A Framework for the Construction of a Sentiment-Driven Performance Index: The Case of DAX40

Publication

Metrics

AI Quick Summary

This research develops a sentiment-driven performance index for the DAX40 stock market by extracting sentiment from German and English news articles. The sentiment index outperforms the traditional DAX40, achieving an annualized return of 7.51% compared to 2.13%, demonstrating a more responsive reaction to real-time sentiment data.

Paper Preview

Abstract

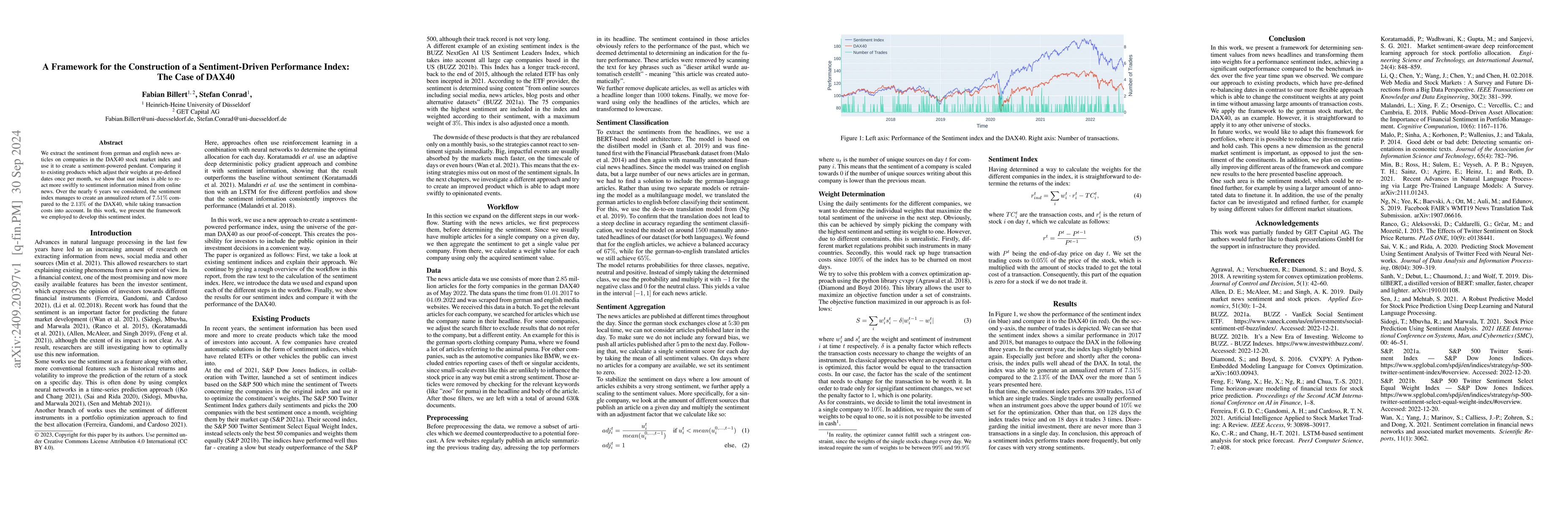

We extract the sentiment from german and english news articles on companies in the DAX40 stock market index and use it to create a sentiment-powered pendant. Comparing it to existing products which adjust their weights at pre-defined dates once per month, we show that our index is able to react more swiftly to sentiment information mined from online news. Over the nearly 6 years we considered, the sentiment index manages to create an annualized return of 7.51% compared to the 2.13% of the DAX40, while taking transaction costs into account. In this work, we present the framework we employed to develop this sentiment index.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0