Calculating CVaR and bPOE for Common Probability Distributions With Application to Portfolio Optimization and Density Estimation

Publication

Metrics

Paper Preview

Abstract

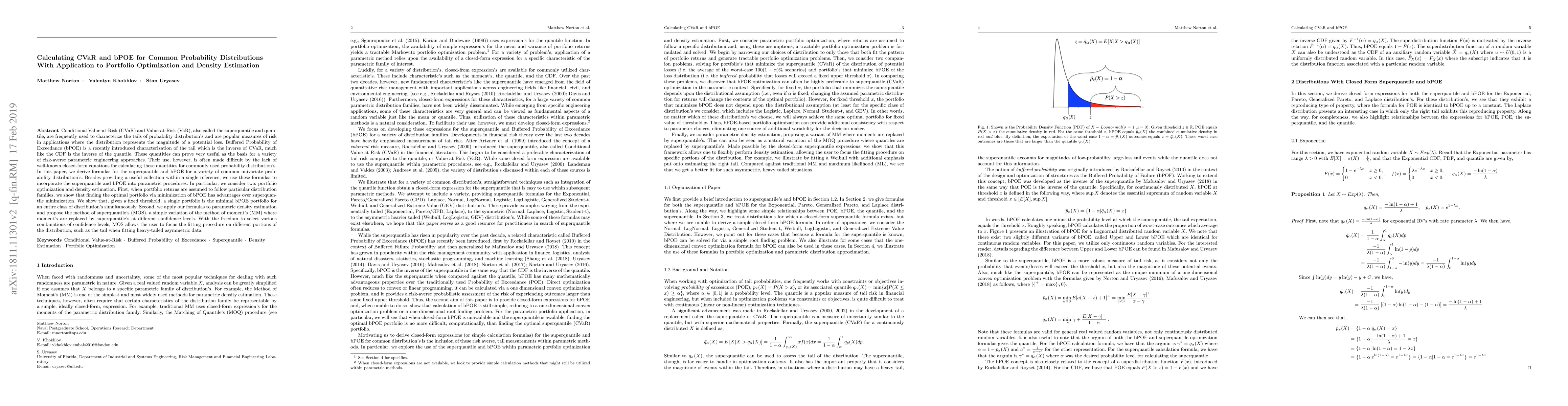

Conditional Value-at-Risk (CVaR) and Value-at-Risk (VaR), also called the superquantile and quantile, are frequently used to characterize the tails of probability distribution's and are popular measures of risk. Buffered Probability of Exceedance (bPOE) is a recently introduced characterization of the tail which is the inverse of CVaR, much like the CDF is the inverse of the quantile. These quantities can prove very useful as the basis for a variety of risk-averse parametric engineering approaches. Their use, however, is often made difficult by the lack of well-known closed-form equations for calculating these quantities for commonly used probability distribution's. In this paper, we derive formulas for the superquantile and bPOE for a variety of common univariate probability distribution's. Besides providing a useful collection within a single reference, we use these formulas to incorporate the superquantile and bPOE into parametric procedures. In particular, we consider two: portfolio optimization and density estimation. First, when portfolio returns are assumed to follow particular distribution families, we show that finding the optimal portfolio via minimization of bPOE has advantages over superquantile minimization. We show that, given a fixed threshold, a single portfolio is the minimal bPOE portfolio for an entire class of distribution's simultaneously. Second, we apply our formulas to parametric density estimation and propose the method of superquantile's (MOS), a simple variation of the method of moment's (MM) where moment's are replaced by superquantile's at different confidence levels. With the freedom to select various combinations of confidence levels, MOS allows the user to focus the fitting procedure on different portions of the distribution, such as the tail when fitting heavy-tailed asymmetric data.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0