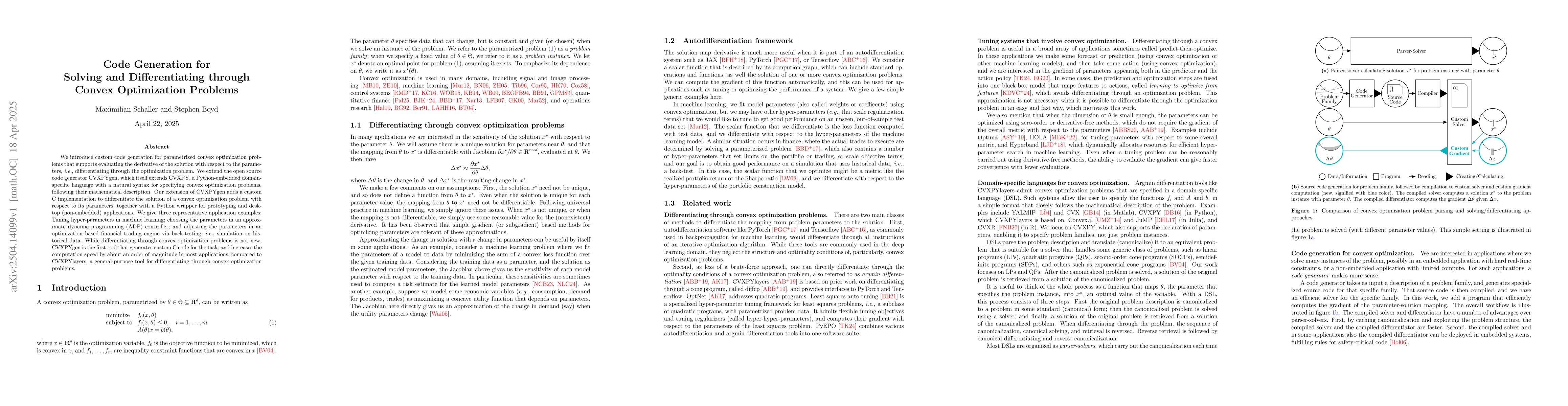

We introduce custom code generation for parametrized convex optimization

problems that supports evaluating the derivative of the solution with respect

to the parameters, i.e., differentiating through the optimization problem. We

extend the open source code generator CVXPYgen, which itself extends CVXPY, a

Python-embedded domain-specific language with a natural syntax for specifying

convex optimization problems, following their mathematical description. Our

extension of CVXPYgen adds a custom C implementation to differentiate the

solution of a convex optimization problem with respect to its parameters,

together with a Python wrapper for prototyping and desktop (non-embedded)

applications. We give three representative application examples: Tuning

hyper-parameters in machine learning; choosing the parameters in an approximate

dynamic programming (ADP) controller; and adjusting the parameters in an

optimization based financial trading engine via back-testing, i.e., simulation

on historical data. While differentiating through convex optimization problems

is not new, CVXPYgen is the first tool that generates custom C code for the

task, and increases the computation speed by about an order of magnitude in

most applications, compared to CVXPYlayers, a general-purpose tool for

differentiating through convex optimization problems.

Discussion 0