Academic Profile

Statistics

Similar Authors

Papers on arXiv

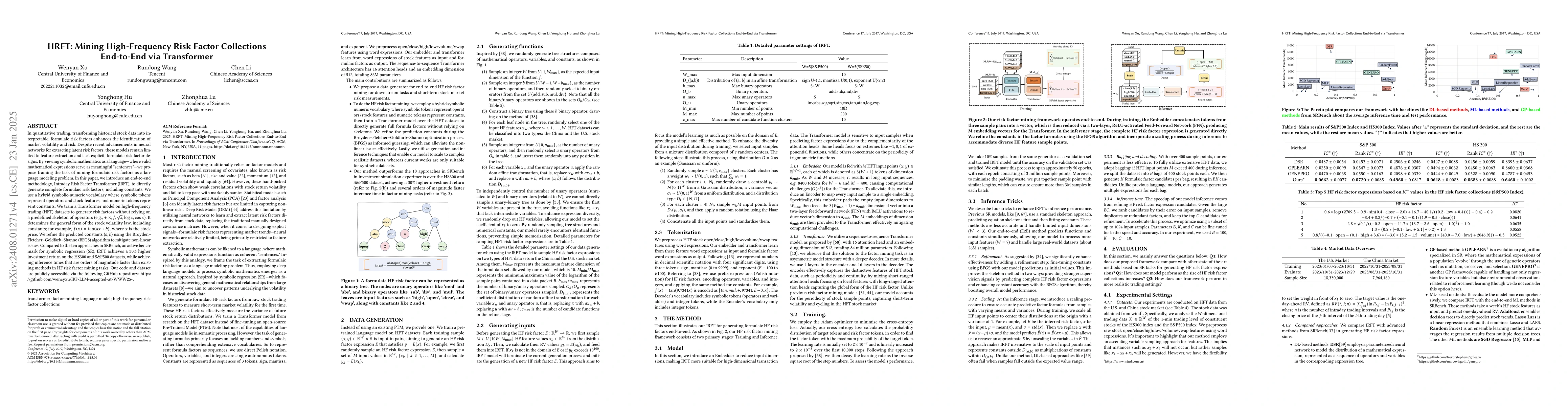

In quantitative trading, transforming historical stock data into interpretable, formulaic risk factors enhances the identification of market volatility and risk. Despite recent advancements in neural ...

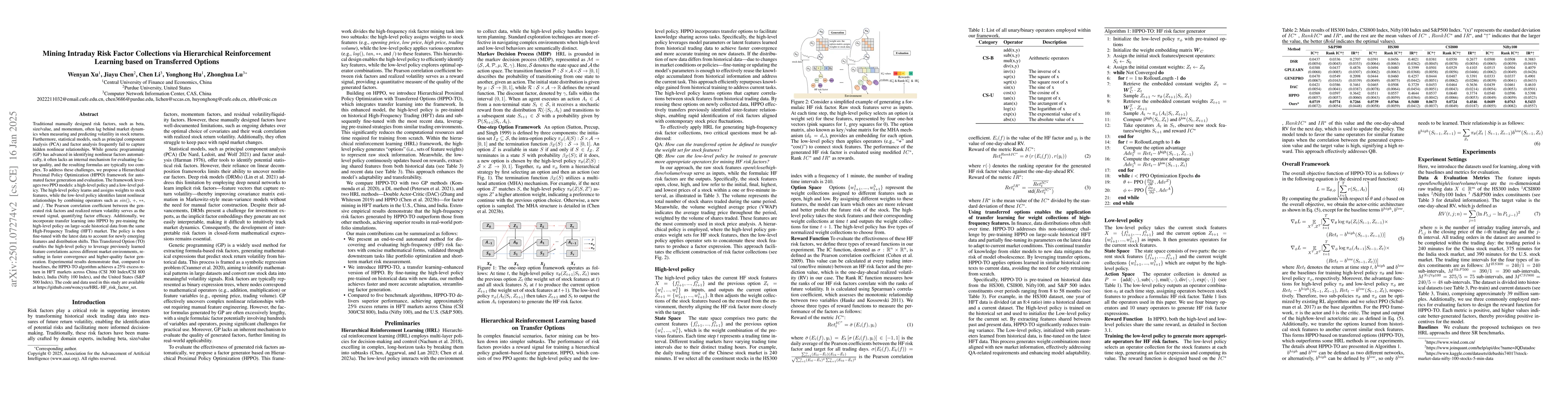

Traditional risk factors like beta, size/value, and momentum often lag behind market dynamics in measuring and predicting stock return volatility. Statistical models like PCA and factor analysis fail ...

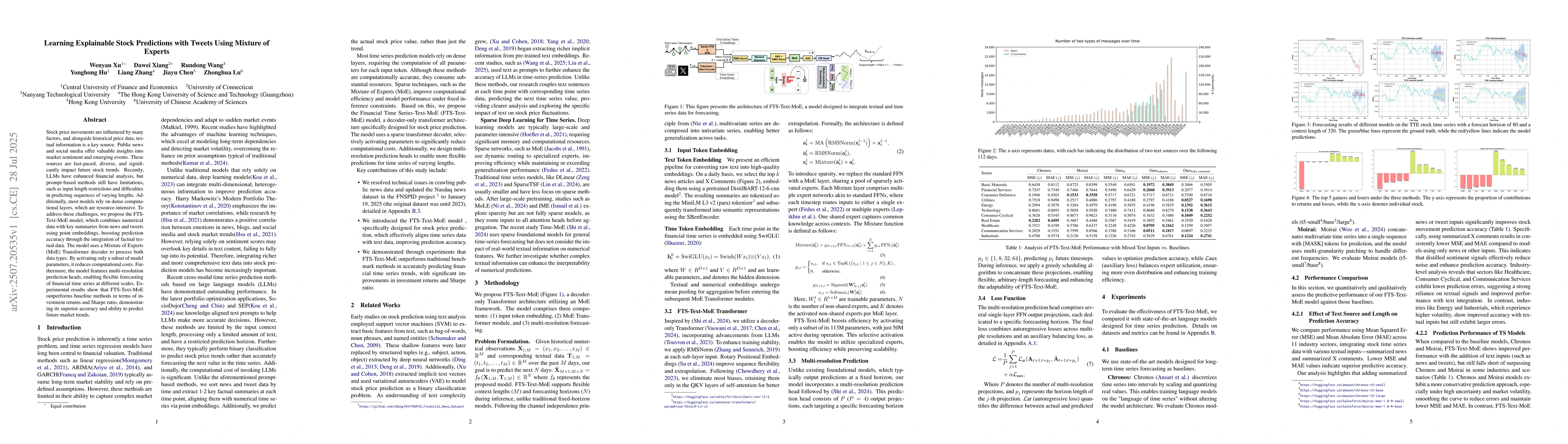

Stock price movements are influenced by many factors, and alongside historical price data, tex-tual information is a key source. Public news and social media offer valuable insights into market sentim...

Rapid financial innovation has been accompanied by a sharp increase in patenting activity, making timely and comprehensive prior-art discovery more difficult. This problem is especially evident in fin...

Optical I/O technologies have emerged as a potential industrial solution for high-performance data interconnection in AI/ML computing acceleration. While optical I/Os are deployed at the edge of compu...