It is time to move on from attempts to make the pharmacy benefit manager

(PBM) reseller business model more transparent. Time and time again the Big 3

PBMs have developed opaque alternatives to piece-meal 100% pass-through

mandates. Time and time again PBMs have demonstrated expertise in finding

loopholes in state government disclosure laws. The purpose of this paper is to

provide quantitative estimates of two transparent insurance business models as

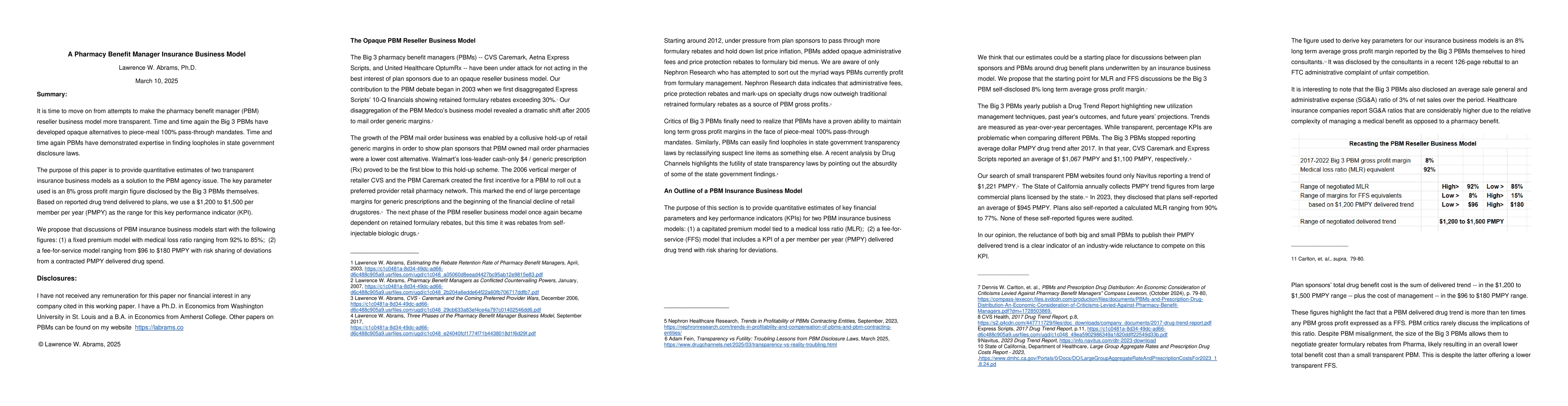

a solution to the PBM agency issue. The key parameter used is an 8% gross

profit margin figure disclosed by the Big 3 PBMs themselves. Based on reported

drug trend delivered to plans, we use a $1,200 to $1,500 per member per year

(PMPY) as the range for this key performance indicator (KPI). We propose that

discussions of PBM insurance business models start with the following figures:

(1) a fixed premium model with medical loss ratio ranging from 92% to 85%; (2)

a fee-for-service model ranging from $96 to $180 PMPY with risk sharing of

deviations from a contracted PMPY delivered drug spend.

Discussion 0