Money laundering through insurance claims poses a threat to insurers both through fraudulent payouts and reputational and regulatory risk. Despite this, little research has examined how such laundering can be prevented. This paper examines whether machine learning can help insurers flag suspicious claims before payout, shifting the focus from passive reporting to active prevention. Using production data from a major Norwegian insurer, we train gradient-boosted decision tree models to detect claims later reported to authorities for suspected money laundering. Because fraud and laundering may share behavioural patterns, we also examine whether insurance fraud labels can serve as an auxiliary training signal. We compare different learning setups using the Budget-Weighted Capture Rate, a metric introduced in this paper to measure how many laundering cases are captured when only a small share of claims can be manually reviewed. The results show that incorporating fraud-related investigation labels substantially improves laundering detection. The best-performing model captures nearly two-thirds of laundering cases within the top-ranked 2 to 6 percent of claims selected for investigation. To our knowledge, this is the first empirical study of machine learning for money laundering detection in insurance claims.

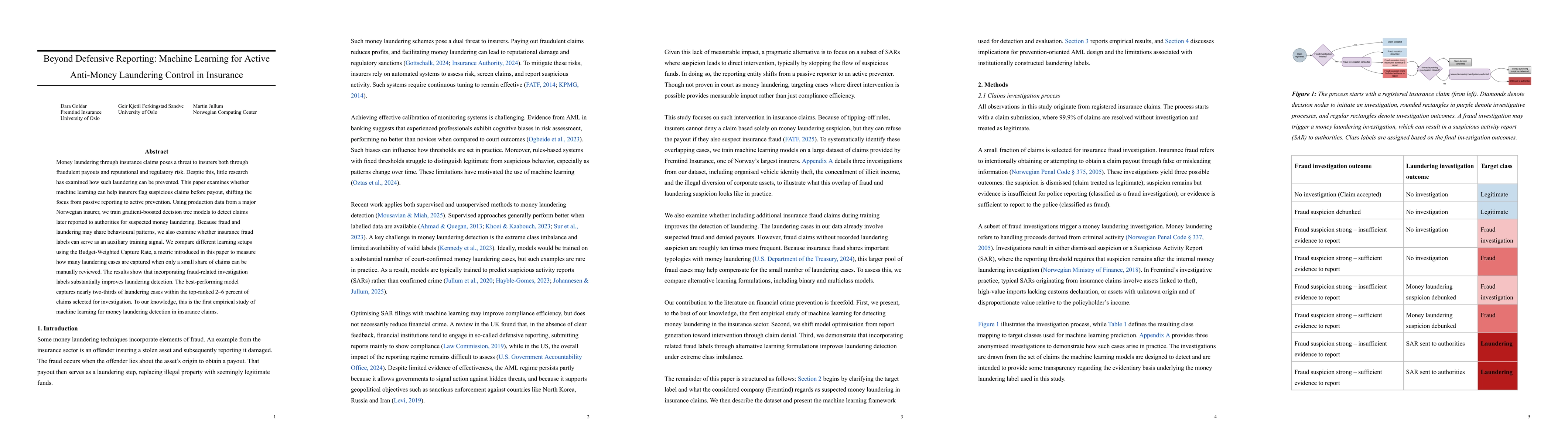

Discussion 0