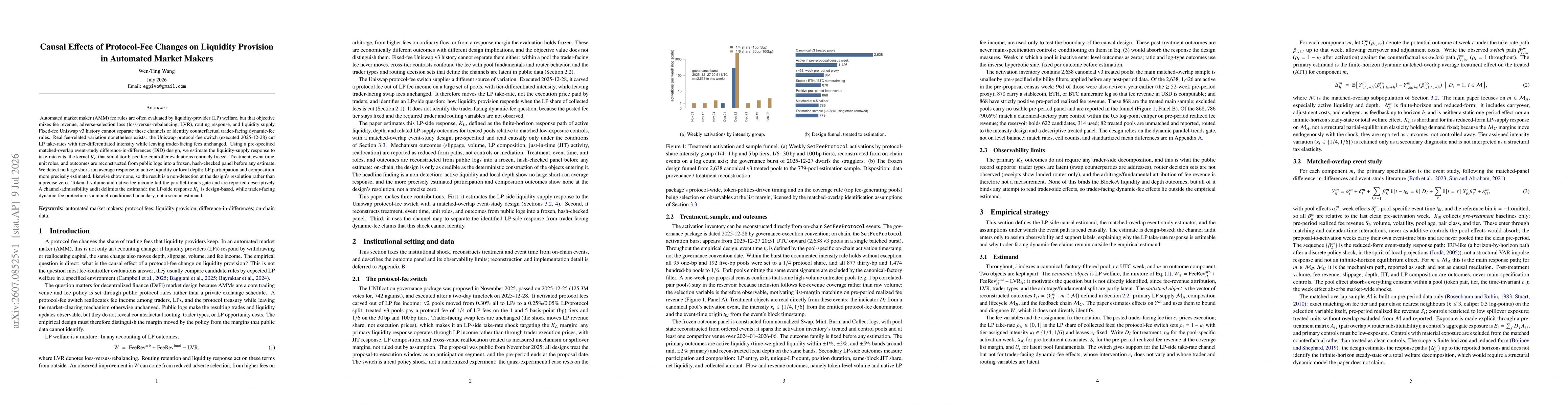

Automated market maker (AMM) fee rules are often evaluated by liquidity-provider (LP) welfare, but that objective mixes fee revenue, adverse-selection loss (loss-versus-rebalancing, LVR), routing response, and liquidity supply. Fixed-fee Uniswap v3 history cannot separate these channels or identify counterfactual trader-facing dynamic-fee rules. Real fee-related variation nonetheless exists: the Uniswap protocol-fee switch cut LP take-rates with tier-differentiated intensity while leaving trader-facing fees unchanged. Using a pre-specified matched-overlap event-study difference-in-differences design, we estimate the liquidity-supply response to take-rate cuts, the kernel K_L that simulator-based fee-controller evaluations routinely freeze, while reconstructing treatment, event time, unit roles, and outcomes from public logs into a frozen, hash-checked panel before any estimate. We detect no large short-run average response in active liquidity or local depth; LP participation and composition, more precisely estimated, likewise show none, so the result is a non-detection at the design's resolution rather than a precise zero. Token-1 volume and native fee income fail the parallel-trends gate and are reported descriptively. A channel-admissibility audit delimits the estimand: the LP-side response K_L is design-based, while trader-facing dynamic-fee protection is a model-conditioned boundary, not a second estimand.

Discussion 0