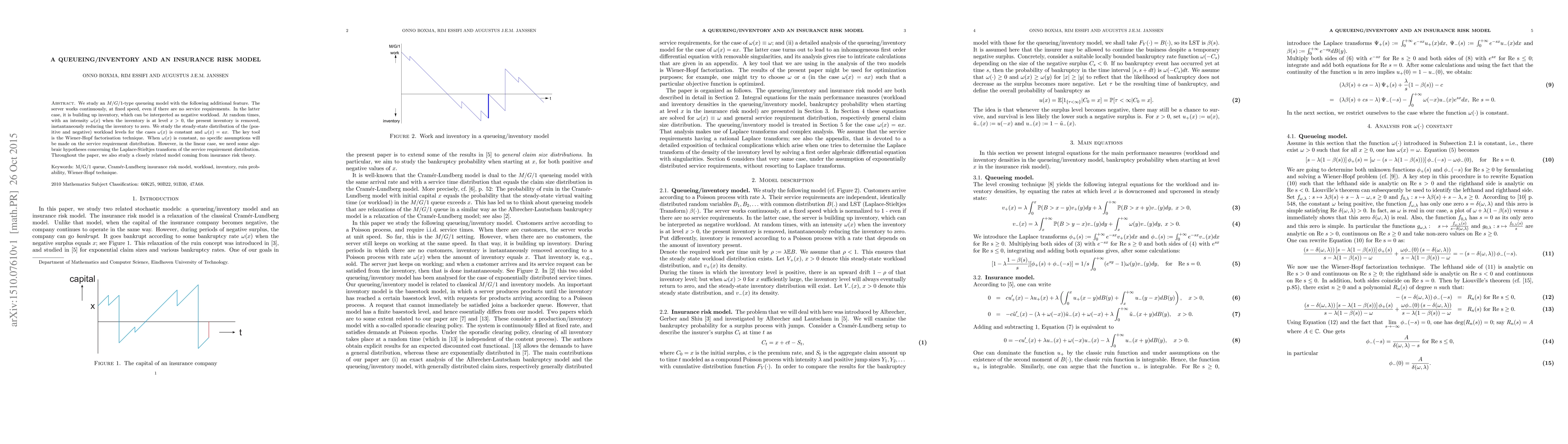

We study an M/G/1-type queueing model with the following additional feature.

The server works continuously, at fixed speed, even if there are no service

requirements. In the latter case, it is building up inventory, which can be

interpreted as negative workload. At random times, with an intensity

{\omega}(x) when the inventory is at level x > 0, the present inventory is

removed, instantaneously reducing the inventory to zero. We study the

steady-state distribution of the (positive and negative) workload levels for

the cases {\omega}(x) is constant and {\omega}(x) = ax. The key tool is the

Wiener-Hopf factorisation technique. When {\omega}(x) is constant, no specific

assumptions will be made on the service requirement distribution. However, in

the linear case, we need some algebraic hypotheses concerning the

Laplace-Stieltjes transform of the service requirement distribution. Throughout

the paper, we also study a closely related model coming from insurance risk

theory. Keywords: M/G/1 queue, Cramer-Lundberg insurance risk model, workload,

inventory, ruin probability, Wiener-Hopf technique. 2010 Mathematics Subject

Classification: 60K25, 90B22, 91B30, 47A68.

Discussion 0