Academic Profile

Statistics

Similar Authors

Papers on arXiv

A novel procedure is presented for finding the true but latent endpoints within the repayment histories of individual loans. The monthly observations beyond these true endpoints are false, largely d...

The IFRS 9 accounting standard requires the prediction of credit deterioration in financial instruments, i.e., significant increases in credit risk (SICR). However, the definition of such a SICR-eve...

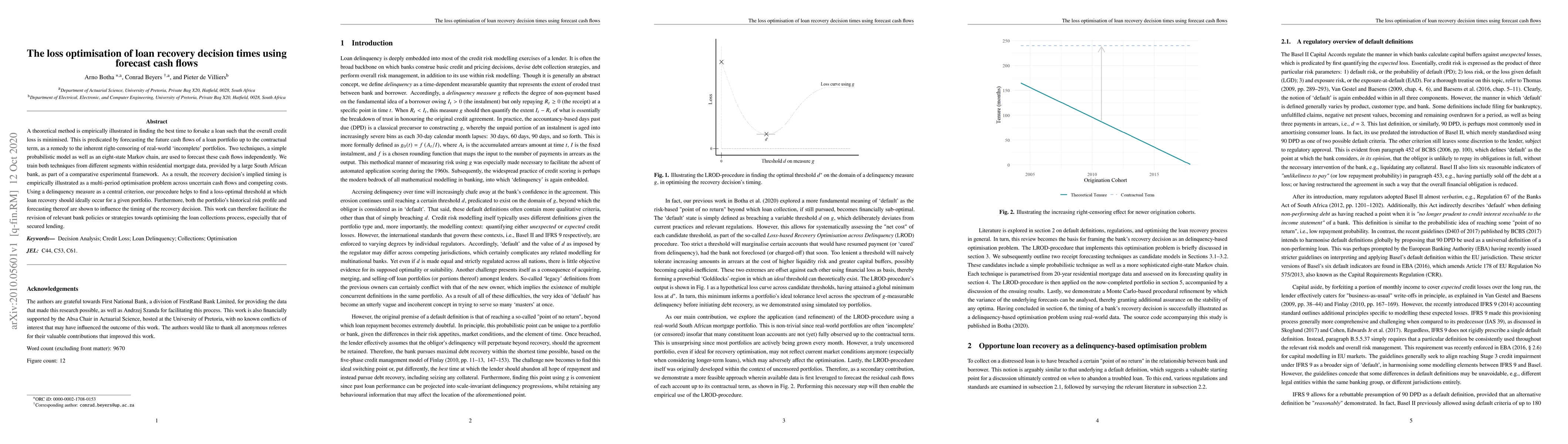

A theoretical method is empirically illustrated in finding the best time to forsake a loan such that the overall credit loss is minimised. This is predicated by forecasting the future cash flows of ...

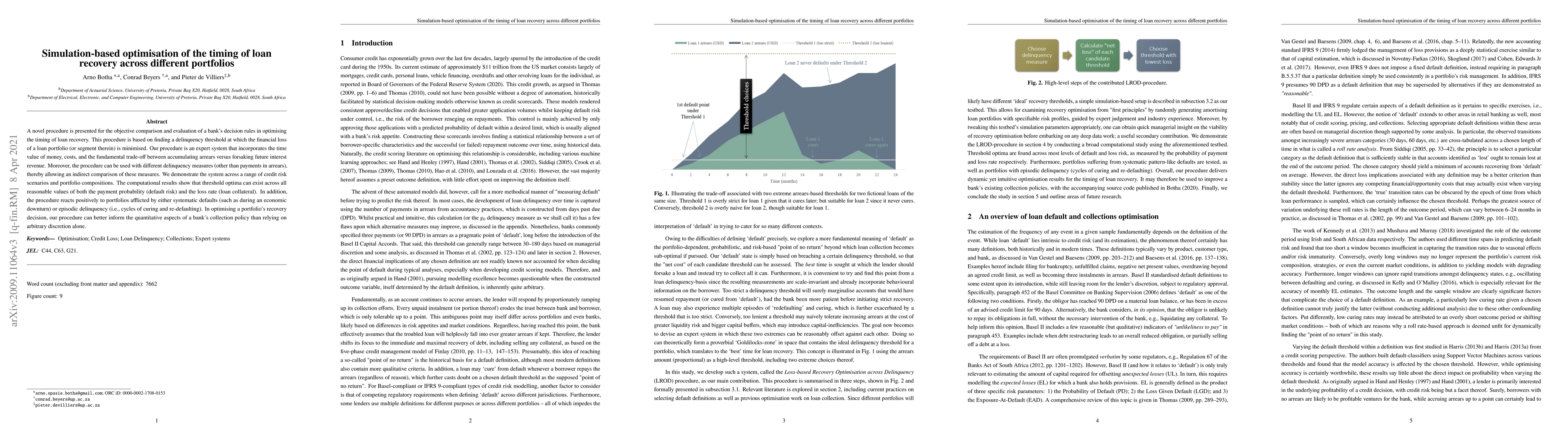

A novel procedure is presented for the objective comparison and evaluation of a bank's decision rules in optimising the timing of loan recovery. This procedure is based on finding a delinquency thre...

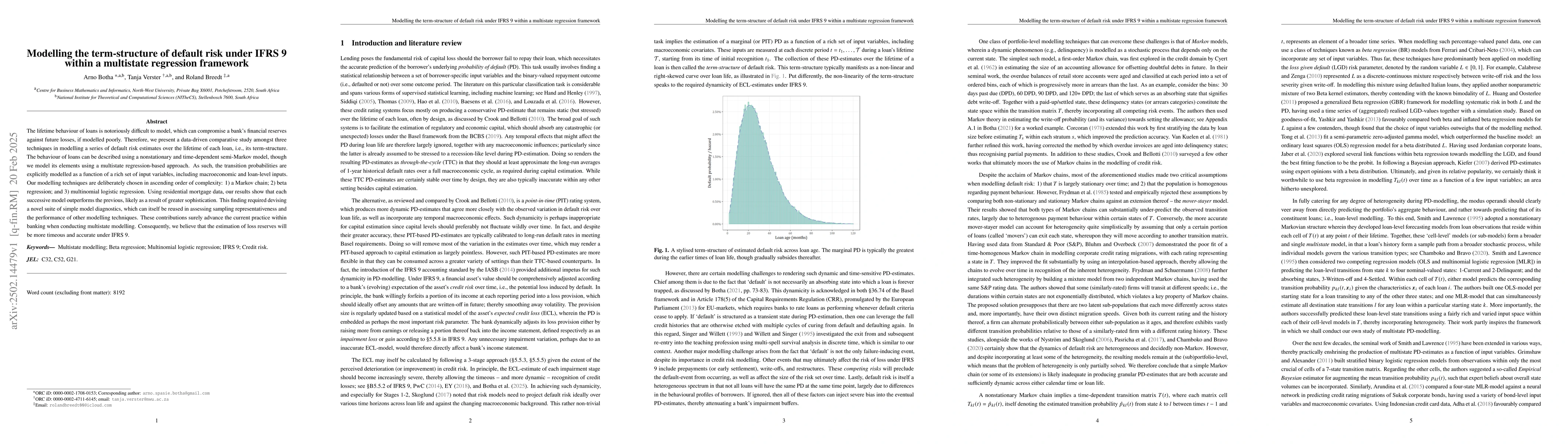

The lifetime behaviour of loans is notoriously difficult to model, which can compromise a bank's financial reserves against future losses, if modelled poorly. Therefore, we present a data-driven compa...

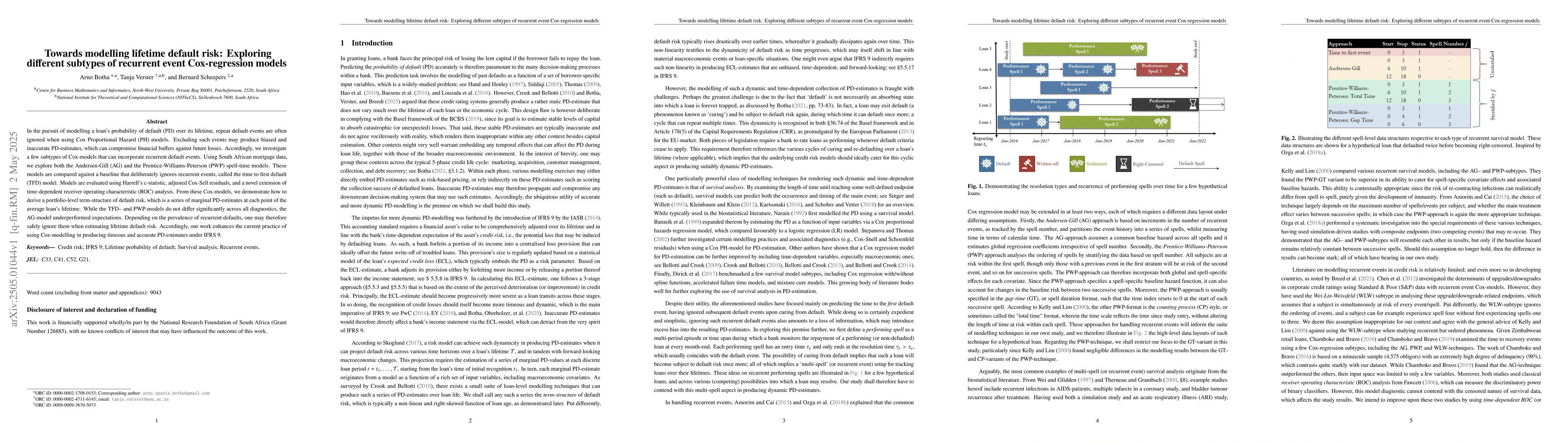

In the pursuit of modelling a loan's probability of default (PD) over its lifetime, repeat default events are often ignored when using Cox Proportional Hazard (PH) models. Excluding such events may pr...

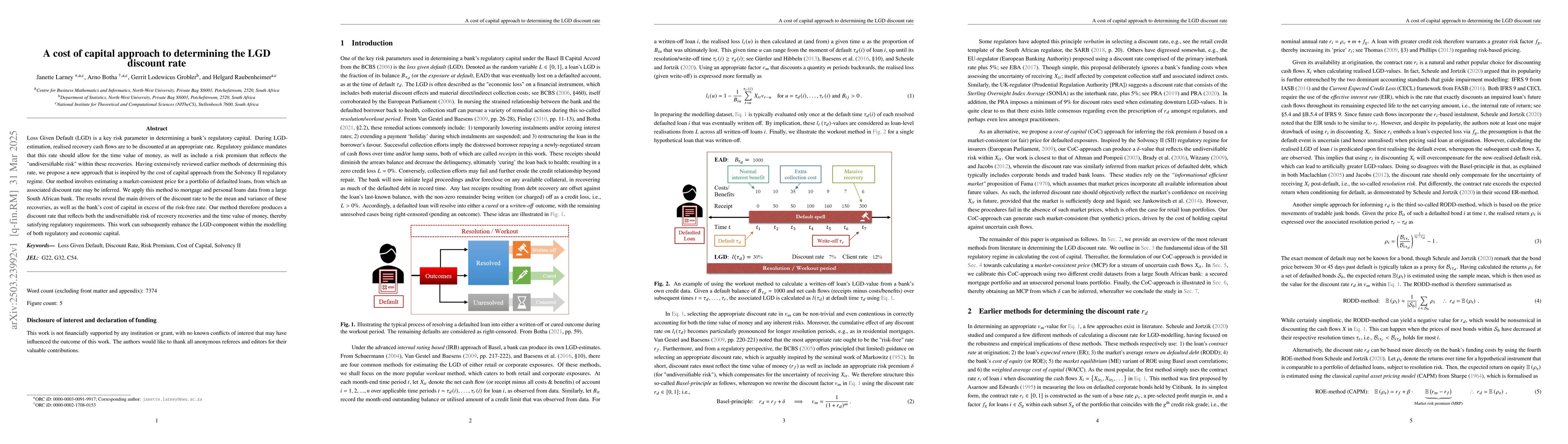

Loss Given Default (LGD) is a key risk parameter in determining a bank's regulatory capital. During LGD-estimation, realised recovery cash flows are to be discounted at an appropriate rate. Regulatory...

Under the International Financial Reporting Standards (IFRS) 9, credit losses ought to be recognised timeously and accurately. This requirement belies a certain degree of dynamicity when estimating th...

The estimation of marginal loan write-off probabilities is a non-trivial task when modelling the loss given default (LGD) risk parameter in credit risk. We explore two types of survival models in esti...

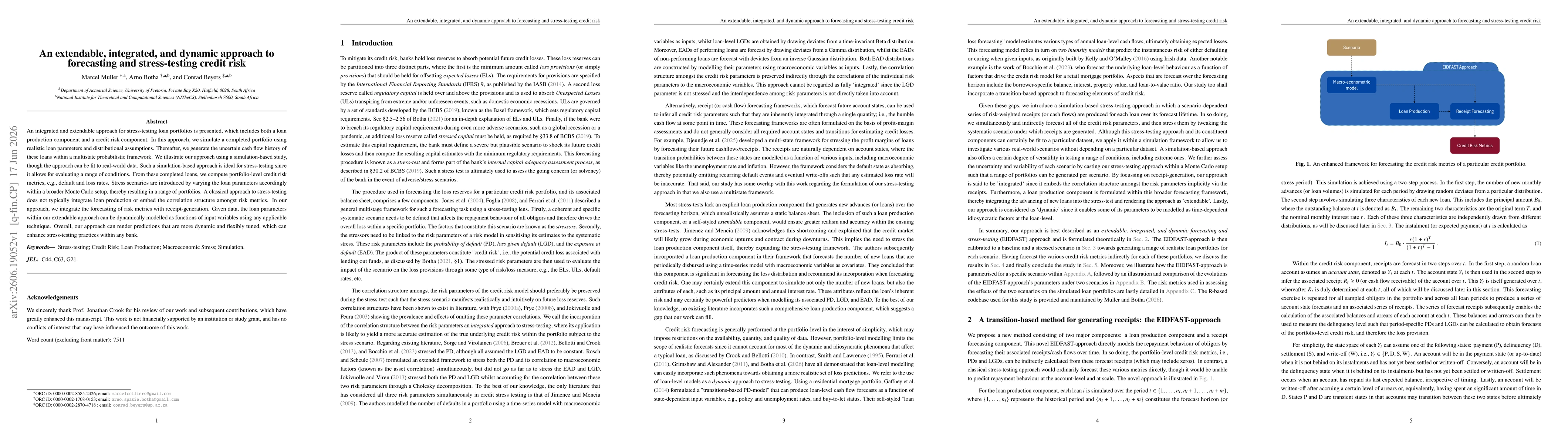

An integrated and extendable approach for stress-testing loan portfolios is presented, which includes both a loan production component and a credit risk component. In this approach, we simulate a comp...