A partial correlation vine based approach for modeling and forecasting multivariate volatility time-series

Publication

Metrics

Paper Preview

Abstract

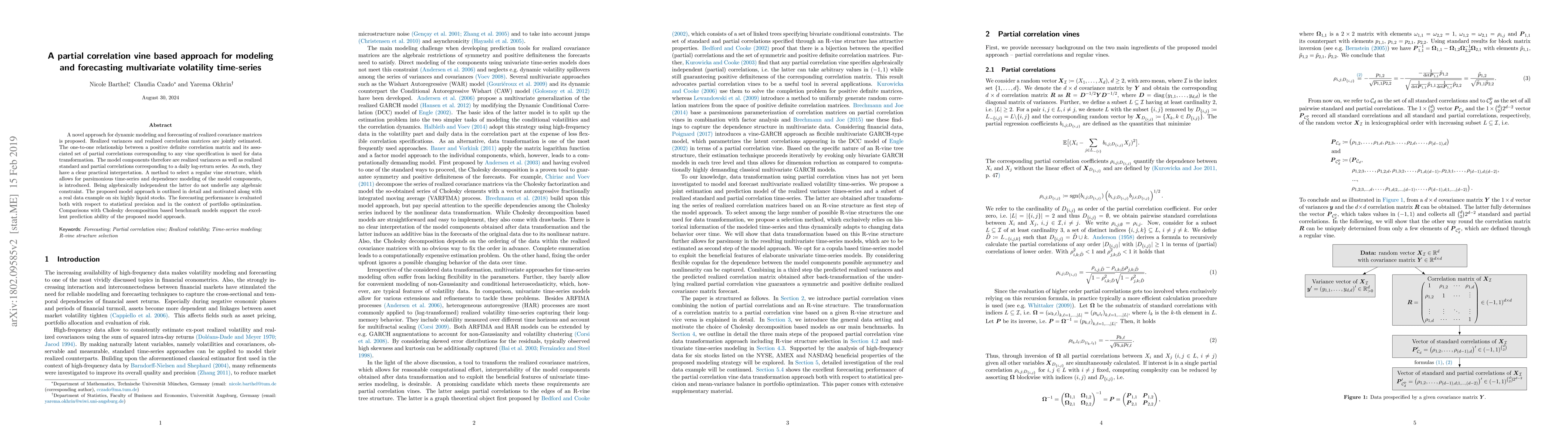

A novel approach for dynamic modeling and forecasting of realized covariance matrices is proposed. Realized variances and realized correlation matrices are jointly estimated. The one-to-one relationship between a positive definite correlation matrix and its associated set of partial correlations corresponding to any vine specification is used for data transformation. The model components therefore are realized variances as well as realized standard and partial correlations corresponding to a daily log-return series. As such, they have a clear practical interpretation. A method to select a regular vine structure, which allows for parsimonious time-series and dependence modeling of the model components, is introduced. Being algebraically independent the latter do not underlie any algebraic constraint. The proposed model approach is outlined in detail and motivated along with a real data example on six highly liquid stocks. The forecasting performance is evaluated both with respect to statistical precision and in the context of portfolio optimization. Comparisons with Cholesky decomposition based benchmark models support the excellent prediction ability of the proposed model approach.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0