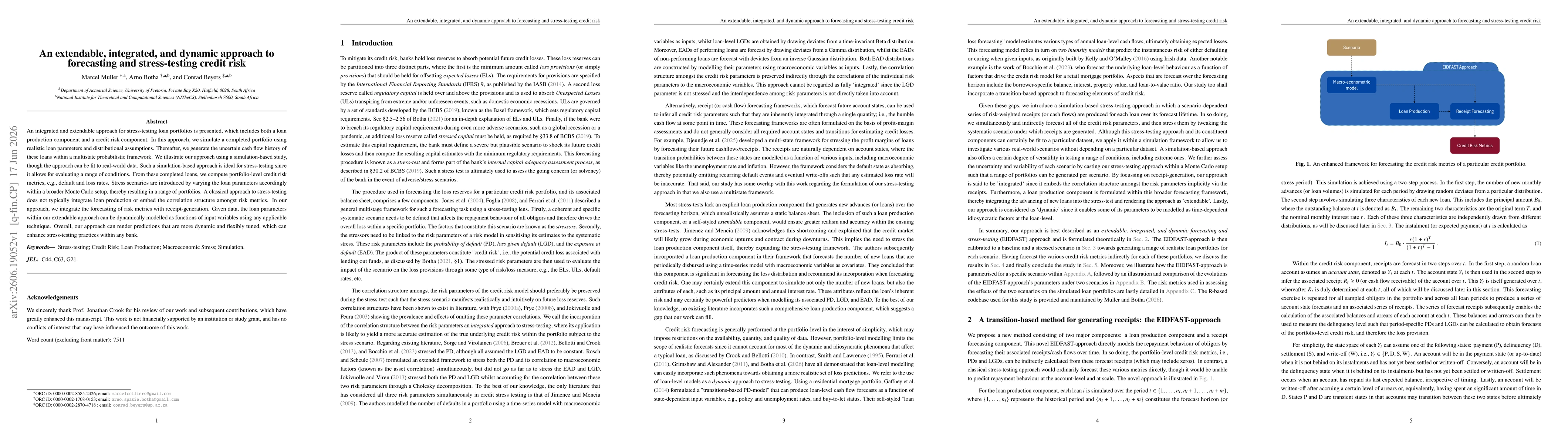

An integrated and extendable approach for stress-testing loan portfolios is presented, which includes both a loan production component and a credit risk component. In this approach, we simulate a completed portfolio using realistic loan parameters and distributional assumptions. Thereafter, we generate the uncertain cash flow history of these loans within a multistate probabilistic framework. We illustrate our approach using a simulation-based study, though the approach can be fit to real-world data. Such a simulation-based approach is ideal for stress-testing since it allows for evaluating a range of conditions. From these completed loans, we compute portfolio-level credit risk metrics, e.g., default and loss rates. Stress scenarios are introduced by varying the loan parameters accordingly within a broader Monte Carlo setup, thereby resulting in a range of portfolios. A classical approach to stress-testing does not typically integrate loan production or embed the correlation structure amongst risk metrics. In our approach, we integrate the forecasting of risk metrics with receipt-generation. Given data, the loan parameters within our extendable approach can be dynamically modelled as functions of input variables using any applicable technique. Overall, our approach can render predictions that are more dynamic and flexibly tuned, which can enhance stress-testing practices within any bank.

Discussion 0