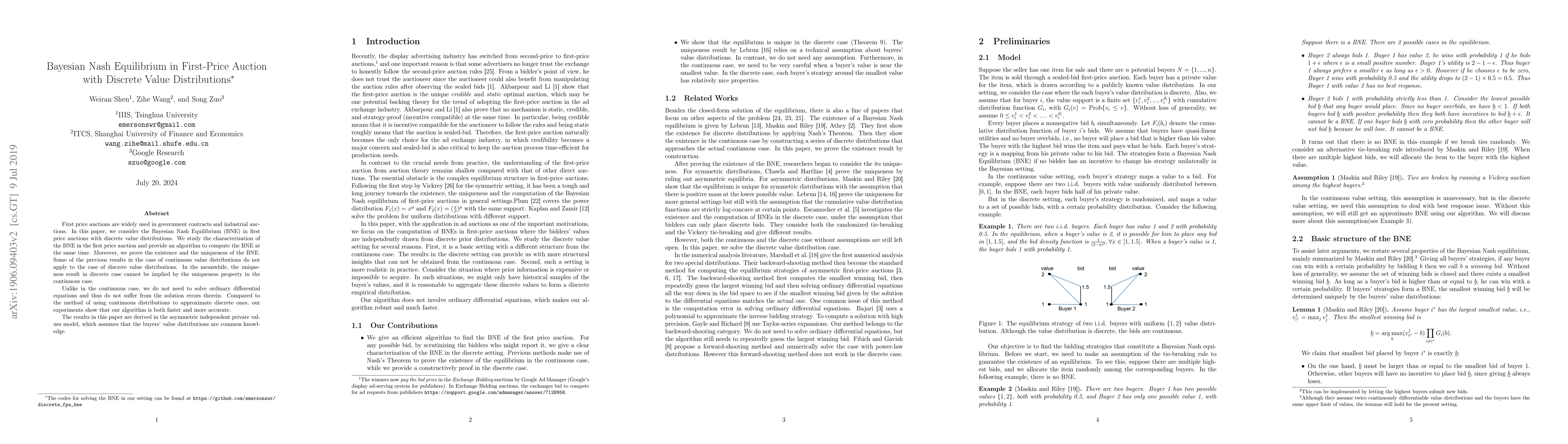

First price auctions are widely used in government contracts and industrial

auctions. In this paper, we consider the Bayesian Nash Equilibrium (BNE) in

first price auctions with discrete value distributions. We study the

characterization of the BNE in the first price auction and provide an algorithm

to compute the BNE at the same time. Moreover, we prove the existence and the

uniqueness of the BNE. Some of the previous results in the case of continuous

value distributions do not apply to the case of discrete value distributions.

In the meanwhile, the uniqueness result in discrete case cannot be implied by

the uniqueness property in the continuous case.

Unlike in the continuous case, we do not need to solve ordinary differential

equations and thus do not suffer from the solution errors therein. Compared to

the method of using continuous distributions to approximate discrete ones, our

experiments show that our algorithm is both faster and more accurate.

The results in this paper are derived in the asymmetric independent private

values model, which assumes that the buyers' value distributions are common

knowledge.

Discussion 0