Betting vs. Trading: Learning a Linear Decision Policy for Selling Wind Power and Hydrogen

Publication

Metrics

AI Quick Summary

This paper develops a linear decision policy for a hybrid power plant to optimize selling wind power and hydrogen, transitioning from an all-or-nothing 'betting' strategy to a diversified 'trading' strategy by incorporating risk constraints. The proposed method shows satisfactory performance compared to an oracle model, evaluated under different grid purchase scenarios.

Paper Preview

Abstract

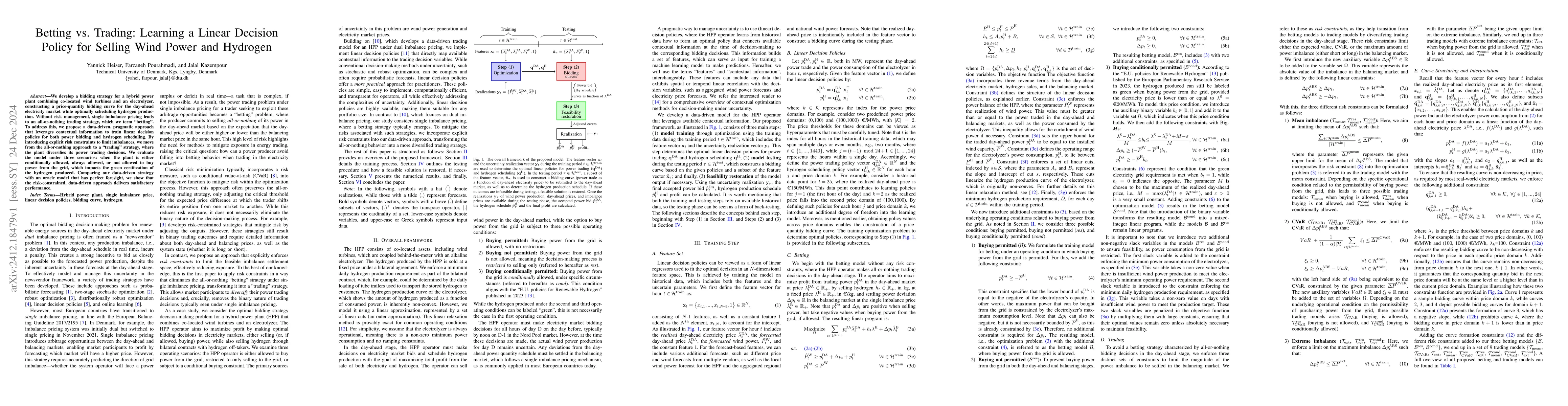

We develop a bidding strategy for a hybrid power plant combining co-located wind turbines and an electrolyzer, constructing a price-quantity bidding curve for the day-ahead electricity market while optimally scheduling hydrogen production. Without risk management, single imbalance pricing leads to an all-or-nothing trading strategy, which we term 'betting'. To address this, we propose a data-driven, pragmatic approach that leverages contextual information to train linear decision policies for both power bidding and hydrogen scheduling. By introducing explicit risk constraints to limit imbalances, we move from the all-or-nothing approach to a 'trading" strategy', where the plant diversifies its power trading decisions. We evaluate the model under three scenarios: when the plant is either conditionally allowed, always allowed, or not allowed to buy power from the grid, which impacts the green certification of the hydrogen produced. Comparing our data-driven strategy with an oracle model that has perfect foresight, we show that the risk-constrained, data-driven approach delivers satisfactory performance.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Authors

PDF Preview

Related Papers

No references found for this paper.

Discussion 0