Academic Profile

Statistics

Similar Authors

Papers on arXiv

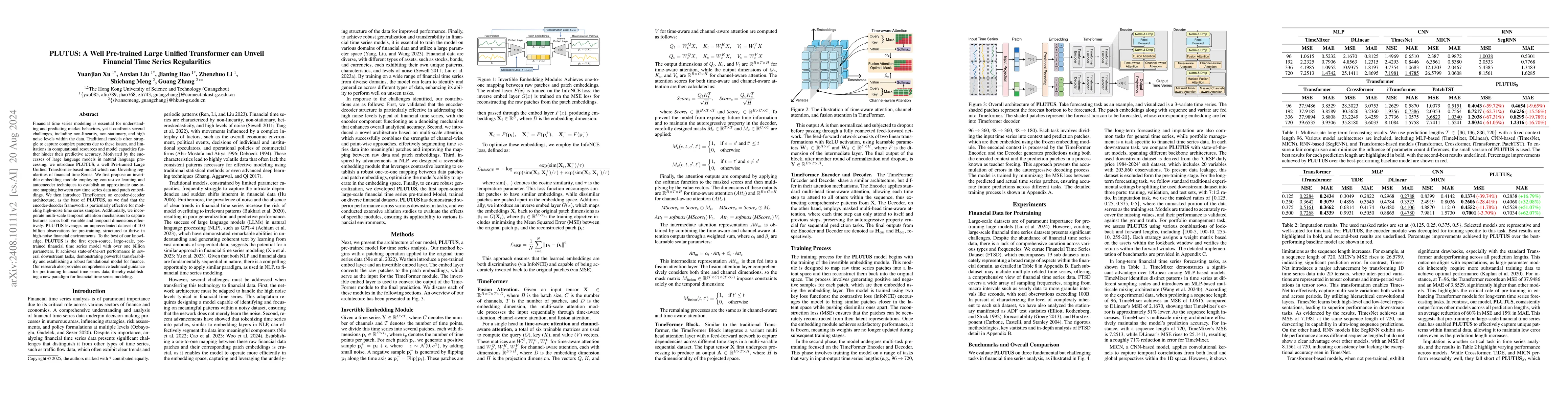

Financial time series modeling is crucial for understanding and predicting market behaviors but faces challenges such as non-linearity, non-stationarity, and high noise levels. Traditional models stru...

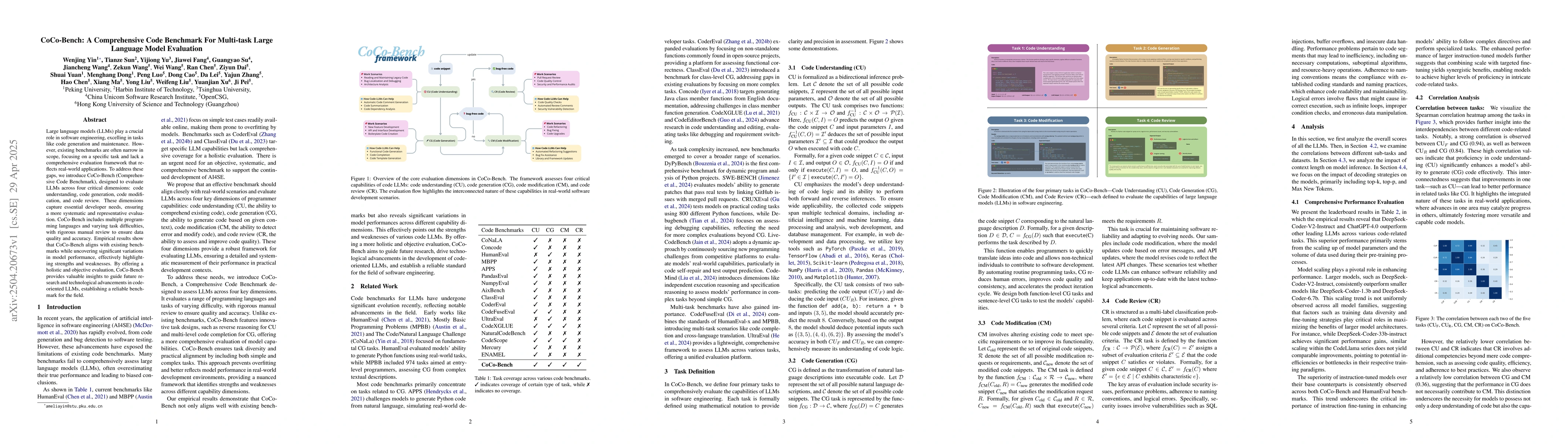

Large language models (LLMs) play a crucial role in software engineering, excelling in tasks like code generation and maintenance. However, existing benchmarks are often narrow in scope, focusing on a...

Financial markets exhibit complex dynamics where localized events trigger ripple effects across entities. Previous event studies, constrained by static single-company analyses and simplistic assumptio...

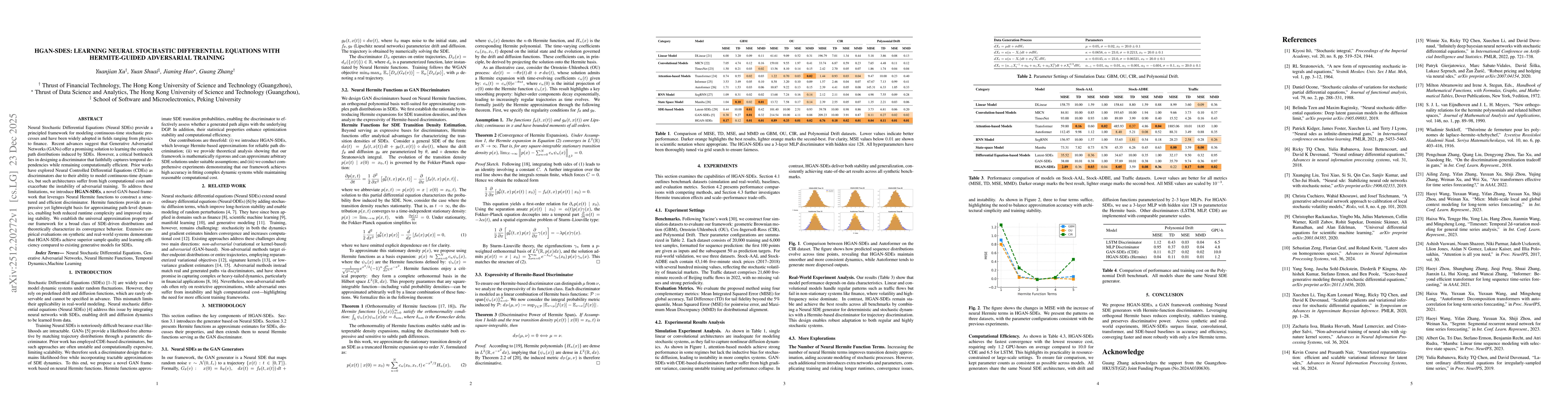

Neural Stochastic Differential Equations (Neural SDEs) provide a principled framework for modeling continuous-time stochastic processes and have been widely adopted in fields ranging from physics to f...

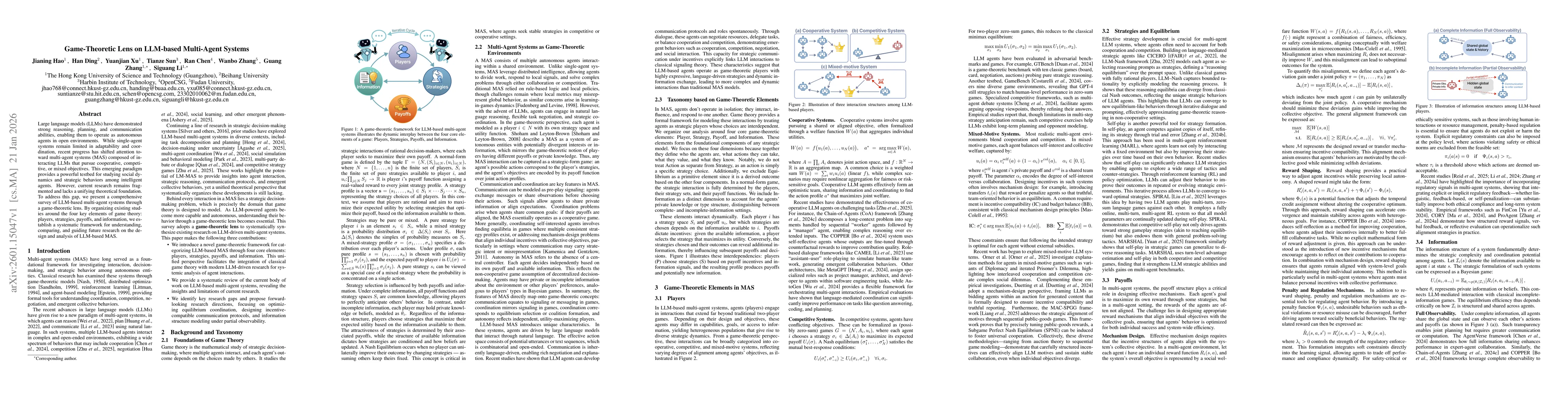

Large language models (LLMs) have demonstrated strong reasoning, planning, and communication abilities, enabling them to operate as autonomous agents in open environments. While single-agent systems r...

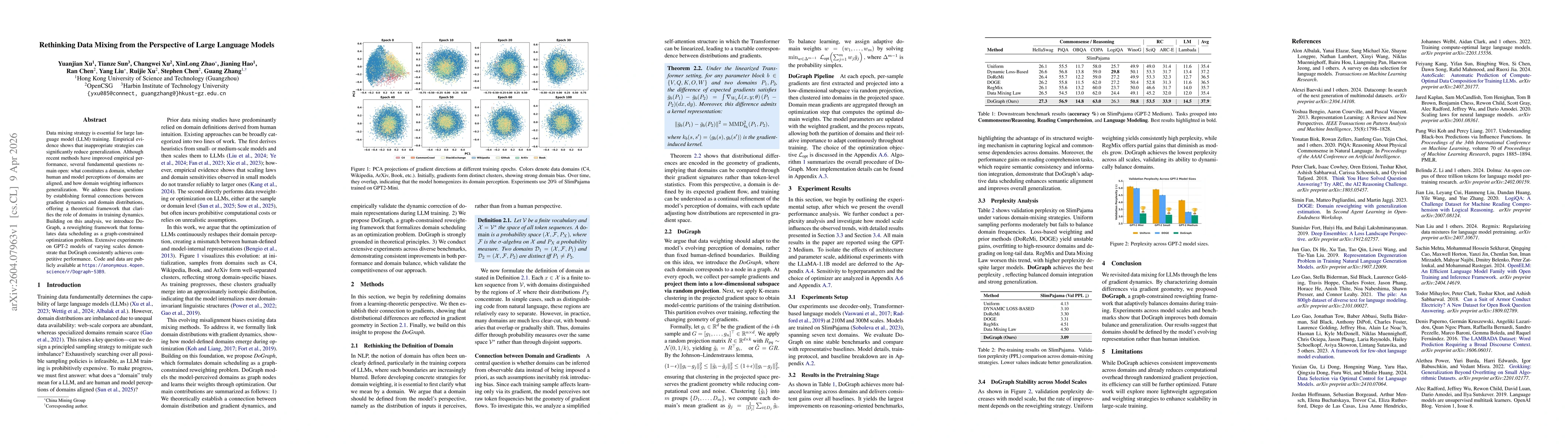

Data mixing strategy is essential for large language model (LLM) training. Empirical evidence shows that inappropriate strategies can significantly reduce generalization. Although recent methods have ...

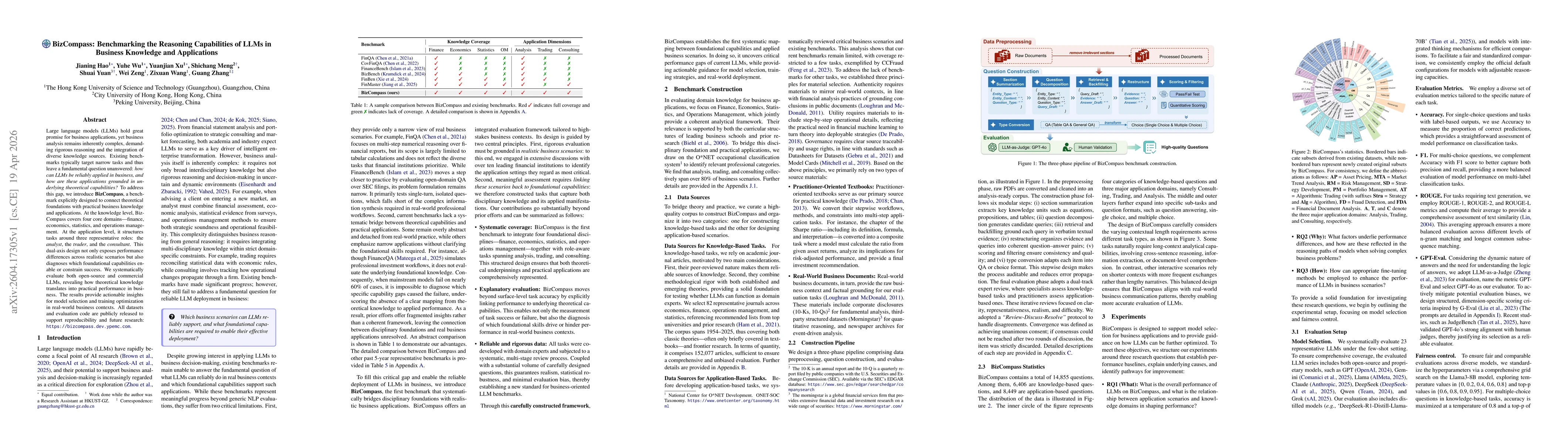

Large language models (LLMs) hold great promise for business applications, yet business analysis remains inherently complex, demanding rigorous reasoning and the integration of diverse knowledge sourc...

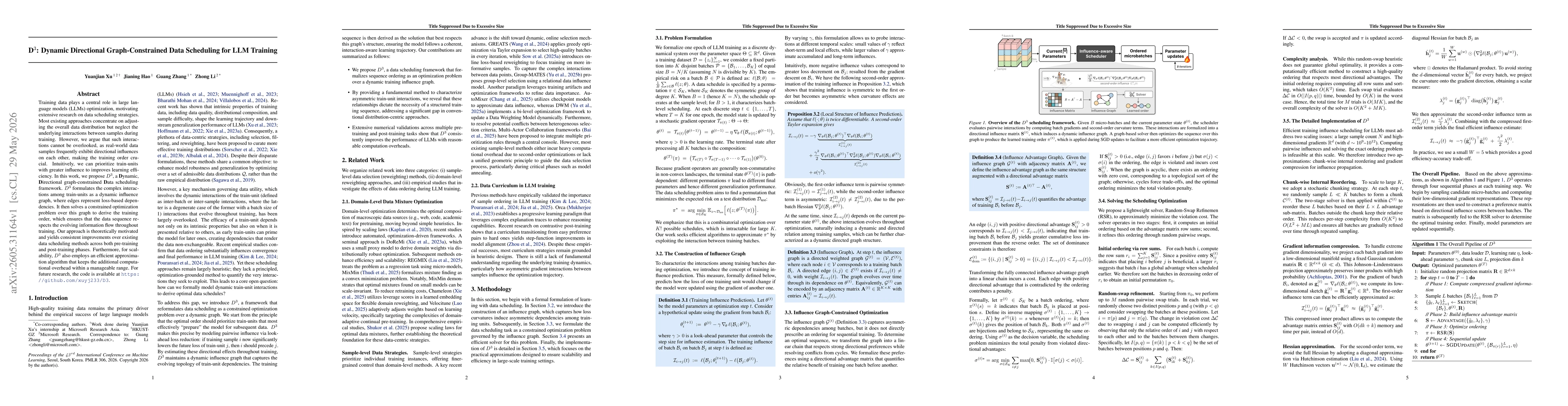

Training data plays a central role in large language models (LLMs) optimization, motivating extensive research on data scheduling strategies. Most existing approaches concentrate on adjusting the over...

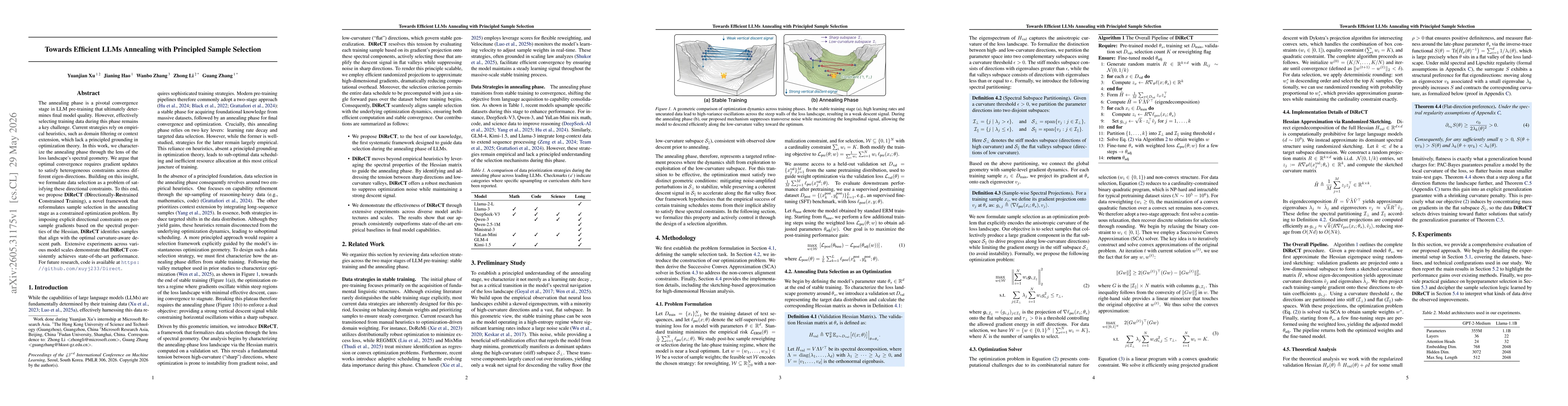

The annealing phase is a pivotal convergence stage in LLM pre-training that ultimately determines final model quality. However, effectively selecting training data during this phase remains a key chal...