2

arXiv Papers

2

Total Publications

Profile

Academic Profile

Metrics

Statistics

2

arXiv Papers

2

Total Publications

Network

Similar Authors

Publications

Papers on arXiv

arXiv

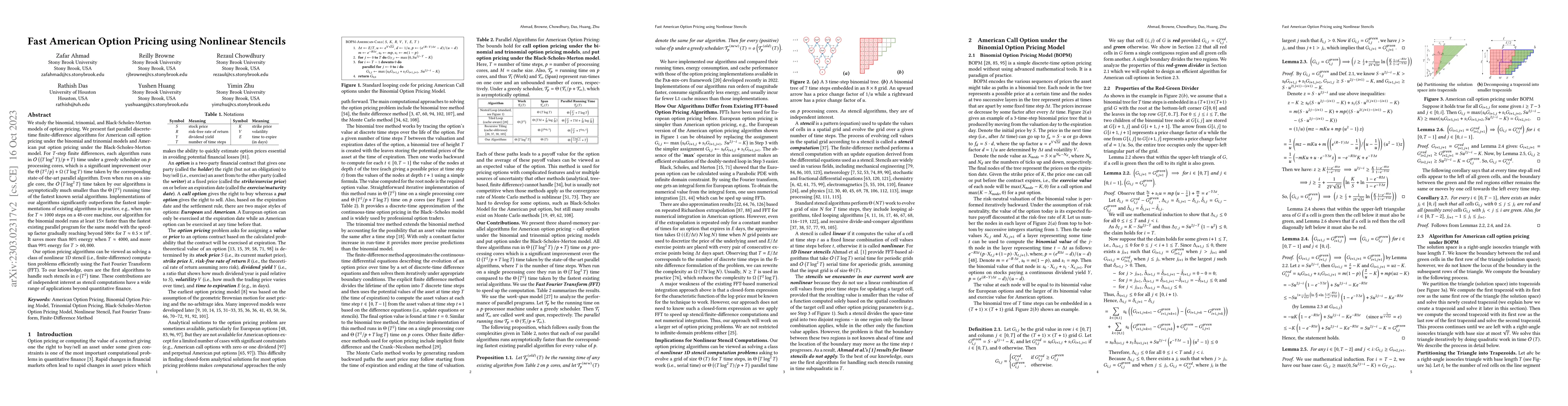

Fast American Option Pricing using Nonlinear Stencils

We study the binomial, trinomial, and Black-Scholes-Merton models of option pricing. We present fast parallel discrete-time finite-difference algorithms for American call option pricing under the bi...

arXiv

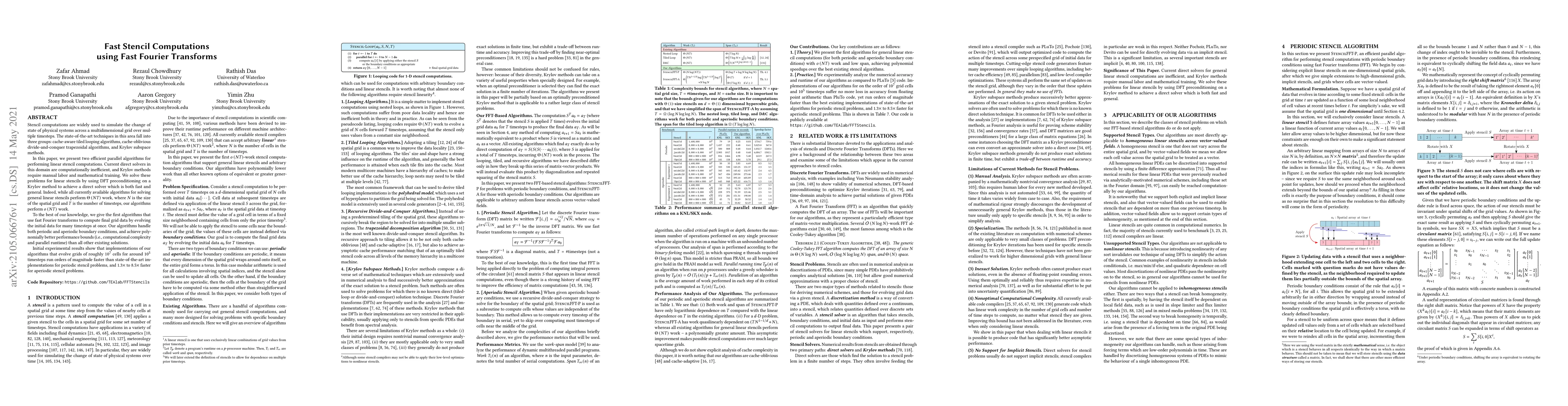

Fast Stencil Computations using Fast Fourier Transforms

Stencil computations are widely used to simulate the change of state of physical systems across a multidimensional grid over multiple timesteps. The state-of-the-art techniques in this area fall int...