A Comprehensive Analysis of Machine Learning Models for Algorithmic Trading of Bitcoin

Publication

Metrics

AI Quick Summary

This study evaluates 41 machine learning models for Bitcoin trading, finding that Random Forest and Stochastic Gradient Descent excel in profitability and risk management amidst market volatility. The analysis uses both machine learning and trading metrics, including backtesting and forward testing, to assess model effectiveness.

Paper Preview

Abstract

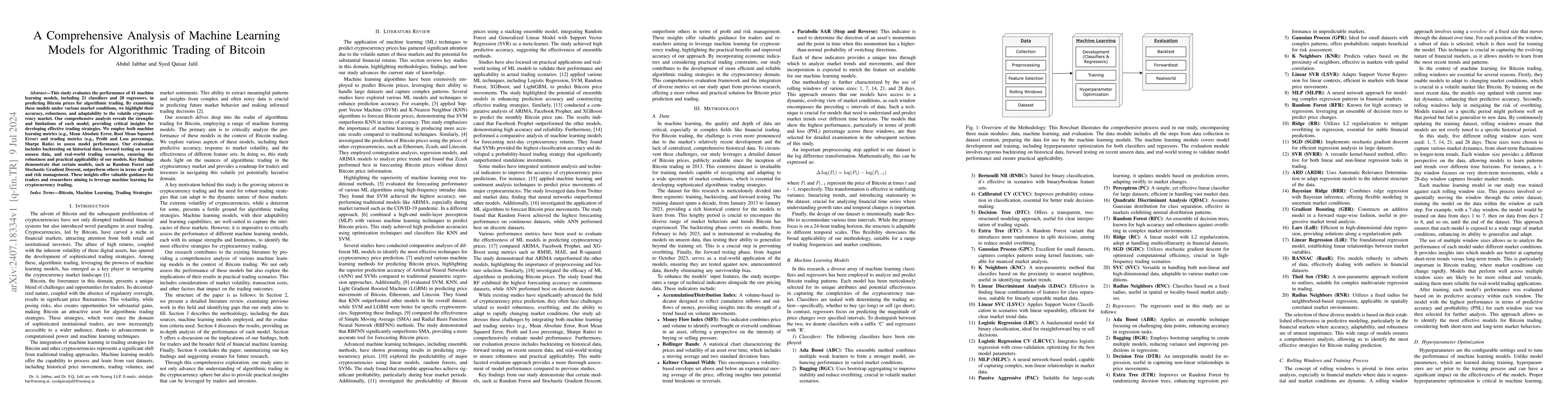

This study evaluates the performance of 41 machine learning models, including 21 classifiers and 20 regressors, in predicting Bitcoin prices for algorithmic trading. By examining these models under various market conditions, we highlight their accuracy, robustness, and adaptability to the volatile cryptocurrency market. Our comprehensive analysis reveals the strengths and limitations of each model, providing critical insights for developing effective trading strategies. We employ both machine learning metrics (e.g., Mean Absolute Error, Root Mean Squared Error) and trading metrics (e.g., Profit and Loss percentage, Sharpe Ratio) to assess model performance. Our evaluation includes backtesting on historical data, forward testing on recent unseen data, and real-world trading scenarios, ensuring the robustness and practical applicability of our models. Key findings demonstrate that certain models, such as Random Forest and Stochastic Gradient Descent, outperform others in terms of profit and risk management. These insights offer valuable guidance for traders and researchers aiming to leverage machine learning for cryptocurrency trading.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Authors

PDF Preview

Related Papers

No references found for this paper.

Discussion 0