Academic Profile

Statistics

Similar Authors

Papers on arXiv

We investigate sample-based learning of conditional distributions on multi-dimensional unit boxes, allowing for different dimensions of the feature and target spaces. Our approach involves clusterin...

When an investor is faced with the option to purchase additional information regarding an asset price, how much should she pay? To address this question, we solve for the indifference price of infor...

One approach to reducing greenhouse gas (GHG) emissions is to incentivize carbon capturing and carbon reducing projects while simultaneously penalising excess GHG output. In this work, we present a ...

We study a reinsurer who faces multiple sources of model uncertainty. The reinsurer offers contracts to $n$ insurers whose claims follow compound Poisson processes representing both idiosyncratic an...

This paper proposes a novel framework for identifying an agent's risk aversion using interactive questioning. Our study is conducted in two scenarios: a one-period case and an infinite horizon case....

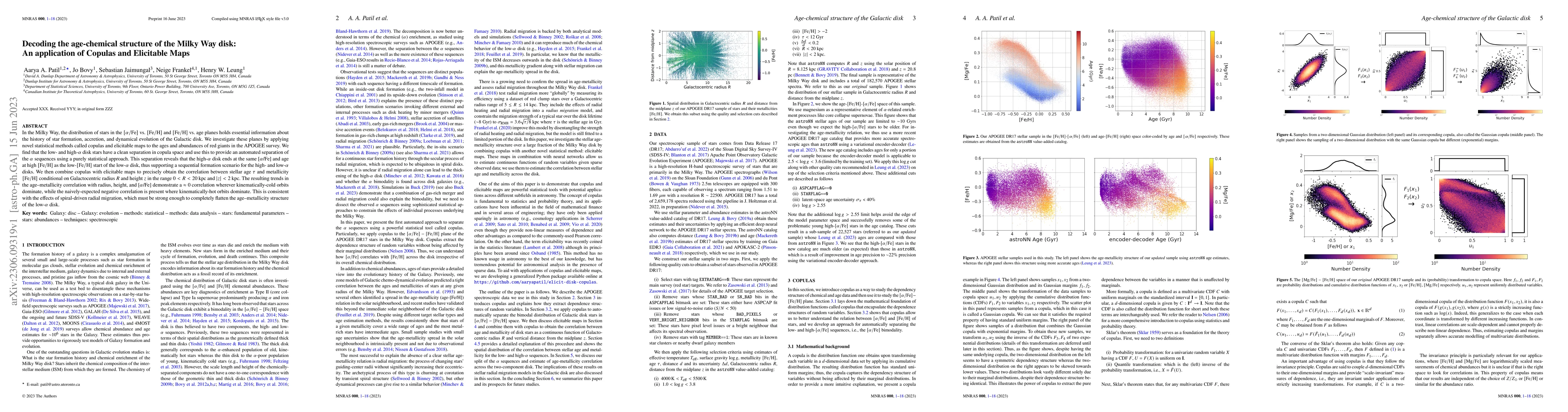

In the Milky Way, the distribution of stars in the $[\alpha/\mathrm{Fe}]$ vs. $[\mathrm{Fe/H}]$ and $[\mathrm{Fe/H}]$ vs. age planes holds essential information about the history of star formation, ...

We define and develop an approach for risk budgeting allocation -- a risk diversification portfolio strategy -- where risk is measured using a dynamic time-consistent risk measure. For this, we intr...

This article explores the optimisation of trading strategies in Constant Function Market Makers (CFMMs) and centralised exchanges. We develop a model that accounts for the interaction between these ...

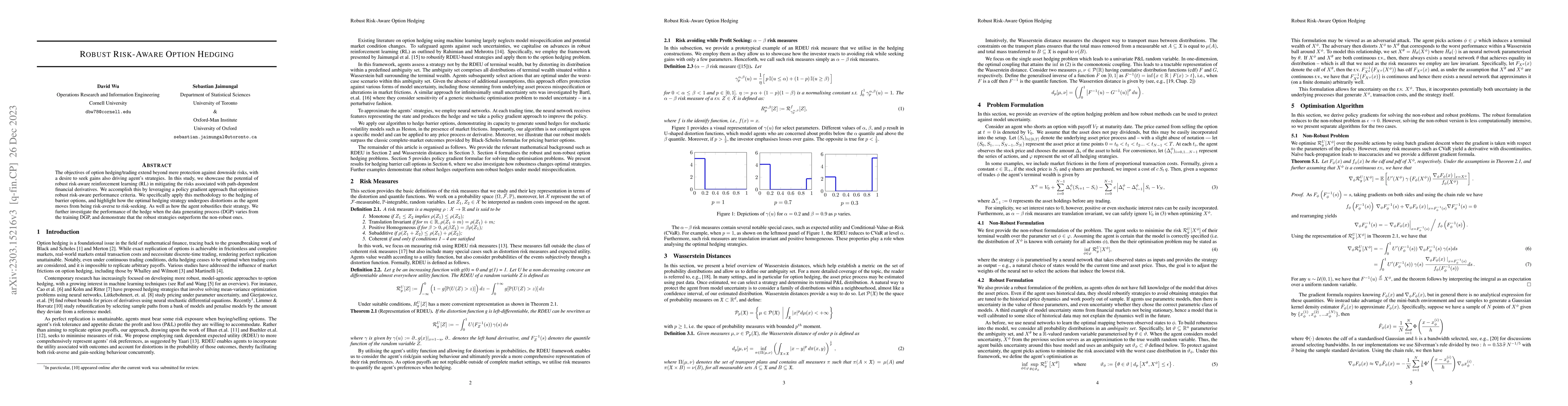

The objectives of option hedging/trading extend beyond mere protection against downside risks, with a desire to seek gains also driving agent's strategies. In this study, we showcase the potential o...

We introduce a new approach for generating sequences of implied volatility (IV) surfaces across multiple assets that is faithful to historical prices. We do so using a combination of functional data...

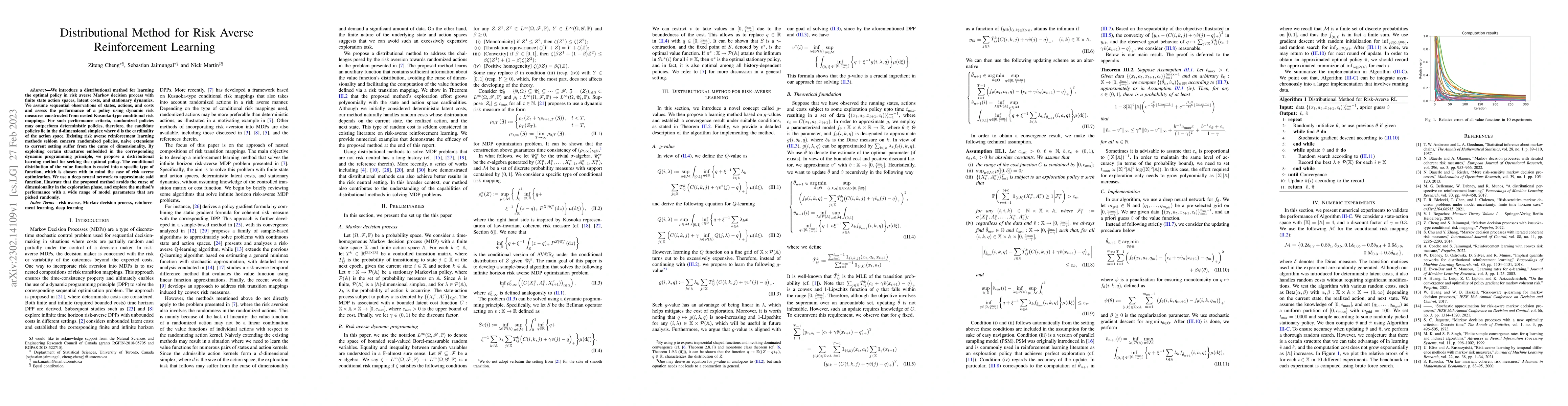

We introduce a distributional method for learning the optimal policy in risk averse Markov decision process with finite state action spaces, latent costs, and stationary dynamics. We assume sequenti...

We study optimal control in models with latent factors where the agent controls the distribution over actions, rather than actions themselves, in both discrete and continuous time. To encourage expl...

Stress testing, and in particular, reverse stress testing, is a prominent exercise in risk management practice. Reverse stress testing, in contrast to (forward) stress testing, aims to find an alter...

We propose a novel framework to solve risk-sensitive reinforcement learning (RL) problems where the agent optimises time-consistent dynamic spectral risk measures. Based on the notion of conditional...

By adopting a distributional viewpoint on law-invariant convex risk measures, we construct dynamics risk measures (DRMs) at the distributional level. We then apply these DRMs to investigate Markov d...

We develop an approach for solving time-consistent risk-sensitive stochastic optimization problems using model-free reinforcement learning (RL). Specifically, we assume agents assess the risk of a s...

Principal agent games are a growing area of research which focuses on the optimal behaviour of a principal and an agent, with the former contracting work from the latter, in return for providing a m...

Here, we develop a deep learning algorithm for solving Principal-Agent (PA) mean field games with market-clearing conditions -- a class of problems that have thus far not been studied and one that p...

High-resolution spectroscopic surveys of the Milky Way have entered the Big Data regime and have opened avenues for solving outstanding questions in Galactic archaeology. However, exploiting their f...

We present a reinforcement learning (RL) approach for robust optimisation of risk-aware performance criteria. To allow agents to express a wide variety of risk-reward profiles, we assess the value o...

We propose a hybrid method for generating arbitrage-free implied volatility (IV) surfaces consistent with historical data by combining model-free Variational Autoencoders (VAEs) with continuous time...

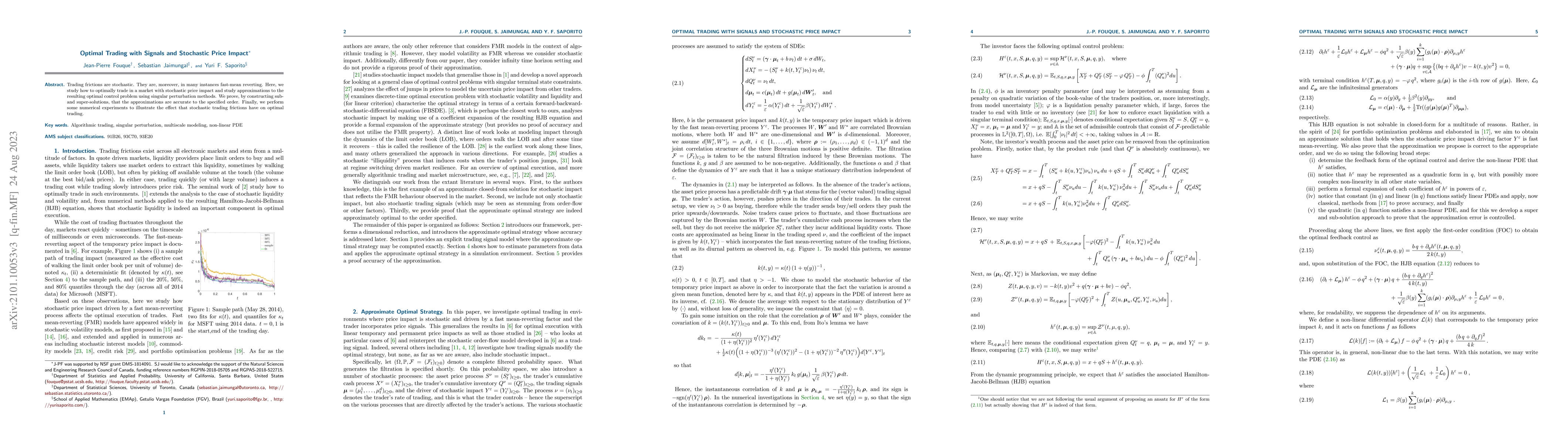

Trading frictions are stochastic. They are, moreover, in many instances fast-mean reverting. Here, we study how to optimally trade in a market with stochastic price impact and study approximations t...

We study the problem of active portfolio management where an investor aims to outperform a benchmark strategy's risk profile while not deviating too far from it. Specifically, an investor considers ...

We study a general class of entropy-regularized multi-variate LQG mean field games (MFGs) in continuous time with $K$ distinct sub-population of agents. We extend the notion of actions to action dis...

We develop the optimal trading strategy for a foreign exchange (FX) broker who must liquidate a large position in an illiquid currency pair. To maximize revenues, the broker considers trading in a c...

We address the Merton problem of maximizing the expected utility of terminal wealth using techniques from variational analysis. Under a general continuous semimartingale market model with stochastic...

Latency (i.e., time delay) in electronic markets affects the efficacy of liquidity taking strategies. During the time liquidity takers process information and send marketable limit orders (MLOs) to ...

A risk-averse agent hedges her exposure to a non-tradable risk factor $U$ using a correlated traded asset $S$ and accounts for the impact of her trades on both factors. The effect of the agent's tra...

Model-free learning for multi-agent stochastic games is an active area of research. Existing reinforcement learning algorithms, however, are often restricted to zero-sum games, and are applicable on...

SREC markets are a relatively novel market-based system to incentivize the production of energy from solar means. A regulator imposes a floor on the amount of energy each regulated firm must generat...

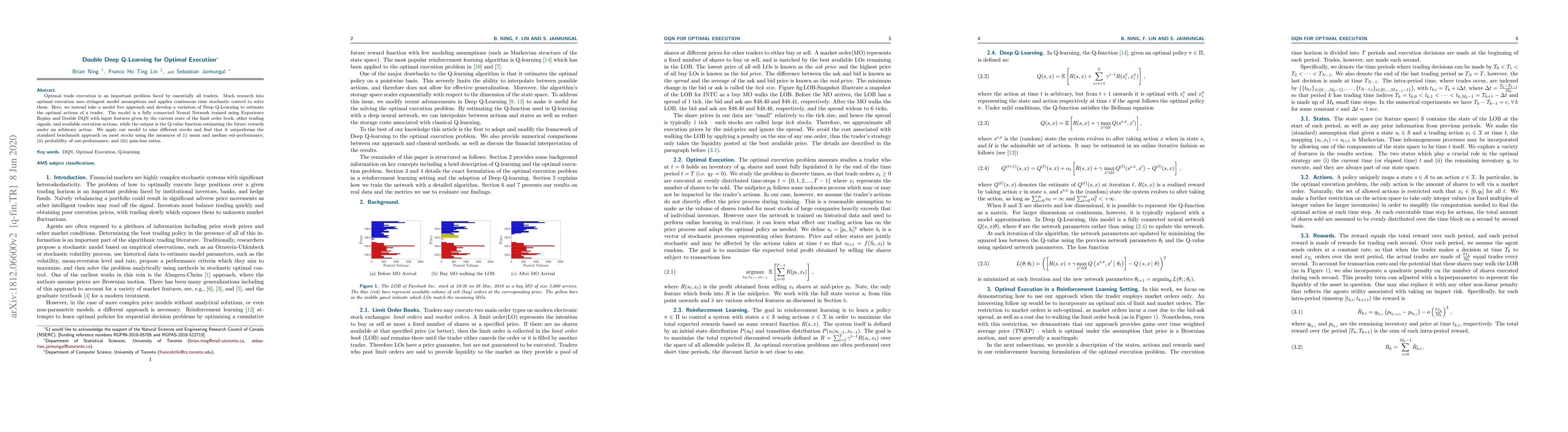

Optimal trade execution is an important problem faced by essentially all traders. Much research into optimal execution uses stringent model assumptions and applies continuous time stochastic control...

Even when confronted with the same data, agents often disagree on a model of the real-world. Here, we address the question of how interacting heterogenous agents, who disagree on what model the real...

In many stochastic games stemming from financial models, the environment evolves with latent factors and there may be common noise across agents' states. Two classic examples are: (i) multi-agent tr...

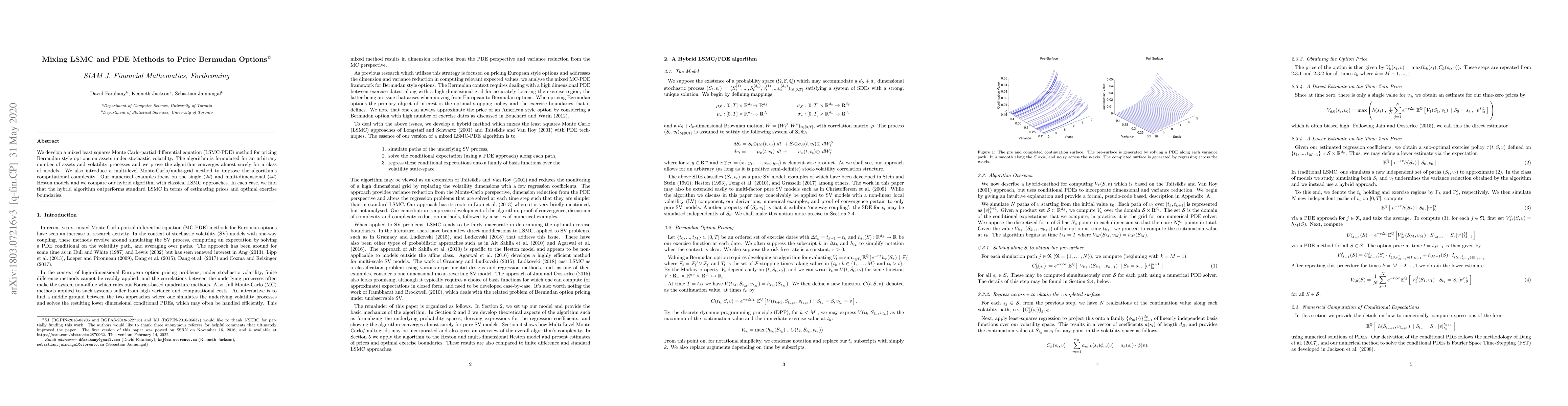

We develop a mixed least squares Monte Carlo-partial differential equation (LSMC-PDE) method for pricing Bermudan style options on assets whose volatility is stochastic. The algorithm is formulated ...

We consider the problem where an agent aims to combine the views and insights of different experts' models. Specifically, each expert proposes a diffusion process over a finite time horizon. The agent...

In a reinforcement learning (RL) setting, the agent's optimal strategy heavily depends on her risk preferences and the underlying model dynamics of the training environment. These two aspects influenc...

We study the perfect information Nash equilibrium between a broker and her clients -- an informed trader and an uniformed trader. In our model, the broker trades in the lit exchange where trades have ...

We study partial information Nash equilibrium between a broker and an informed trader. In this model, the informed trader, who possesses knowledge of a trading signal, trades multiple assets with the ...

Climate change is a major threat to the future of humanity, and its impacts are being intensified by excess man-made greenhouse gas emissions. One method governments can employ to control these emissi...

We consider the problem of an agent who faces losses over a finite time horizon and may choose to share some of these losses with a counterparty. The agent is uncertain about the true loss distributio...

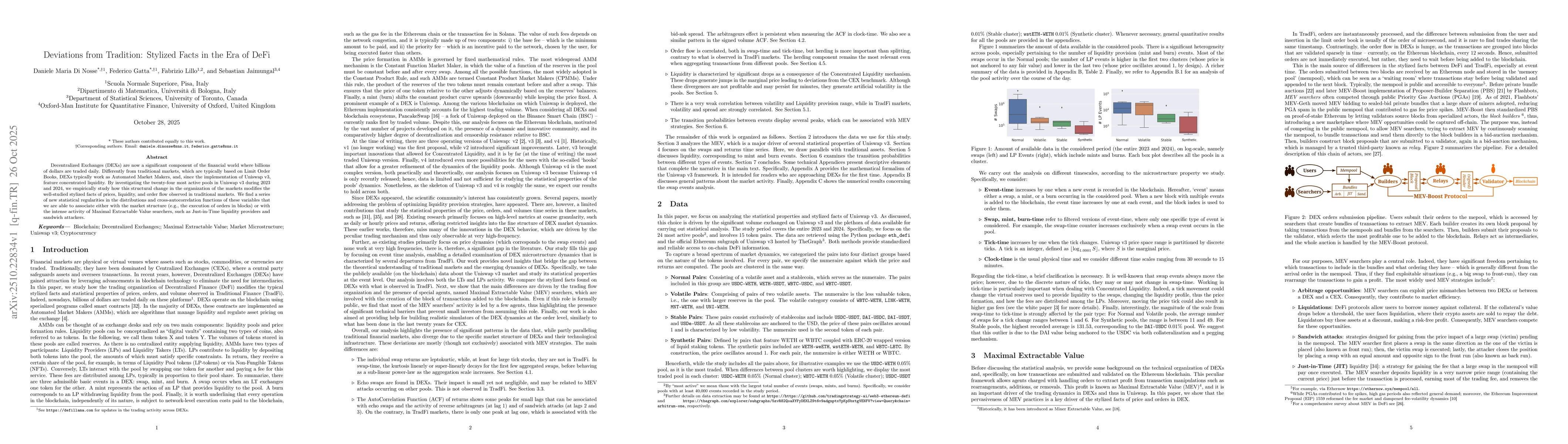

Decentralized Exchanges (DEXs) are now a significant component of the financial world where billions of dollars are traded daily. Differently from traditional markets, which are typically based on Lim...

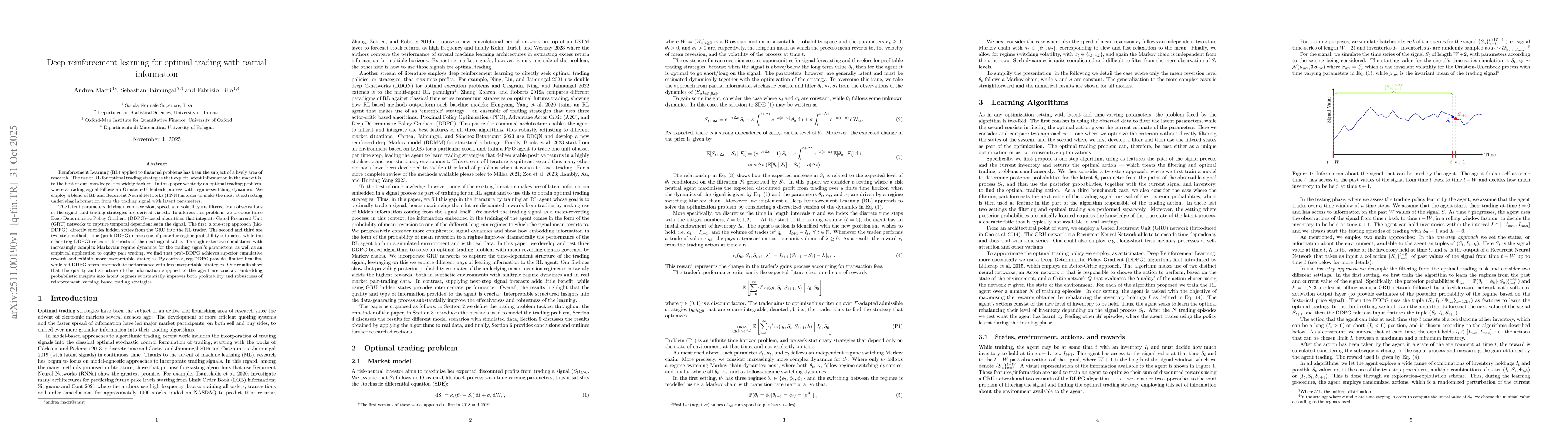

Reinforcement Learning (RL) applied to financial problems has been the subject of a lively area of research. The use of RL for optimal trading strategies that exploit latent information in the market ...

We present a novel numerical method for solving McKean-Vlasov forward-backward stochastic differential equations (MV-FBSDEs) with common noise, combining Picard iterations, elicitability and deep lear...

We develop an economic model of decentralised exchanges (DEXs) in which risk-averse liquidity providers (LPs) manage risk in a centralised exchange (CEX) based on preferences, information, and trading...