Academic Profile

Statistics

Similar Authors

Papers on arXiv

Mean Field Control Games (MFCG), introduced in [Angiuli et al., 2022a], represent competitive games between a large number of large collaborative groups of agents in the infinite limit of number and...

We establish the convergence of the unified two-timescale Reinforcement Learning (RL) algorithm presented in a previous work by Angiuli et al. This algorithm provides solutions to Mean Field Game (M...

We present the development and analysis of a reinforcement learning (RL) algorithm designed to solve continuous-space mean field game (MFG) and mean field control (MFC) problems in a unified manner....

We introduce the notions of Collective Arbitrage and of Collective Super-replication in a discrete-time setting where agents are investing in their markets and are allowed to cooperate through excha...

In this work we propose deep learning-based algorithms for the computation of systemic shortfall risk measures defined via multivariate utility functions. We discuss the key related theoretical aspe...

We propose a mean field control game model for the intra-and-inter-bank borrowing and lending problem. This framework allows to study the competitive game arising between groups of collaborative ban...

The aim of this paper is to study a new methodological framework for systemic risk measures by applying deep learning method as a tool to compute the optimal strategy of capital allocations. Under t...

We present a new combined \textit{mean field control game} (MFCG) problem which can be interpreted as a competitive game between collaborating groups and its solution as a Nash equilibrium between g...

We analyze the systemic risk for disjoint and overlapping groups (e.g., central clearing counterparties (CCP)) by proposing new models with realistic game features. Specifically, we generalize the s...

Mean field games (MFG) and mean field control problems (MFC) are frameworks to study Nash equilibria or social optima in games with a continuum of agents. These problems can be used to approximate c...

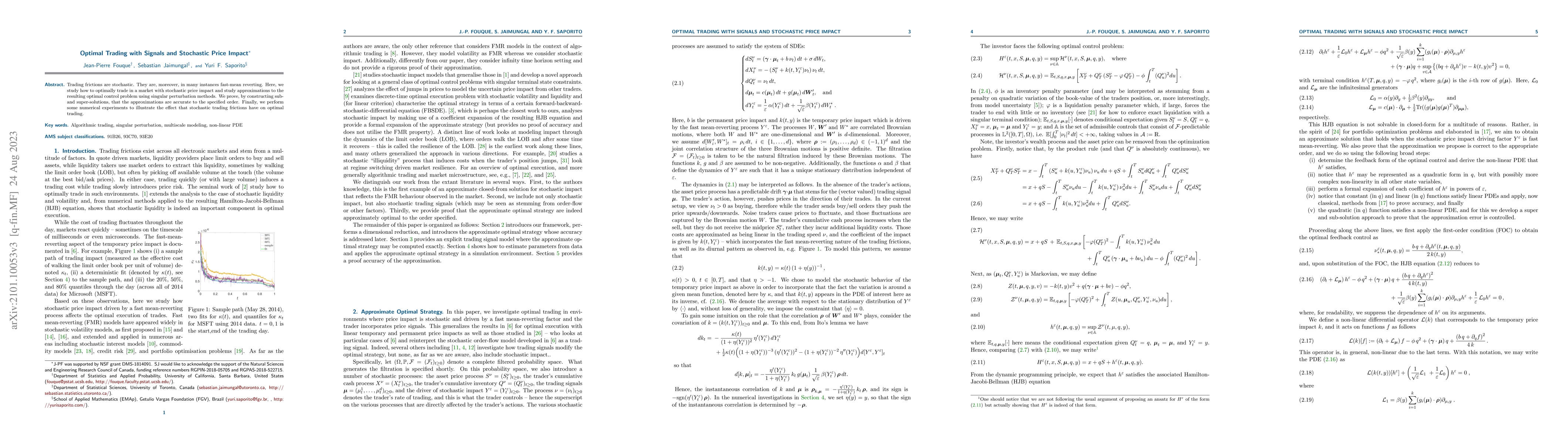

Trading frictions are stochastic. They are, moreover, in many instances fast-mean reverting. Here, we study how to optimally trade in a market with stochastic price impact and study approximations t...

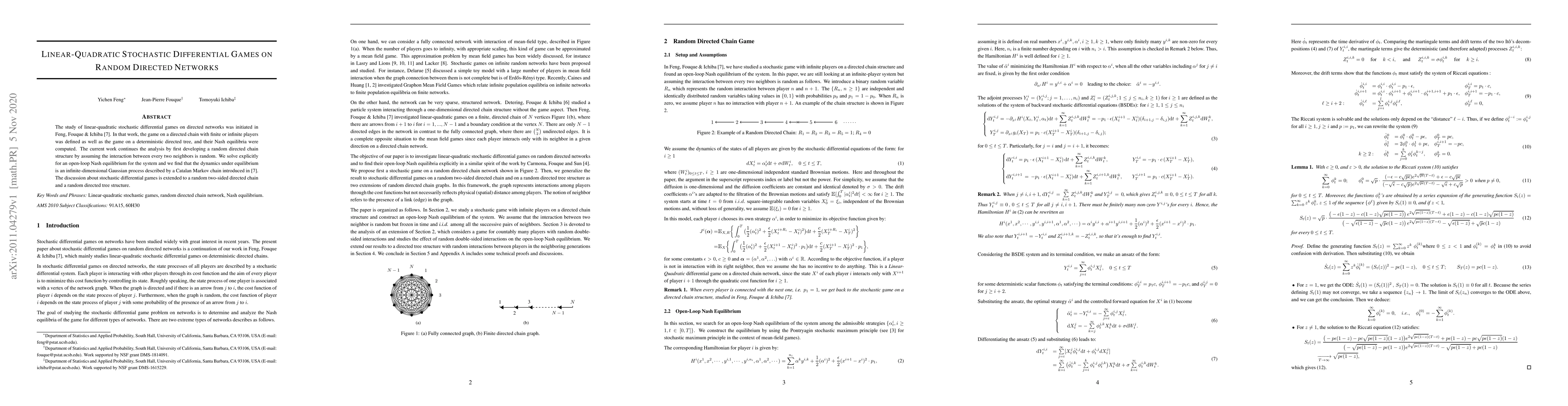

The study of linear-quadratic stochastic differential games on directed networks was initiated in Feng, Fouque \& Ichiba \cite{fengFouqueIchiba2020linearquadratic}. In that work, the game on a direc...

The problem of portfolio allocation in the context of stocks evolving in random environments, that is with volatility and returns depending on random factors, has attracted a lot of attention. The p...

We propose a novel concept of a Systemic Optimal Risk Transfer Equilibrium (SORTE), which is inspired by the B\"uhlmann's classical notion of an Equilibrium Risk Exchange. We provide sufficient gene...

We consider a general class of mean field control problems described by stochastic delayed differential equations of McKean-Vlasov type. Two numerical algorithms are provided based on deep learning ...

We analyze both finite and infinite systems of Riccati equations derived from stochastic differential games on infinite networks. We discuss a connection to the Catalan numbers and the convergence of ...

We explicitly connect (discrete-time) quantum walks on Z with a four-state Markov additive process via a Feynman-type formula (2.5). Using this representation, we derive a relation between the spectra...

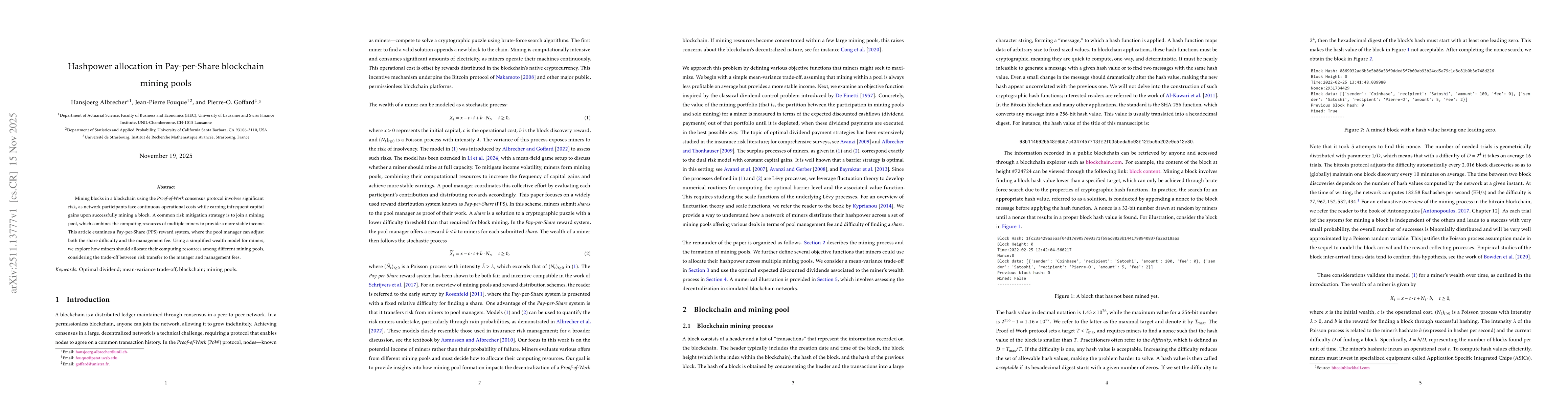

Mining blocks in a blockchain using the \textit{Proof-of-Work} consensus protocol involves significant risk, as network participants face continuous operational costs while earning infrequent capital ...

We establish the convergence of the deep actor-critic reinforcement learning algorithm presented in [Angiuli et al., 2023a] in the setting of continuous state and action spaces with an infinite discre...