Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper addresses a key question in economic forecasting: does pure noise truly lack predictive power? Economists typically conduct variable selection to eliminate noises from predictors. Yet, we...

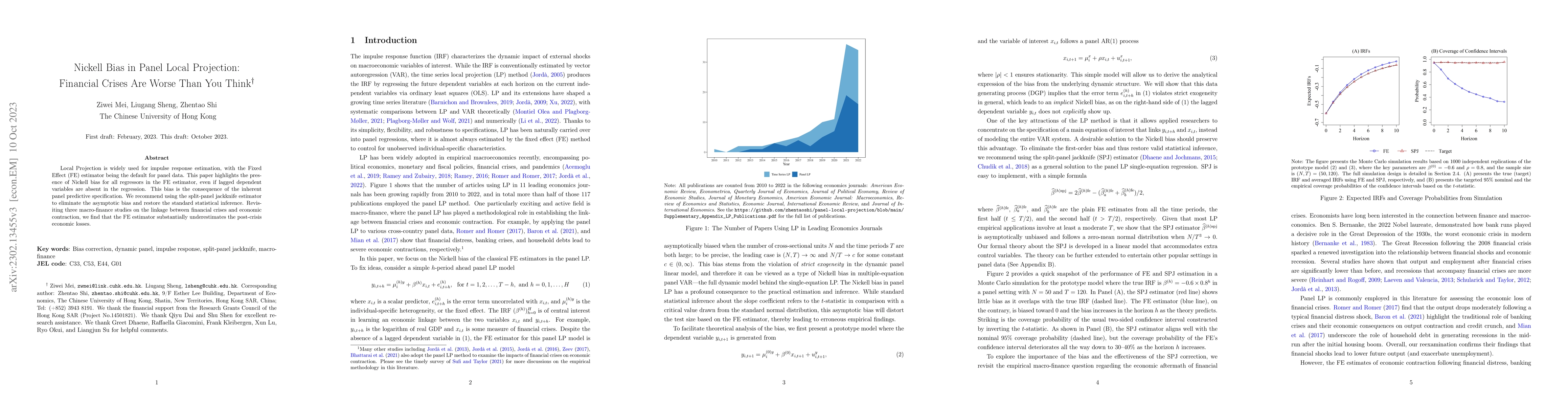

Local Projection is widely used for impulse response estimation, with the Fixed Effect (FE) estimator being the default for panel data. This paper highlights the presence of Nickell bias for all reg...

This paper examines LASSO, a widely-used $L_{1}$-penalized regression method, in high dimensional linear predictive regressions, particularly when the number of potential predictors exceeds the samp...

The global financial crisis and Covid recession have renewed discussion concerning trend-cycle discovery in macroeconomic data, and boosting has recently upgraded the popular HP filter to a modern m...

Models defined by moment conditions are at the center of structural econometric estimation, but economic theory is mostly agnostic about moment selection. While a large pool of valid moments can pot...

This paper tackles forecast combination with many forecasts or minimum variance portfolio selection with many assets. A novel convex problem called L2-relaxation is proposed. In contrast to standard...

Policy evaluation is central to economic data analysis, but economists mostly work with observational data in view of limited opportunities to carry out controlled experiments. In the potential outc...

The Hodrick-Prescott (HP) filter is one of the most widely used econometric methods in applied macroeconomic research. Like all nonparametric methods, the HP filter depends critically on a tuning pa...

Explanatory variables in a predictive regression typically exhibit low signal strength and various degrees of persistence. Variable selection in such a context is of great importance. In this paper,...

Economists specify high-dimensional models to address heterogeneity in empirical studies with complex big data. Estimation of these models calls for optimization techniques to handle a large number ...

This paper studies estimation and inference in a dyadic network formation model with observed covariates, unobserved heterogeneity, and nontransferable utilities. With the presence of the high dimensi...

In panel predictive regressions with persistent covariates, coexistence of the Nickell bias and the Stambaugh bias imposes challenges for hypothesis testing. This paper introduces a new estimator, the...

Economic and financial models -- such as vector autoregressions, local projections, and multivariate volatility models -- feature complex dynamic interactions and spillovers across many time series. T...

This paper investigates the use of synthetic control methods for causal inference in macroeconomic settings when dealing with possibly nonstationary data. While the synthetic control approach has gain...

The synthetic control method (SCM) is widely used for constructing the counterfactual of a treated unit based on data from control units in a donor pool. Allowing the donor pool contains more control ...

We leverage an ensemble of many regressors, the number of which can exceed the sample size, for economic prediction. An underlying latent factor structure implies a dense regression model with highly ...

This paper studies estimation and inference of heterogeneous peer effects featuring group fixed effects and slope heterogeneity under latent structure. We adapt the Classifier-Lasso algorithm to consi...

When the number of assets is larger than the sample size, the minimum variance portfolio interpolates the training data, delivering pathological zero in-sample variance. We show that if the weights of...