Publication

Metrics

AI Quick Summary

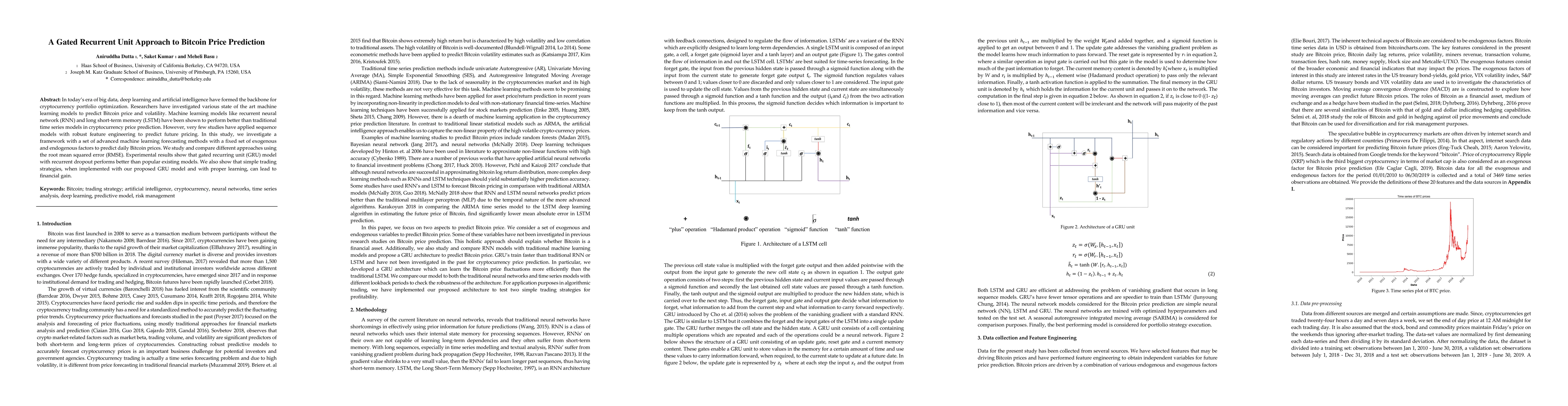

This study explores the use of Gated Recurrent Units (GRU) for predicting daily Bitcoin prices, comparing it against traditional RNN and LSTM models. Results indicate that the GRU model with recurrent dropout outperforms existing models, and simple trading strategies based on the GRU model can yield financial gains.

Paper Preview

Abstract

In today's era of big data, deep learning and artificial intelligence have formed the backbone for cryptocurrency portfolio optimization. Researchers have investigated various state of the art machine learning models to predict Bitcoin price and volatility. Machine learning models like recurrent neural network (RNN) and long short-term memory (LSTM) have been shown to perform better than traditional time series models in cryptocurrency price prediction. However, very few studies have applied sequence models with robust feature engineering to predict future pricing. in this study, we investigate a framework with a set of advanced machine learning methods with a fixed set of exogenous and endogenous factors to predict daily Bitcoin prices. We study and compare different approaches using the root mean squared error (RMSE). Experimental results show that gated recurring unit (GRU) model with recurrent dropout performs better better than popular existing models. We also show that simple trading strategies, when implemented with our proposed GRU model and with proper learning, can lead to financial gain.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0