Publication

Metrics

AI Quick Summary

This paper proposes an agent-based simulation of an OTC market with market makers and two types of investor agents: trend investors using deep learning and value investors using static price targets. The model’s network topology reveals insights into market dynamics, including fragmentation and arbitrage opportunities, and aligns well with real-world market behaviors.

Paper Preview

Abstract

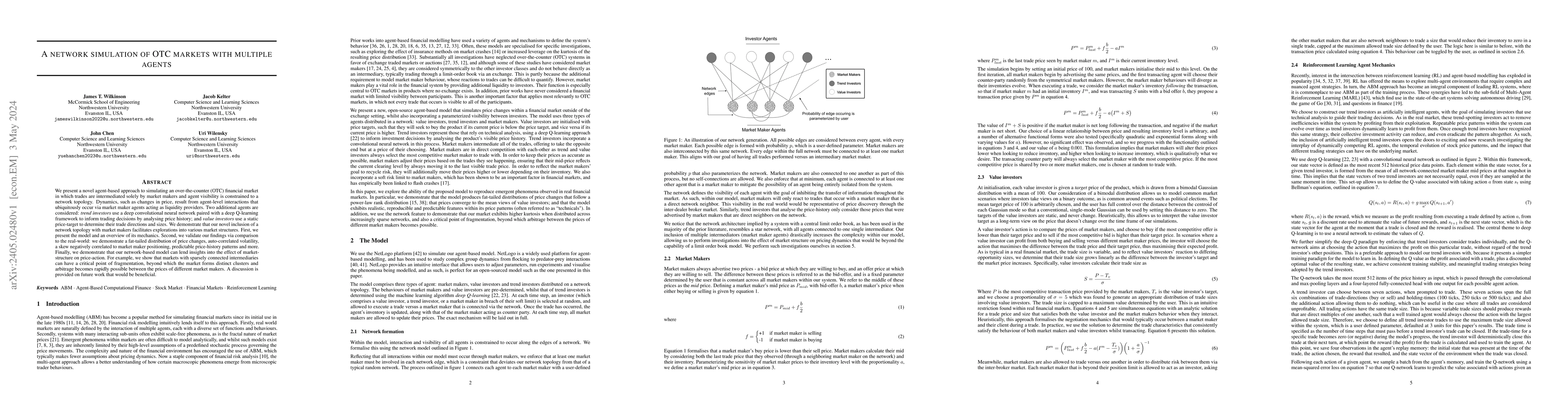

We present a novel agent-based approach to simulating an over-the-counter (OTC) financial market in which trades are intermediated solely by market makers and agent visibility is constrained to a network topology. Dynamics, such as changes in price, result from agent-level interactions that ubiquitously occur via market maker agents acting as liquidity providers. Two additional agents are considered: trend investors use a deep convolutional neural network paired with a deep Q-learning framework to inform trading decisions by analysing price history; and value investors use a static price-target to determine their trade directions and sizes. We demonstrate that our novel inclusion of a network topology with market makers facilitates explorations into various market structures. First, we present the model and an overview of its mechanics. Second, we validate our findings via comparison to the real-world: we demonstrate a fat-tailed distribution of price changes, auto-correlated volatility, a skew negatively correlated to market maker positioning, predictable price-history patterns and more. Finally, we demonstrate that our network-based model can lend insights into the effect of market-structure on price-action. For example, we show that markets with sparsely connected intermediaries can have a critical point of fragmentation, beyond which the market forms distinct clusters and arbitrage becomes rapidly possible between the prices of different market makers. A discussion is provided on future work that would be beneficial.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0