Academic Profile

Statistics

Similar Authors

Papers on arXiv

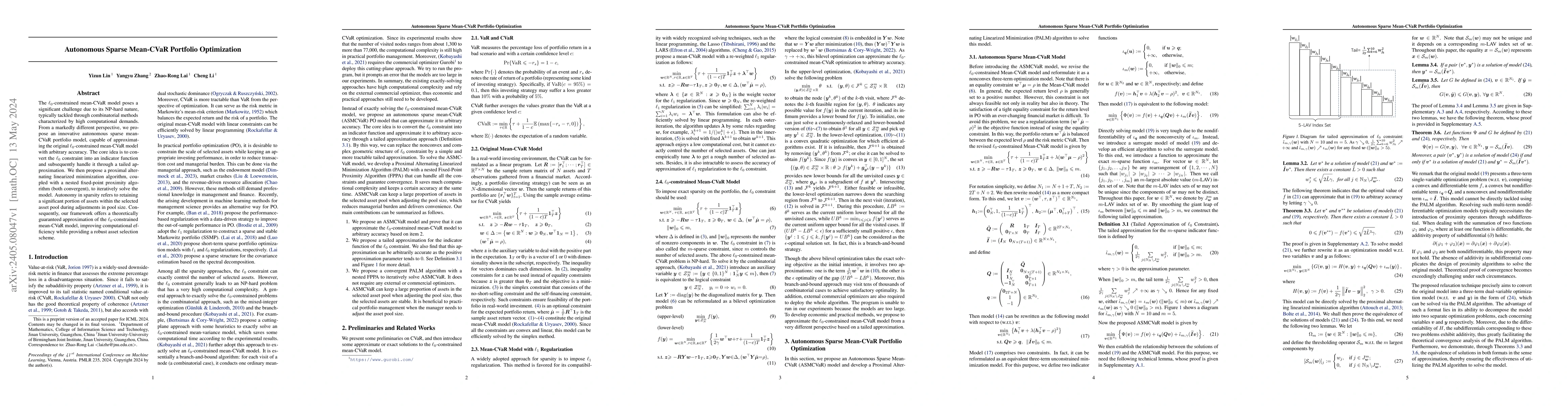

The $\ell_0$-constrained mean-CVaR model poses a significant challenge due to its NP-hard nature, typically tackled through combinatorial methods characterized by high computational demands. From a ...

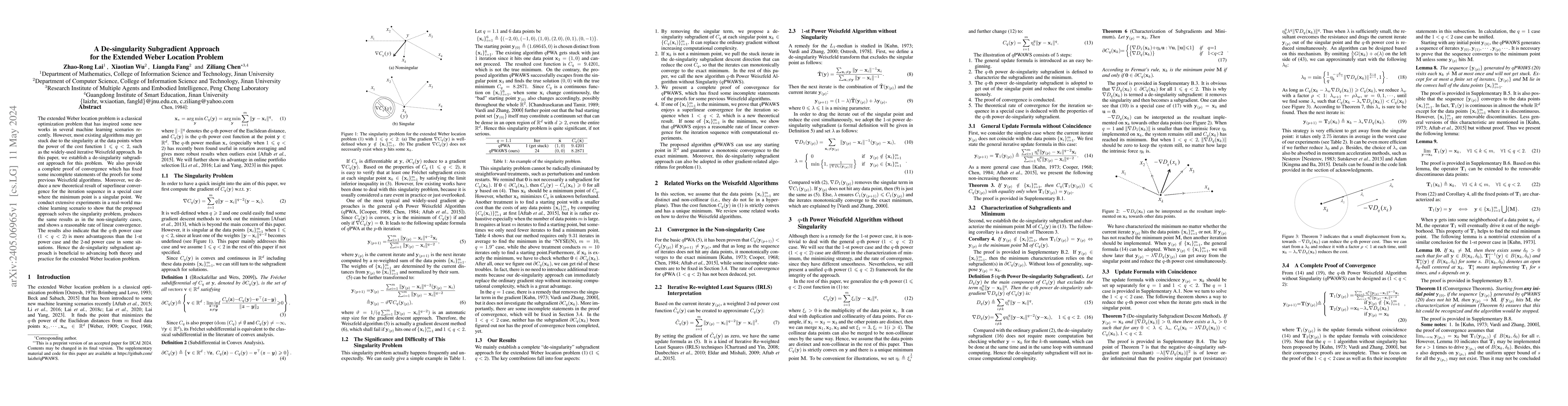

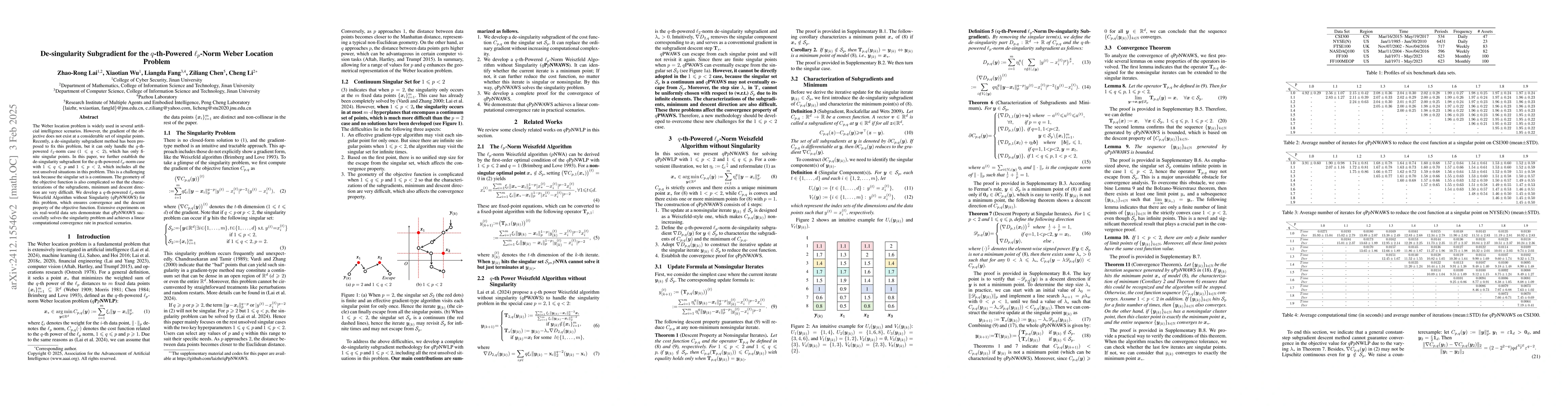

The extended Weber location problem is a classical optimization problem that has inspired some new works in several machine learning scenarios recently. However, most existing algorithms may get stu...

Invariant risk minimization (IRM) is an arising approach to generalize invariant features to different environments in machine learning. While most related works focus on new IRM settings or new app...

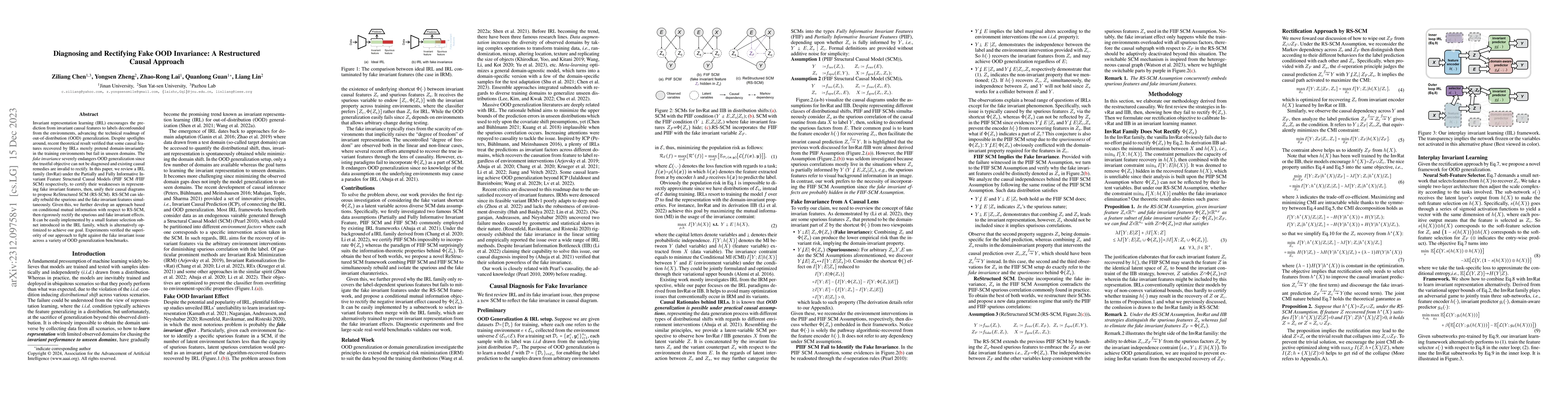

Invariant representation learning (IRL) encourages the prediction from invariant causal features to labels de-confounded from the environments, advancing the technical roadmap of out-of-distribution...

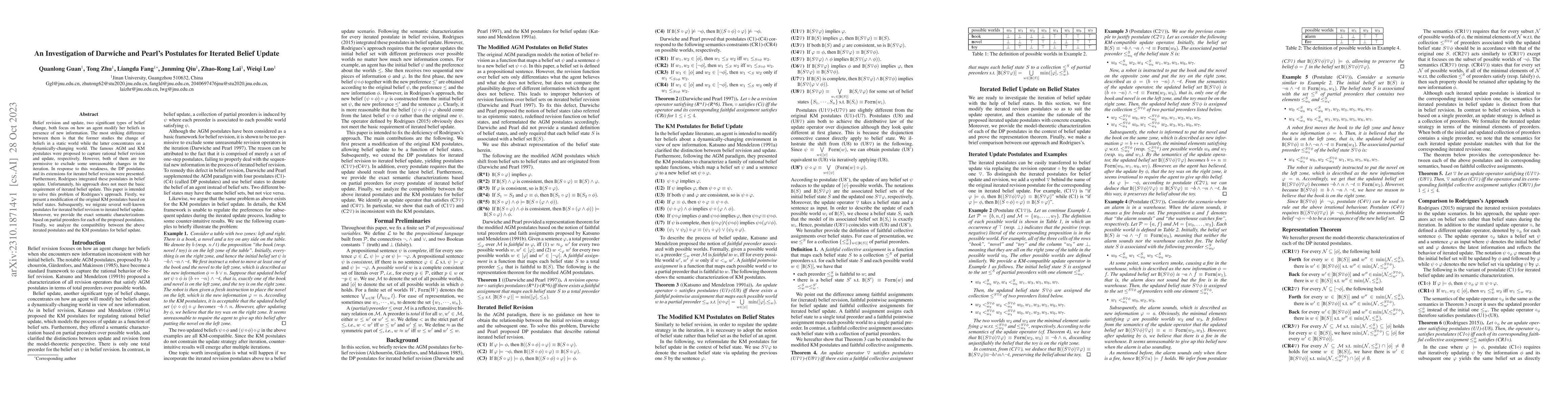

Belief revision and update, two significant types of belief change, both focus on how an agent modify her beliefs in presence of new information. The most striking difference between them is that th...

In this paper, we investigate a category of constrained fractional optimization problems that emerge in various practical applications. The objective function for this category is characterized by t...

Markowitz's criterion aims to balance expected return and risk when optimizing the portfolio. The expected return level is usually fixed according to the risk appetite of an investor, then the risk is...

The Sharpe ratio is an important and widely-used risk-adjusted return in financial engineering. In modern portfolio management, one may require an m-sparse (no more than m active assets) portfolio to ...

The Weber location problem is widely used in several artificial intelligence scenarios. However, the gradient of the objective does not exist at a considerable set of singular points. Recently, a de-s...

Invariant risk minimization is an important general machine learning framework that has recently been interpreted as a total variation model (IRM-TV). However, how to improve out-of-distribution (OOD)...

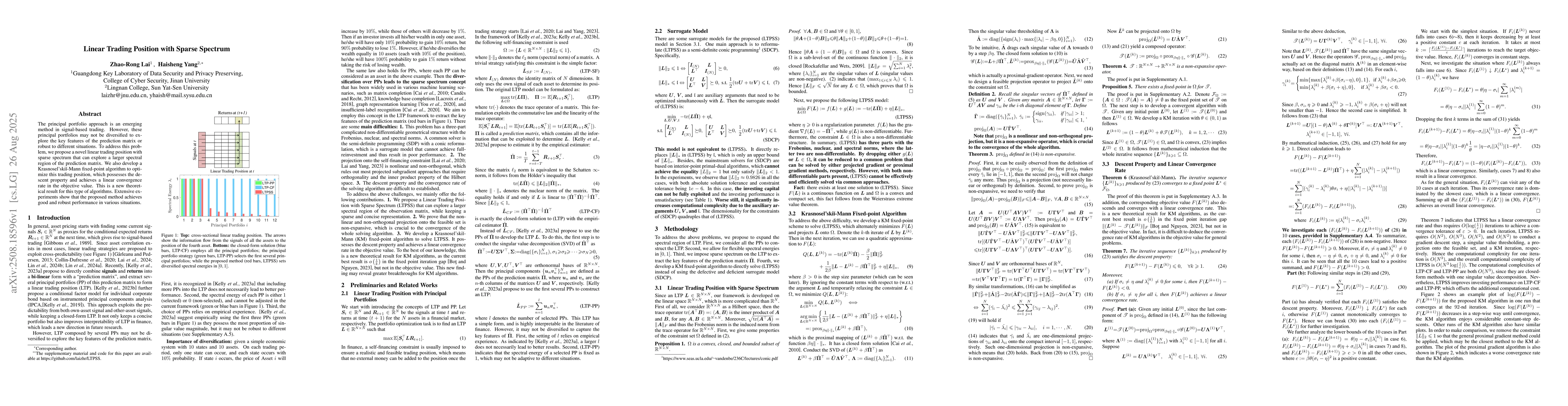

The principal portfolio approach is an emerging method in signal-based trading. However, these principal portfolios may not be diversified to explore the key features of the prediction matrix or robus...

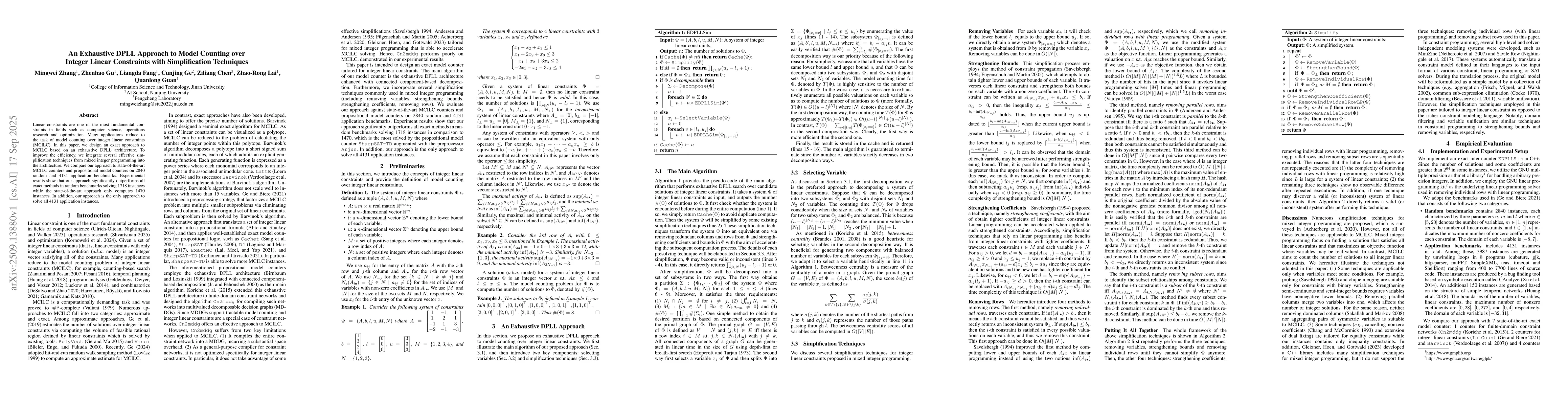

Linear constraints are one of the most fundamental constraints in fields such as computer science, operations research and optimization. Many applications reduce to the task of model counting over int...

Brain encoding models not only serve to decipher how visual stimuli are transformed into neural responses, but also represent a critical step toward visual prostheses that restore vision for patients ...