A Study of Correlations in the Stock Market

Publication

Metrics

Paper Preview

Abstract

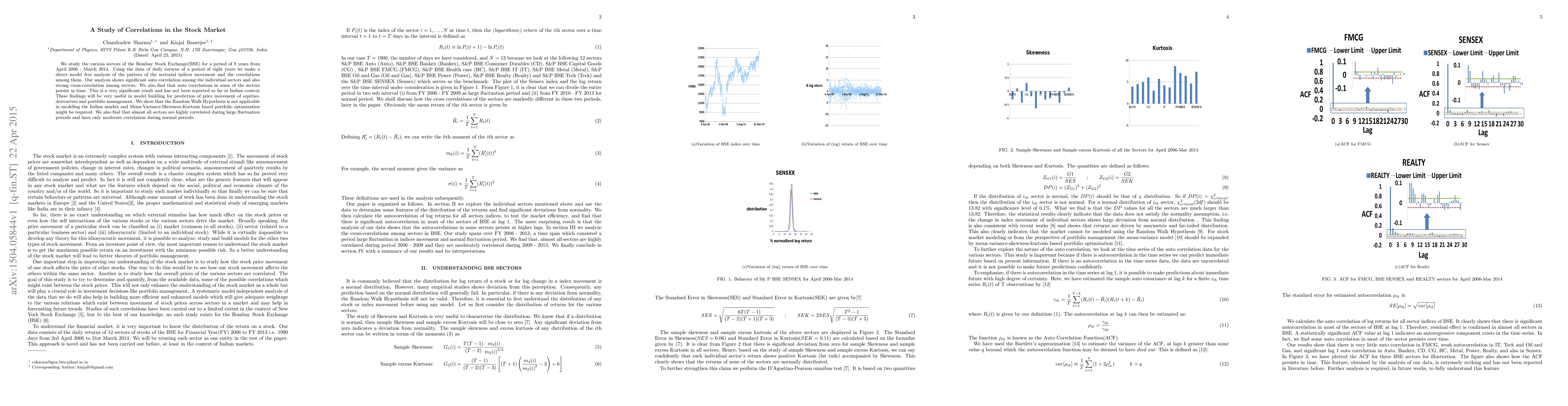

We study the various sectors of the Bombay Stock Exchange(BSE) for a period of 8 years from April 2006 - March 2014. Using the data of daily returns of a period of eight years we make a direct model free analysis of the pattern of the sectorial indices movement and the correlations among them. Our analysis shows significant auto correlation among the individual sectors and also strong cross-correlation among sectors. We also find that auto correlations in some of the sectors persist in time. This is a very significant result and has not been reported so far in Indian context These findings will be very useful in model building for prediction of price movement of equities, derivatives and portfolio management. We show that the Random Walk Hypothesis is not applicable in modeling the Indian market and Mean-Variance-Skewness-Kurtosis based portfolio optimization might be required. We also find that almost all sectors are highly correlated during large fluctuation periods and have only moderate correlation during normal periods.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0