Publication

Metrics

AI Quick Summary

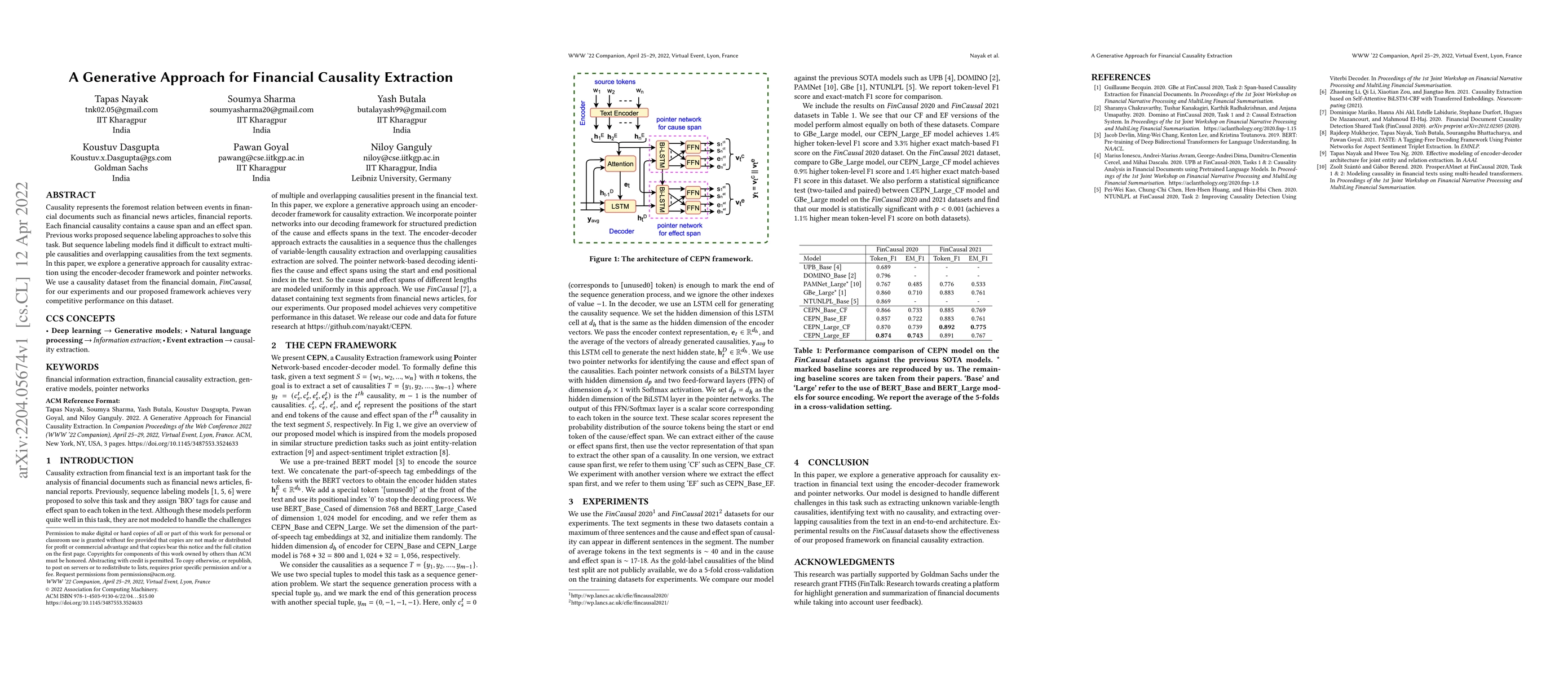

This paper proposes a generative approach using an encoder-decoder framework and pointer networks for extracting financial causalities, addressing the limitations of sequence labeling models in handling multiple and overlapping causalities. The method is tested on the \textit{FinCausal} dataset, demonstrating competitive performance.

Paper Preview

Abstract

Causality represents the foremost relation between events in financial documents such as financial news articles, financial reports. Each financial causality contains a cause span and an effect span. Previous works proposed sequence labeling approaches to solve this task. But sequence labeling models find it difficult to extract multiple causalities and overlapping causalities from the text segments. In this paper, we explore a generative approach for causality extraction using the encoder-decoder framework and pointer networks. We use a causality dataset from the financial domain, \textit{FinCausal}, for our experiments and our proposed framework achieves very competitive performance on this dataset.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0