Publication

Metrics

AI Quick Summary

This paper explores optimal trading strategies in markets with stochastic price impact, employing singular perturbation methods to approximate the optimal control problem. Numerical experiments demonstrate the impact of stochastic trading frictions on optimal trading decisions.

Paper Preview

Abstract

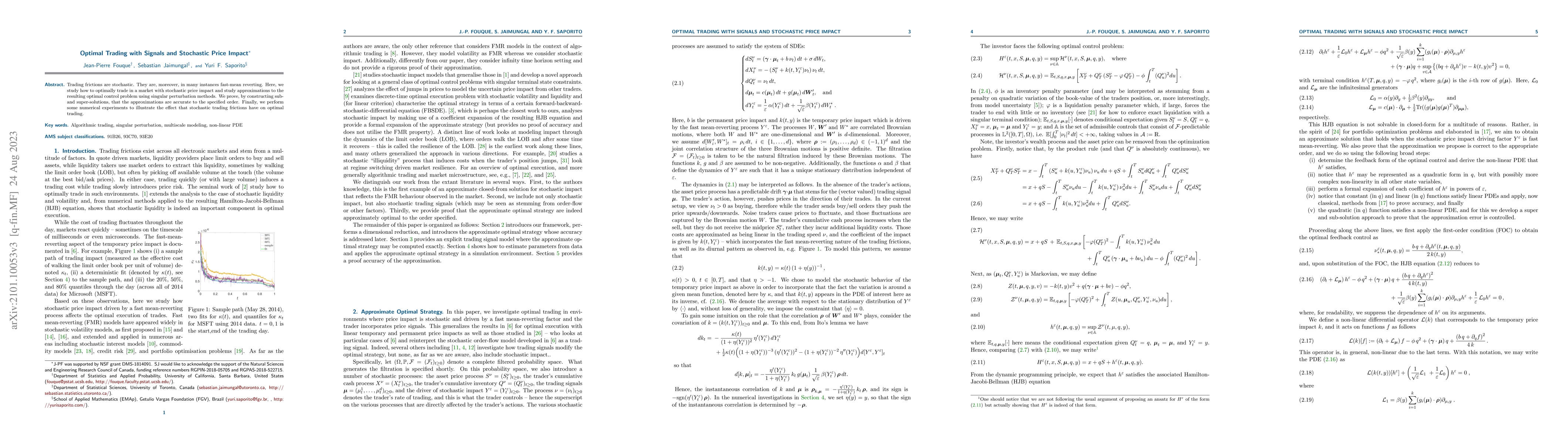

Trading frictions are stochastic. They are, moreover, in many instances fast-mean reverting. Here, we study how to optimally trade in a market with stochastic price impact and study approximations to the resulting optimal control problem using singular perturbation methods. We prove, by constructing sub- and super-solutions, that the approximations are accurate to the specified order. Finally, we perform some numerical experiments to illustrate the effect that stochastic trading frictions have on optimal trading.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0