Academic Profile

Statistics

Similar Authors

Papers on arXiv

We define and develop an approach for risk budgeting allocation -- a risk diversification portfolio strategy -- where risk is measured using a dynamic time-consistent risk measure. For this, we intr...

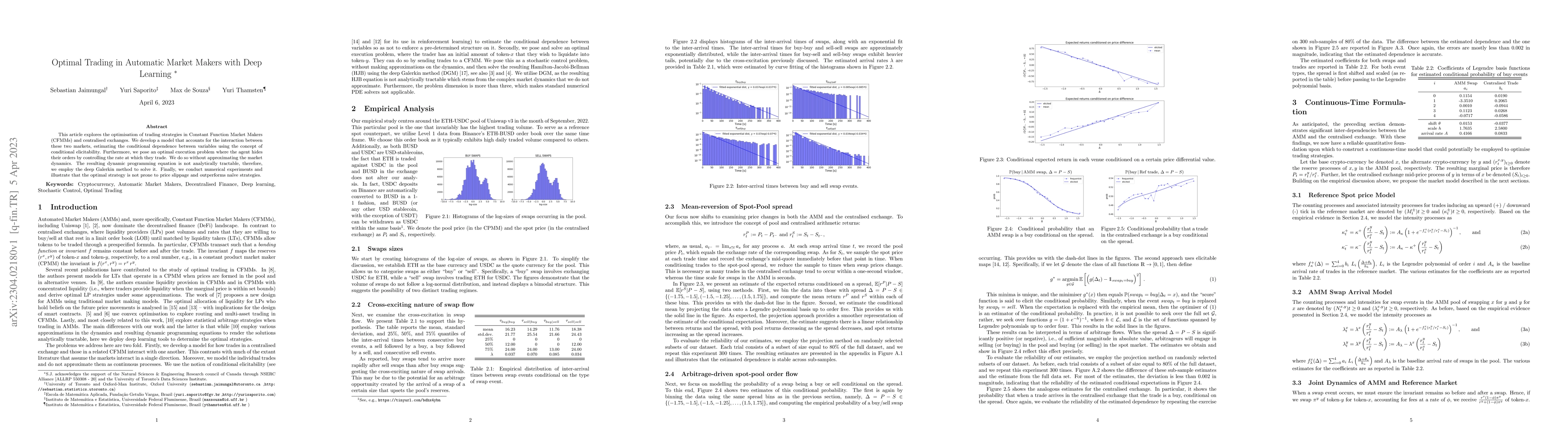

This article explores the optimisation of trading strategies in Constant Function Market Makers (CFMMs) and centralised exchanges. We develop a model that accounts for the interaction between these ...

Inverse problems are paramount in Science and Engineering. In this paper, we consider the setup of Statistical Inverse Problem (SIP) and demonstrate how Stochastic Gradient Descent (SGD) algorithms ...

This paper proposes a classification model for predicting the main activity of bitcoin addresses based on their balances. Since the balances are functions of time, we apply methods from functional d...

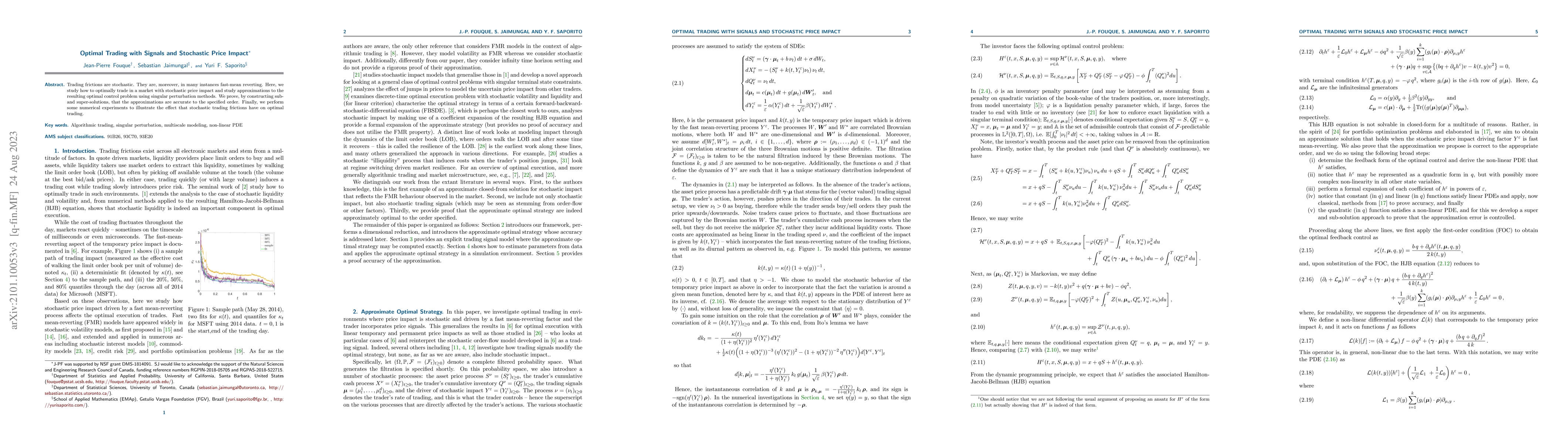

Trading frictions are stochastic. They are, moreover, in many instances fast-mean reverting. Here, we study how to optimally trade in a market with stochastic price impact and study approximations t...

In this paper we derive a efficient Monte Carlo approximation for the price of path-dependent derivatives under the multiscale stochastic volatility models of Fouque \textit{et al}. Using the formul...

This paper is concerned with the process of risk allocation for a generic multivariate model when the risk measure is chosen as the Value-at-Risk (VaR). We recast the traditional Euler contributions...

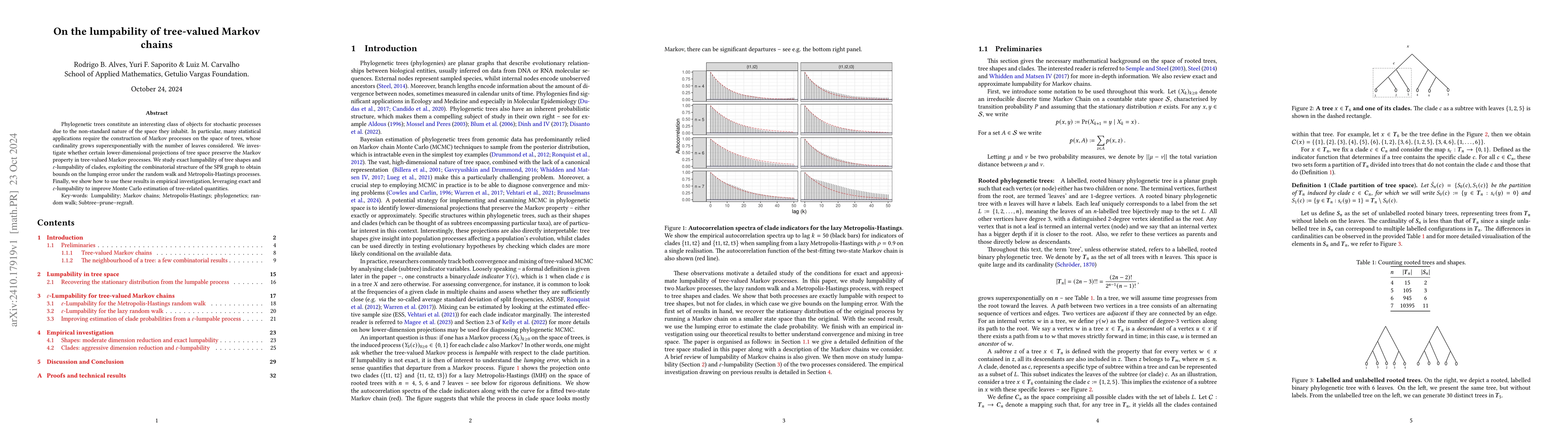

Phylogenetic trees constitute an interesting class of objects for stochastic processes due to the non-standard nature of the space they inhabit. In particular, many statistical applications require th...

Recently, there has been a growing interest in generative models based on diffusions driven by the empirical robustness of these methods in generating high-dimensional photorealistic images and the po...

We present a novel numerical method for solving McKean-Vlasov forward-backward stochastic differential equations (MV-FBSDEs) with common noise, combining Picard iterations, elicitability and deep lear...

In this paper, we propose a random gradient-free method for optimization in infinite dimensional Hilbert spaces, applicable to functional optimization in diverse settings. Though such problems are oft...

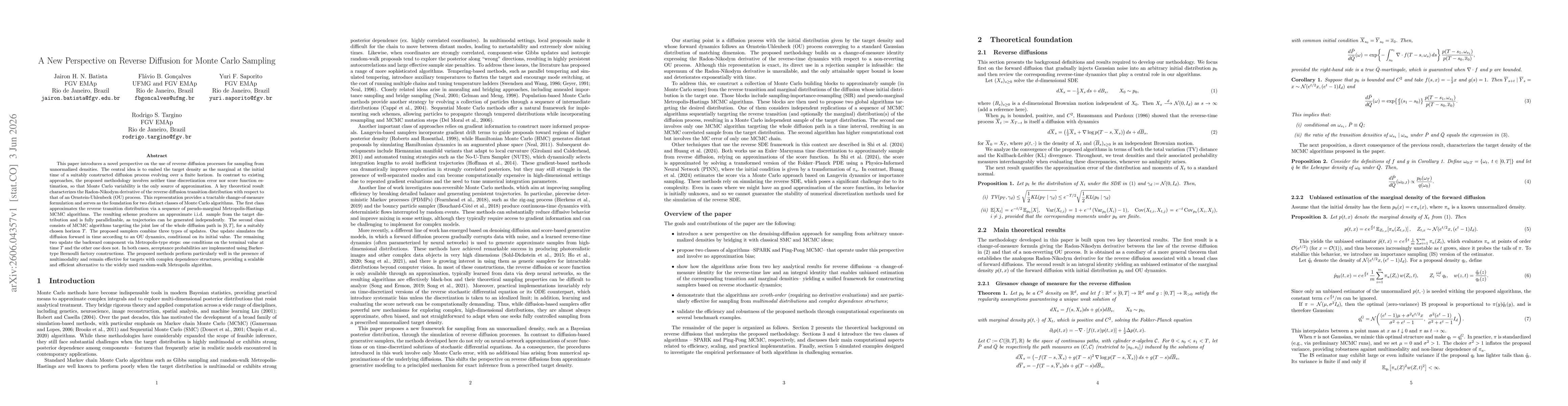

This paper introduces a novel perspective on the use of reverse diffusion processes for sampling from unnormalized densities. The central idea is to embed the target density as the marginal at the ini...