Academic Profile

Statistics

Similar Authors

Papers on arXiv

This article proposes omnibus portmanteau tests for contrasting adequacy of time series models. The test statistics are based on combining the autocorrelation function of the conditional residuals, ...

A new portmanteau test statistic is proposed for detecting nonlinearity in time series data. In this paper, we elaborate on the Toeplitz autocorrelation matrix to the autocorrelation and cross-corre...

In this article, we introduce the R package portes with extensive illustrative applications. The asymptotic distributions and the Monte Carlo procedures of the most popular univariate and multivaria...

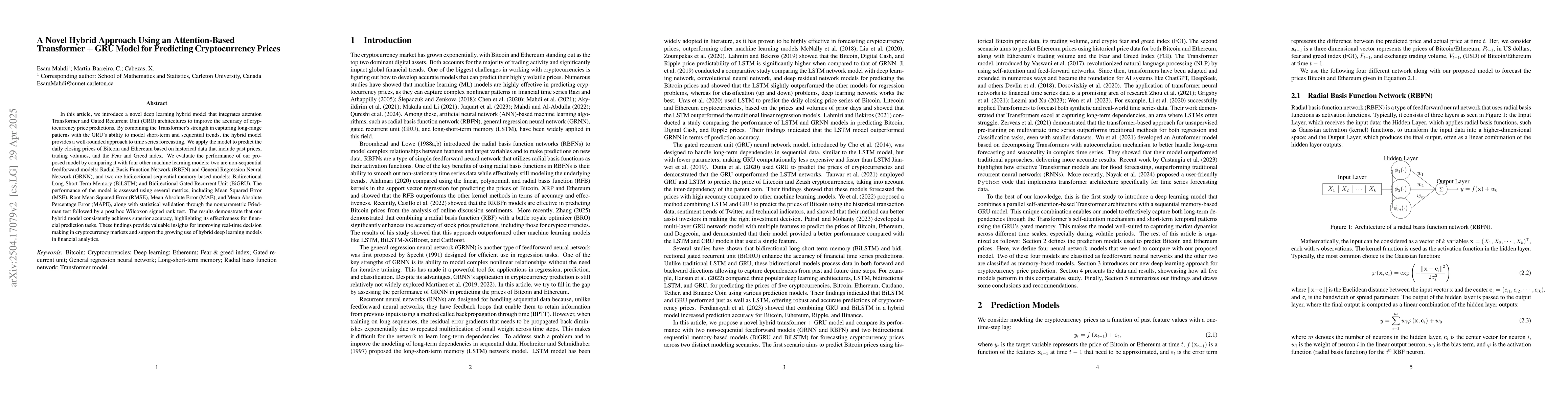

In this article, we introduce a novel deep learning hybrid model that integrates attention Transformer and Gated Recurrent Unit (GRU) architectures to improve the accuracy of cryptocurrency price pred...