did the authors propose for future work?

- Extend framework to multi-asset universes

- Develop hybrid regime classifiers integrating macroeconomic indicators

- Explore alternative optimization methods incorporating higher-order moments

How to Cite This Paper

@article{szabo2025regimefolio,

title = {RegimeFolio: A Regime Aware ML System for Sectoral Portfolio

Optimization in Dynamic Markets},

author = {Szabo, Claudia and Goel, Diksha and Ahmad, Hussain and others},

year = {2025},

eprint = {2510.14986},

archivePrefix = {arXiv},

primaryClass = {q-fin.PM},

}Szabo, C., Goel, D., Ahmad, H., & Zhang, Y. (2025). RegimeFolio: A Regime Aware ML System for Sectoral Portfolio

Optimization in Dynamic Markets. arXiv. https://arxiv.org/abs/2510.14986Szabo, Claudia, et al. "RegimeFolio: A Regime Aware ML System for Sectoral Portfolio

Optimization in Dynamic Markets." arXiv, 2025, arxiv.org/abs/2510.14986.PDF Preview

Similar Papers

Found 4 papersRisk-Aware Deep Reinforcement Learning for Dynamic Portfolio Optimization

Emmanuel Lwele, Sabuni Emmanuel, Sitali Gabriel Sitali

Comments (0)