Accelerated Portfolio Optimization with Conditional Value-at-Risk Constraints using a Cutting-Plane Method

Publication

Metrics

AI Quick Summary

This paper proposes a cutting-plane method to optimize financial portfolios under Conditional Value-at-Risk (CVaR) constraints, addressing the impracticality of large linear constraints in traditional linear programming. The method iteratively refines the solution, reducing computational time and resource usage compared to reformulation approaches.

Paper Preview

Abstract

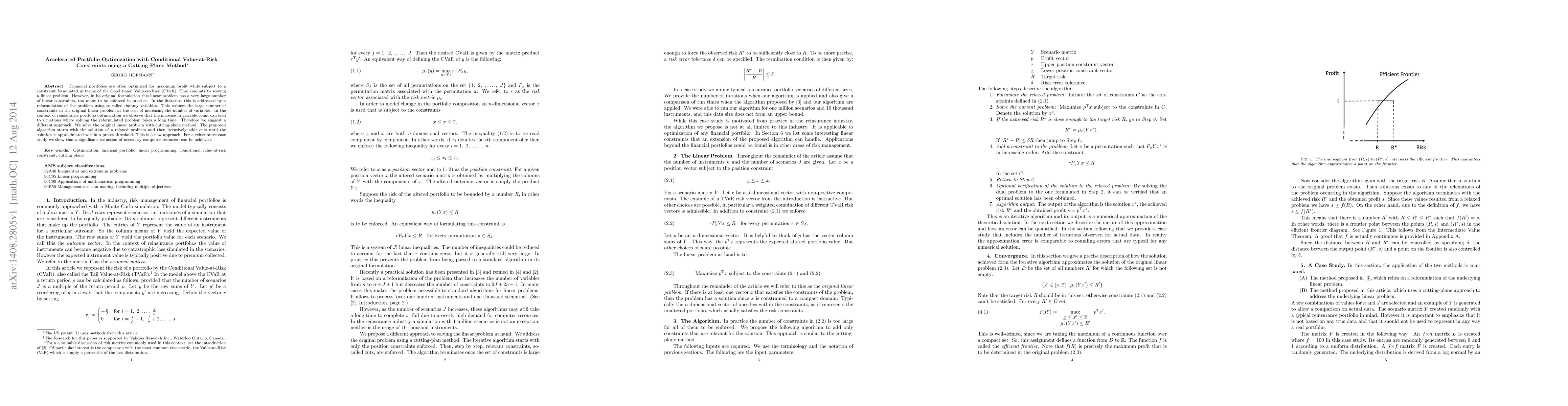

Financial portfolios are often optimized for maximum profit while subject to a constraint formulated in terms of the Conditional Value-at-Risk (CVaR). This amounts to solving a linear problem. However, in its original formulation this linear problem has a very large number of linear constraints, too many to be enforced in practice. In the literature this is addressed by a reformulation of the problem using so-called dummy variables. This reduces the large number of constraints in the original linear problem at the cost of increasing the number of variables. In the context of reinsurance portfolio optimization we observe that the increase in variable count can lead to situations where solving the reformulated problem takes a long time. Therefore we suggest a different approach. We solve the original linear problem with cutting-plane method: The proposed algorithm starts with the solution of a relaxed problem and then iteratively adds cuts until the solution is approximated within a preset threshold. This is a new approach. For a reinsurance case study we show that a significant reduction of necessary computer resources can be achieved.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0