In this article, we introduce a novel deep learning hybrid model that

integrates attention Transformer and Gated Recurrent Unit (GRU) architectures

to improve the accuracy of cryptocurrency price predictions. By combining the

Transformer's strength in capturing long-range patterns with the GRU's ability

to model short-term and sequential trends, the hybrid model provides a

well-rounded approach to time series forecasting. We apply the model to predict

the daily closing prices of Bitcoin and Ethereum based on historical data that

include past prices, trading volumes, and the Fear and Greed index. We evaluate

the performance of our proposed model by comparing it with four other machine

learning models: two are non-sequential feedforward models: Radial Basis

Function Network (RBFN) and General Regression Neural Network (GRNN), and two

are bidirectional sequential memory-based models: Bidirectional Long-Short-Term

Memory (BiLSTM) and Bidirectional Gated Recurrent Unit (BiGRU). The performance

of the model is assessed using several metrics, including Mean Squared Error

(MSE), Root Mean Squared Error (RMSE), Mean Absolute Error (MAE), and Mean

Absolute Percentage Error (MAPE), along with statistical validation through the

nonparametric Friedman test followed by a post hoc Wilcoxon signed rank test.

The results demonstrate that our hybrid model consistently achieves superior

accuracy, highlighting its effectiveness for financial prediction tasks. These

findings provide valuable insights for improving real-time decision making in

cryptocurrency markets and support the growing use of hybrid deep learning

models in financial analytics.

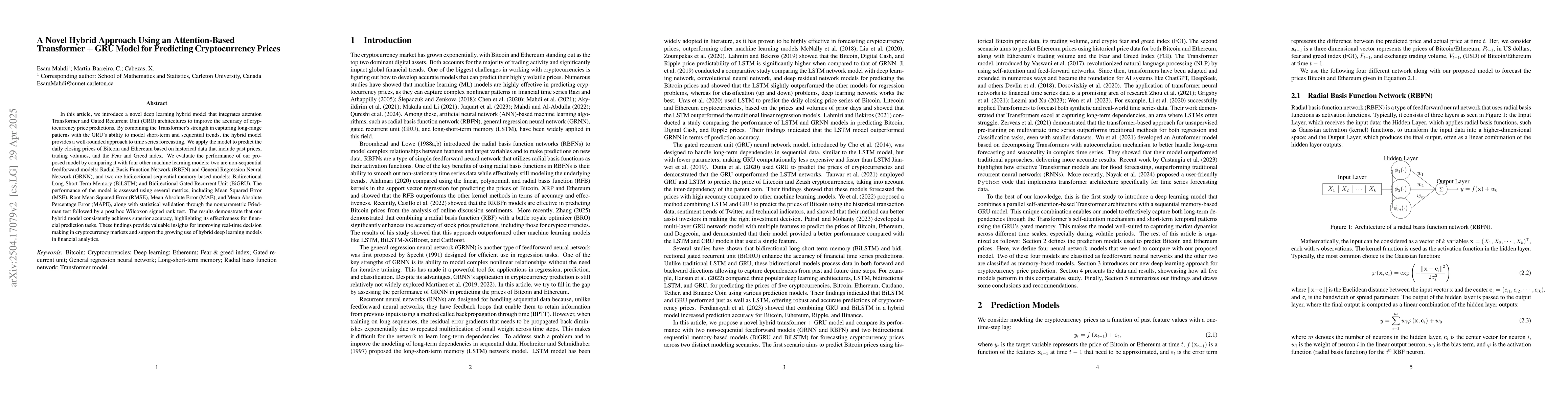

Discussion 0