A network and machine learning approach to detect Value Added Tax fraud

Publication

Metrics

AI Quick Summary

This paper proposes machine learning algorithms to detect VAT fraud by leveraging the network structure of VAT transactions. The method combines a Laplacian matrix with scalable machine learning techniques, achieving a 50% detection rate on Bulgarian VAT data, outperforming traditional methods.

Paper Preview

Abstract

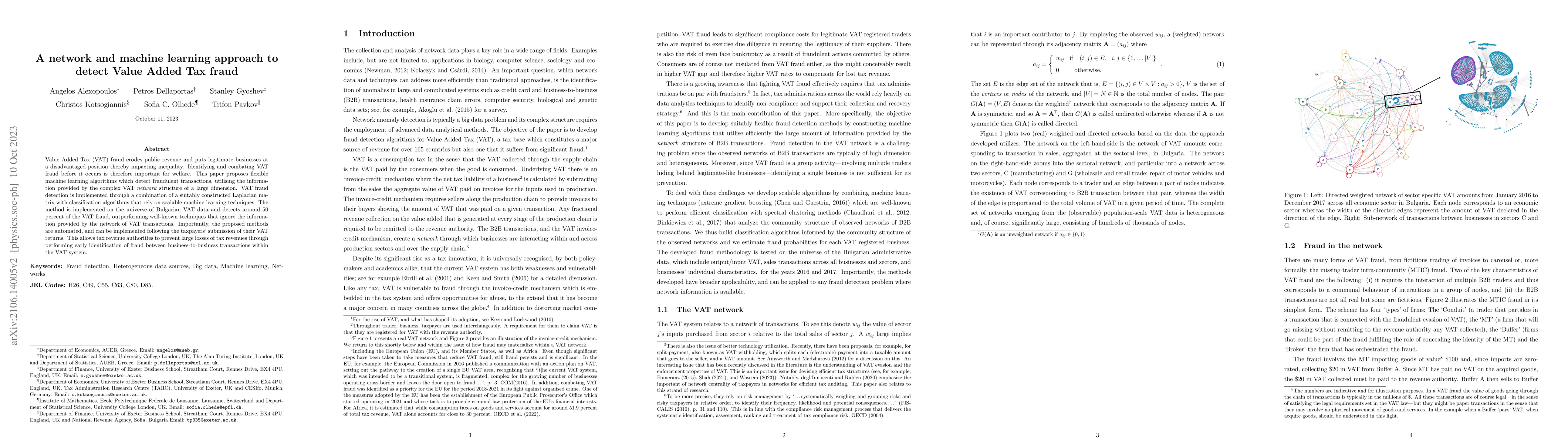

Value Added Tax (VAT) fraud erodes public revenue and puts legitimate businesses at a disadvantaged position thereby impacting inequality. Identifying and combating VAT fraud before it occurs is therefore important for welfare. This paper proposes flexible machine learning algorithms which detect fraudulent transactions, utilising the information provided by the complex VAT network structure of a large dimension. VAT fraud detection is implemented through a combination of a suitably constructed Laplacian matrix with classification algorithms that rely on scalable machine learning techniques. The method is implemented on the universe of Bulgarian VAT data and detects around 50 percent of the VAT fraud, outperforming well-known techniques that ignore the information provided by the network of VAT transactions. Importantly, the proposed methods are automated, and can be implemented following the taxpayers submission of their VAT returns. This allows tax revenue authorities to prevent large losses of tax revenues through performing early identification of fraud between business-to-business transactions within the VAT system.

AI Key Findings — Processing

Key findings are being generated. Please check back in a few minutes.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0