A note on the CAPM with endogenously consistent market returns

Publication

Metrics

AI Quick Summary

This paper shows that in a CAPM framework where market returns are determined by equilibrium, asset expected returns are influenced by the collective risks of all assets. It concludes that the feasible range of market returns is constrained and depends on the distribution of weights in the market portfolio, with diversified markets tending to zero returns and dominated markets returning the risk-free rate.

Paper Preview

Abstract

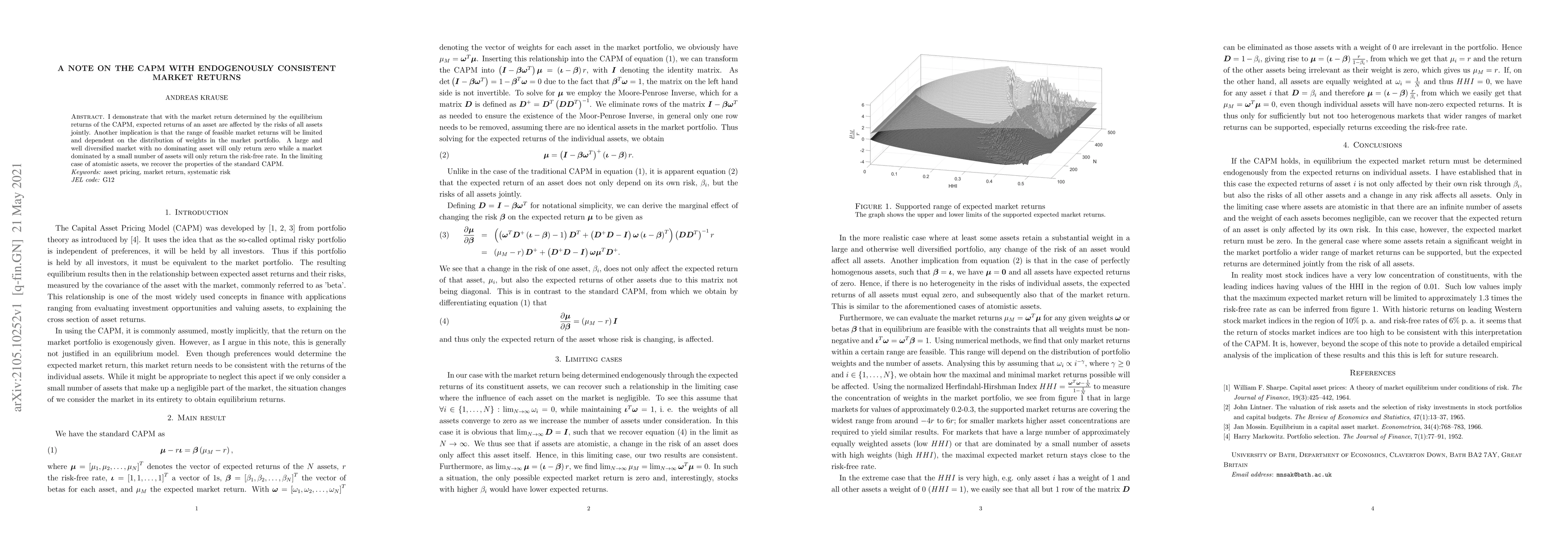

I demonstrate that with the market return determined by the equilibrium returns of the CAPM, expected returns of an asset are affected by the risks of all assets jointly. Another implication is that the range of feasible market returns will be limited and dependent on the distribution of weights in the market portfolio. A large and well diversified market with no dominating asset will only return zero while a market dominated by a small number of assets will only return the risk-free rate. In the limiting case of atomistic assets, we recover the properties of the standard CAPM.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0