Publication

Metrics

Citations:

40

Source:

ArXiv

Paper Preview

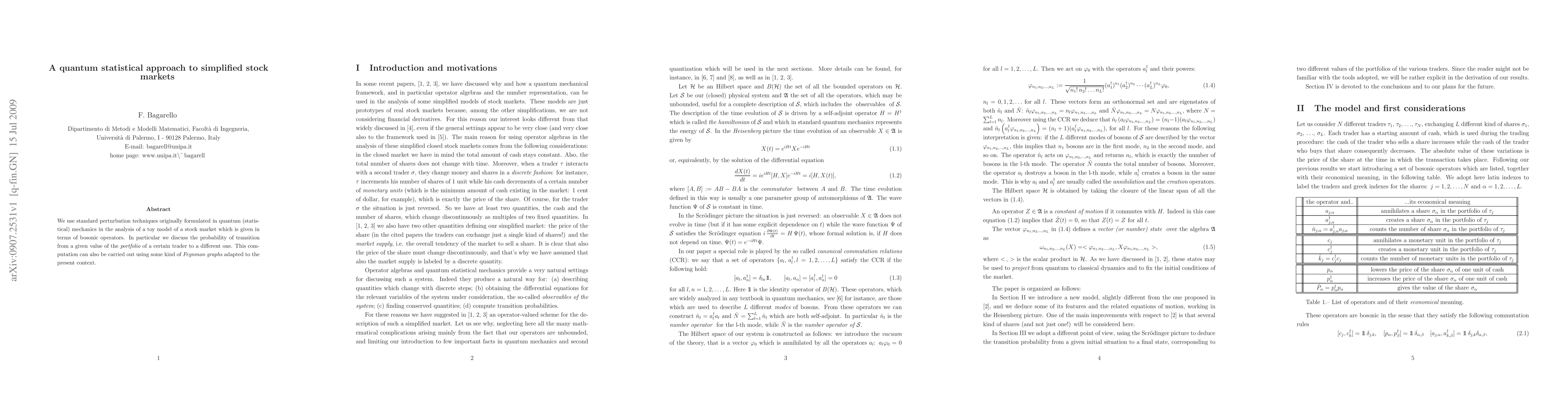

Abstract

We use standard perturbation techniques originally formulated in quantum (statistical) mechanics in the analysis of a toy model of a stock market which is given in terms of bosonic operators. In particular we discuss the probability of transition from a given value of the {\em portfolio} of a certain trader to a different one. This computation can also be carried out using some kind of {\em Feynman graphs} adapted to the present context.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

40

Citations

10

References

Paper Details

Paper ID:

0907.2531

License:

http://arxiv.org/licenses/nonexclusive-distrib/1.0/

Comments:

in press in Physica A

Categories:

q-fin.GN

PDF Preview

Key Terms

em

(0.353)

feynman

(0.243)

originally

(0.226)

adapted

(0.224)

market

(0.222)

bosonic

(0.218)

given

(0.211)

kind

(0.208)

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Current Paper

Citations

References

Click to view

Discussion 0