Academic Profile

Statistics

Similar Authors

Papers on arXiv

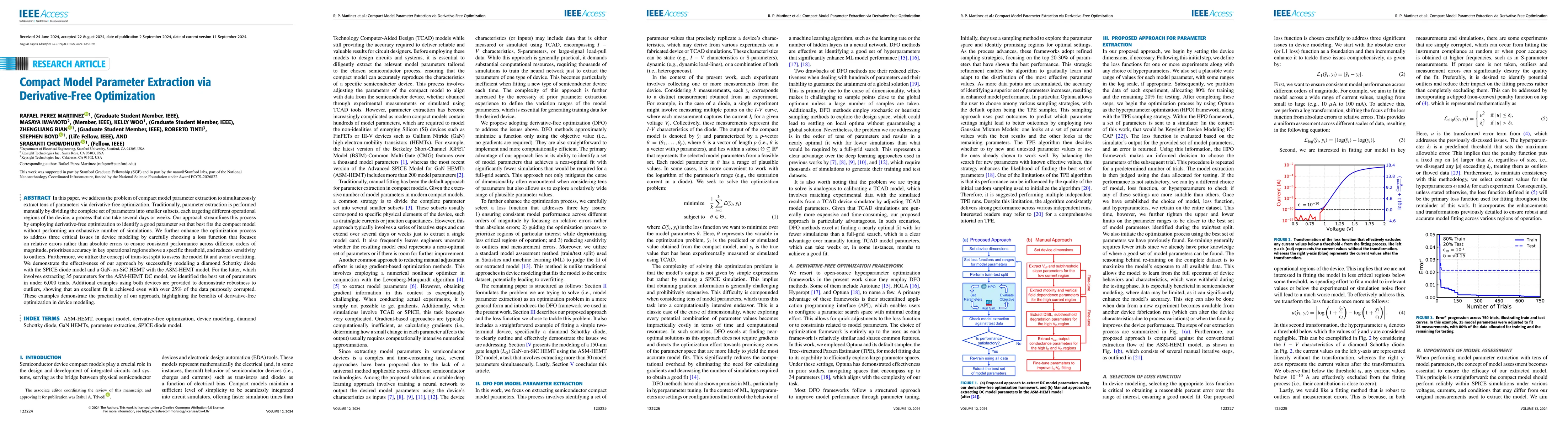

In this paper, we address the problem of compact model parameter extraction to simultaneously extract tens of parameters via derivative-free optimization. Traditionally, parameter extraction is perfor...

Real-world imaging systems acquire measurements that are degraded by noise, optical aberrations, and other imperfections that make image processing for human viewing and higher-level perception task...

This paper introduces a robust Pareto design approach for selecting Gallium Nitride (GaN) High Electron Mobility Transistors (HEMTs), particularly for power amplifier (PA) and low-noise amplifier (L...

An exponentially weighted moving model (EWMM) for a vector time series fits a new data model each time period, based on an exponentially fading loss function on past observed data. The well known an...

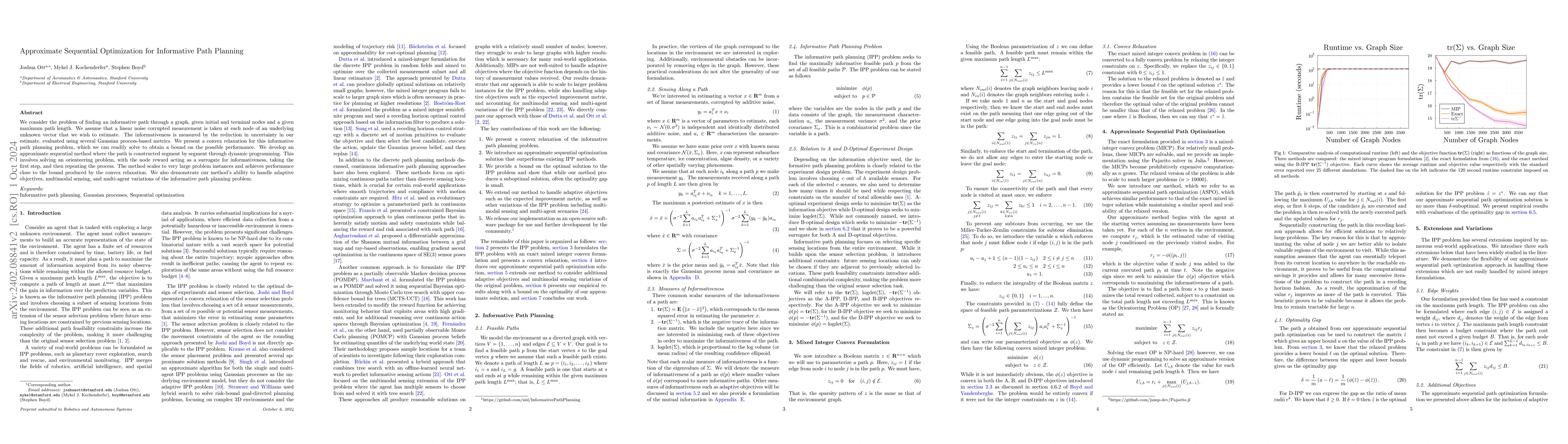

We consider the problem of finding an informative path through a graph, given initial and terminal nodes and a given maximum path length. We assume that a linear noise corrupted measurement is taken...

We propose a new method for finding statistical arbitrages that can contain more assets than just the traditional pair. We formulate the problem as seeking a portfolio with the highest volatility, s...

More than seventy years ago Harry Markowitz formulated portfolio construction as an optimization problem that trades off expected return and risk, defined as the standard deviation of the portfolio ...

We consider the performance of a least-squares regression model, as judged by out-of-sample $R^2$. Shapley values give a fair attribution of the performance of a model to its input features, taking ...

We consider multilevel low rank (MLR) matrices, defined as a row and column permutation of a sum of matrices, each one a block diagonal refinement of the previous one, with all blocks low rank given...

In 1963 Boris Polyak suggested a particular step size for gradient descent methods, now known as the Polyak step size, that he later adapted to subgradient methods. The Polyak step size requires kno...

We consider a simple home energy system consisting of a (net) load, an energy storage device, and a grid connection. We focus on minimizing the cost for grid power that includes a time-varying usage...

We propose a method for designing policies for convex stochastic control problems characterized by random linear dynamics and convex stage cost. We consider policies that employ quadratic approximat...

We consider robust empirical risk minimization (ERM), where model parameters are chosen to minimize the worst-case empirical loss when each data point varies over a given convex uncertainty set. In ...

We consider the well-studied problem of predicting the time-varying covariance matrix of a vector of financial returns. Popular methods range from simple predictors like rolling window or exponentia...

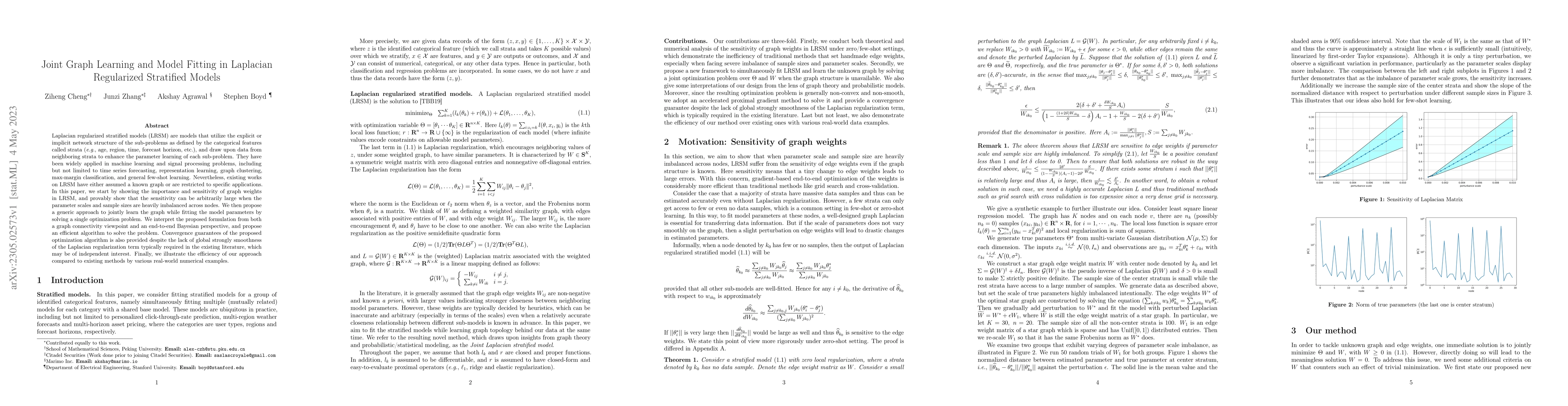

Laplacian regularized stratified models (LRSM) are models that utilize the explicit or implicit network structure of the sub-problems as defined by the categorical features called strata (e.g., age,...

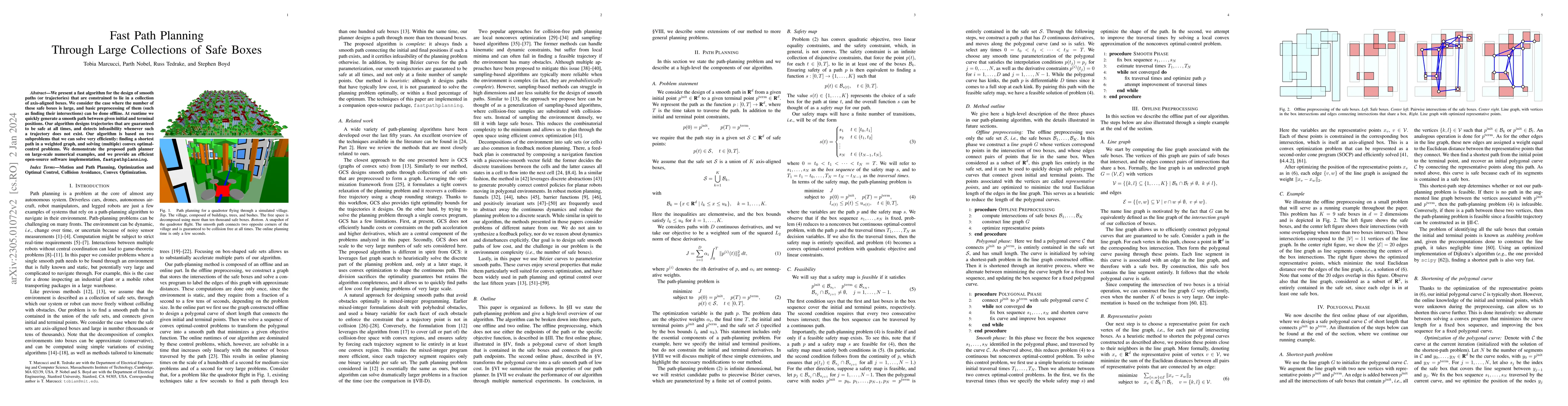

We present a fast algorithm for the design of smooth paths (or trajectories) that are constrained to lie in a collection of axis-aligned boxes. We consider the case where the number of these safe bo...

We consider convex-concave saddle point problems, and more generally convex optimization problems we refer to as $\textit{saddle problems}$, which include the partial supremum or infimum of convex-c...

The minimum (worst case) value of a long-only portfolio of bonds, over a convex set of yield curves and spreads, can be estimated by its sensitivities to the points on the yield curve. We show that ...

Stein's unbiased risk estimate (SURE) gives an unbiased estimate of the $\ell_2$ risk of any estimator of the mean of a Gaussian random vector. We focus here on the case when the estimator minimizes...

We consider the problem of minimizing a function that is a sum of convex agent functions plus a convex common public function that couples them. The agent functions can only be accessed via a subgra...

We consider the problem of choosing a portfolio that maximizes the cumulative prospect theory (CPT) utility on an empirical distribution of asset returns. We show that while CPT utility is not a con...

We address the problem of strategic asset allocation (SAA) with portfolios that include illiquid alternative asset classes. The main challenge in portfolio construction with illiquid asset classes i...

We consider the problem of choosing an optimal portfolio, assuming the asset returns have a Gaussian mixture (GM) distribution, with the objective of maximizing expected exponential utility. In this...

In this paper, we present a method for computing bounds for a variety of efficiency metrics in photonics, such as the focusing efficiency or the mode purity. We focus on the special case where the o...

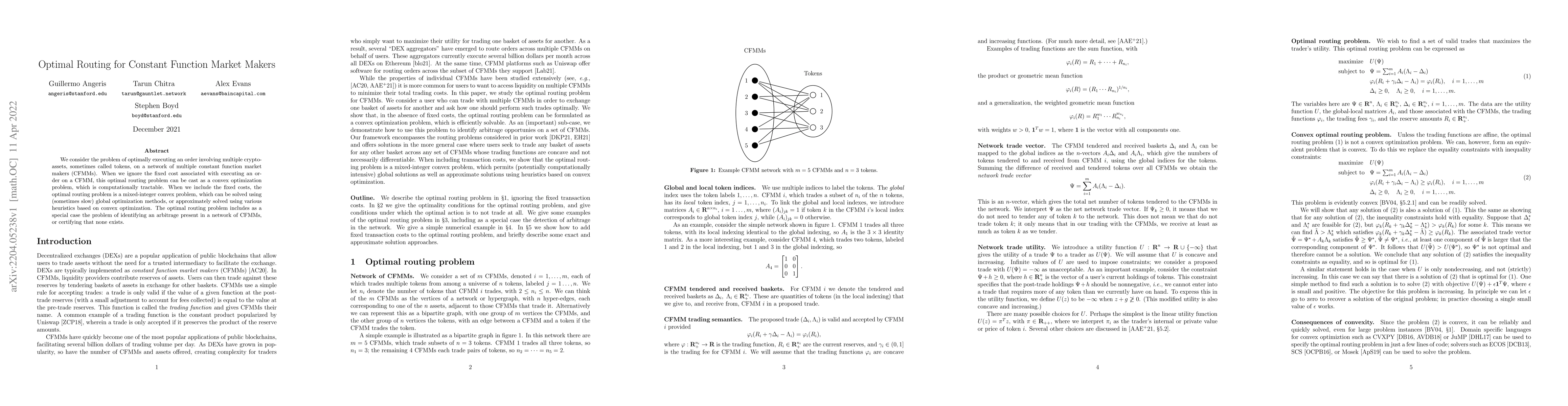

We consider the problem of optimally executing an order involving multiple crypto-assets, sometimes called tokens, on a network of multiple constant function market makers (CFMMs). When we ignore th...

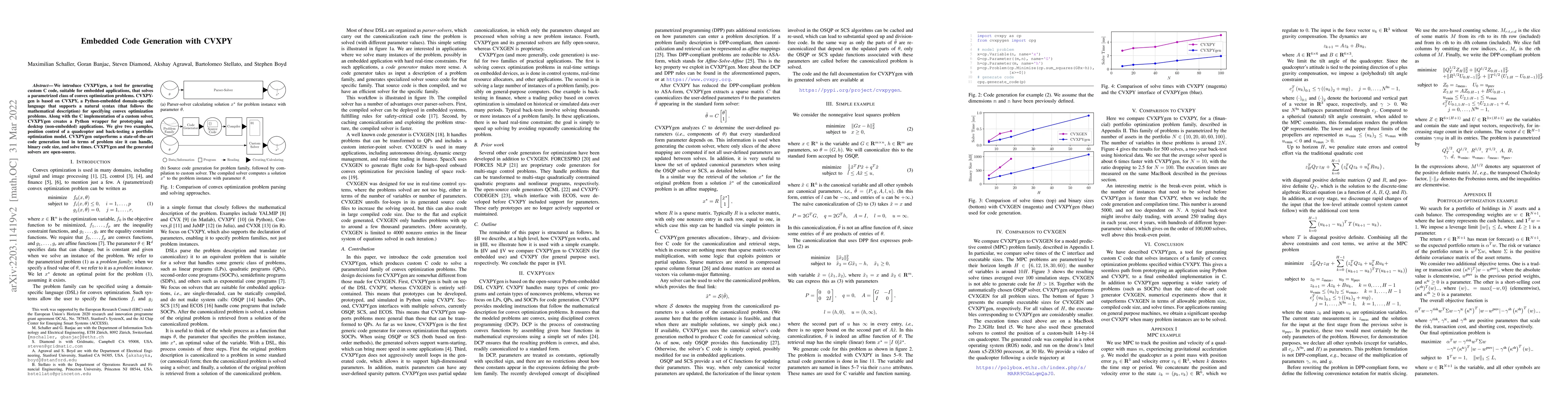

We introduce CVXPYgen, a tool for generating custom C code, suitable for embedded applications, that solves a parametrized class of convex optimization problems. CVXPYgen is based on CVXPY, a Python...

We describe a light-weight yet performant system for hyper-parameter optimization that approximately minimizes an overall scalar cost function that is obtained by combining multiple performance obje...

In recent work Simkin shows that bounds on an exponent occurring in the famous $n$-queens problem can be evaluated by solving convex optimization problems, allowing him to find bounds far tighter th...

Multi-forecast model predictive control (MF-MPC) is a control policy that creates a plan of actions over a horizon for each of a given set of forecasted scenarios or contingencies, with the constrai...

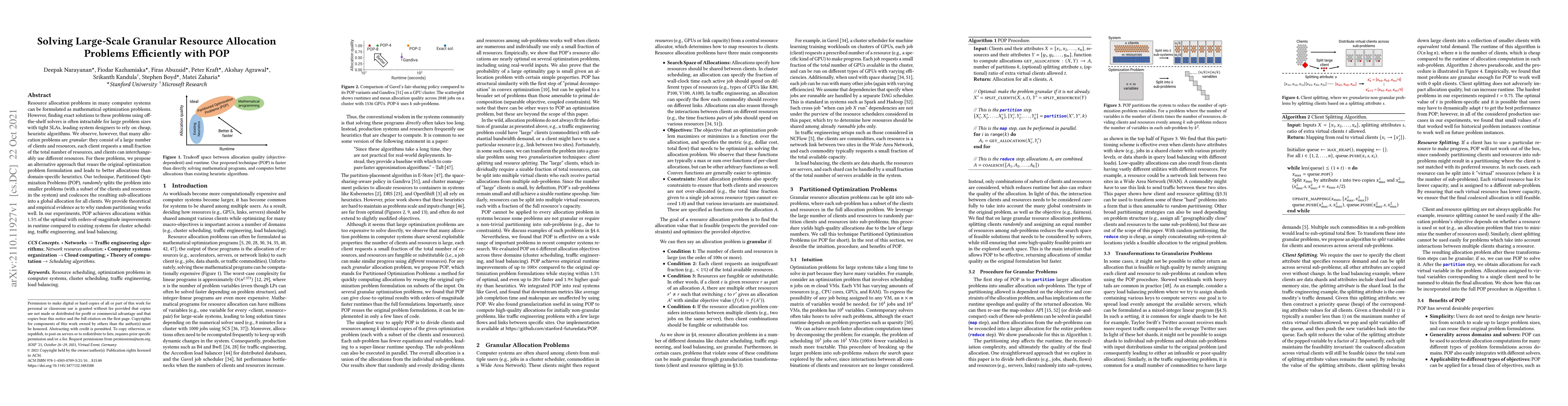

Resource allocation problems in many computer systems can be formulated as mathematical optimization problems. However, finding exact solutions to these problems using off-the-shelf solvers is often...

The rise of Ethereum and other blockchains that support smart contracts has led to the creation of decentralized exchanges (DEXs), such as Uniswap, Balancer, Curve, mStable, and SushiSwap, which ena...

Using a lifecycle framework with Epstein-Zin (1989) utility and a mixed-integer optimization approach, we compute the optimal age to claim Social Security benefits. Taking advantage of homogeneity, ...

We consider the problem of minimizing a composite convex function with two different access methods: an oracle, for which we can evaluate the value and gradient, and a structured function, which we ...

We present an optimization-based approach to radiation treatment planning over time. Our approach formulates treatment planning as an optimal control problem with nonlinear patient health dynamics d...

Mean-variance portfolio optimization problems often involve separable nonconvex terms, including penalties on capital gains, integer share constraints, and minimum position and trade sizes. We propo...

We consider the vector embedding problem. We are given a finite set of items, with the goal of assigning a representative vector to each one, possibly under some constraints (such as the collection ...

We consider an investment process that includes a number of features, each of which can be active or inactive. Our goal is to attribute or decompose an achieved performance to each of these features...

We consider the problem of predicting the covariance of a zero mean Gaussian vector, based on another feature vector. We describe a covariance predictor that has the form of a generalized linear mod...

We consider the problem of forecasting multiple values of the future of a vector time series, using some past values. This problem, and related ones such as one-step-ahead prediction, have a very lo...

The Merton problem is the well-known stochastic control problem of choosing consumption over time, as well as an investment mix, to maximize expected constant relative risk aversion (CRRA) utility o...

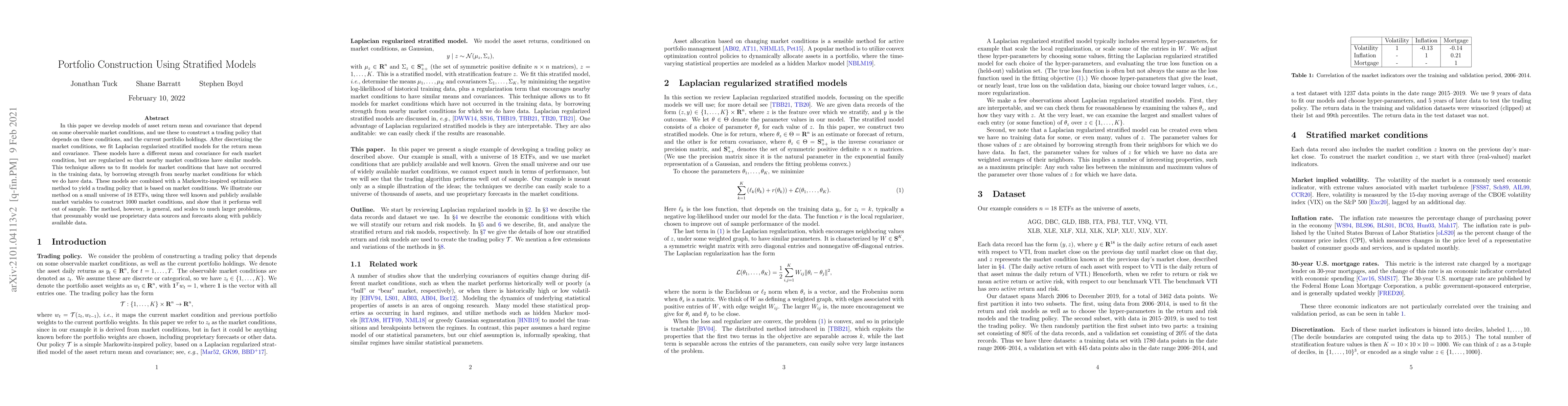

In this paper we develop models of asset return mean and covariance that depend on some observable market conditions, and use these to construct a trading policy that depends on these conditions, an...

In the photonic design problem, a scientist or engineer chooses the physical parameters of a device to best match some desired device behavior. Many instances of the photonic design problem can be n...

We present a new approach for inference about a log-concave distribution: Instead of using the method of maximum likelihood, we propose to incorporate the log-concavity constraint in an appropriate ...

Policy gradient methods are among the most effective methods for large-scale reinforcement learning, and their empirical success has prompted several works that develop the foundation of their globa...

We describe an optimization-based tax-aware portfolio construction method that adds tax liability to standard Markowitz-based portfolio construction. Our method produces a trade list that specifies ...

A convex optimization model predicts an output from an input by solving a convex optimization problem. The class of convex optimization models is large, and includes as special cases many well-known...

We consider the problem of determining a sequence of payments among a set of entities that clear (if possible) the liabilities among them. We formulate this as an optimal control problem, which is c...

We consider the problem of assigning weights to a set of samples or data records, with the goal of achieving a representative weighting, which happens when certain sample averages of the data are cl...

We consider the problem of jointly estimating multiple related zero-mean Gaussian distributions from data. We propose to jointly estimate these covariance matrices using Laplacian regularized strati...

We show how to efficiently compute the derivative (when it exists) of the solution map of log-log convex programs (LLCPs). These are nonconvex, nonsmooth optimization problems with positive variable...

We consider a collection of derivatives that depend on the price of an underlying asset at expiration or maturity. The absence of arbitrage is equivalent to the existence of a risk-neutral probabili...

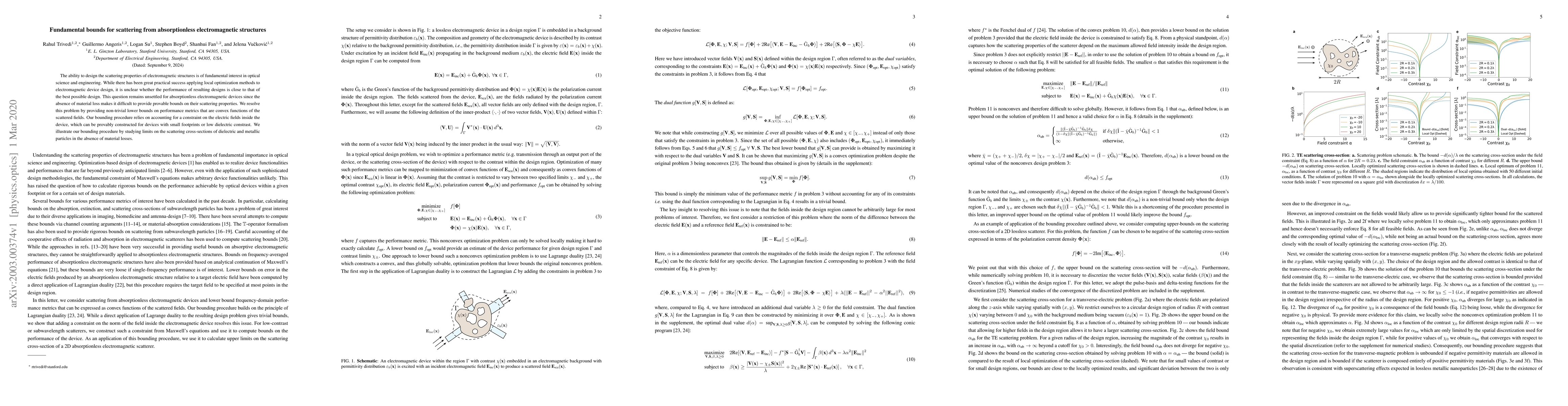

The ability to design the scattering properties of electromagnetic structures is of fundamental interest in optical science and engineering. While there has been great practical success applying loc...

In a physical design problem, the designer chooses values of some physical parameters, within limits, to optimize the resulting field. We focus on the specific case in which each physical design par...

Given an infeasible, unbounded, or pathological convex optimization problem, a natural question to ask is: what is the smallest change we can make to the problem's parameters such that the problem b...

Stratified models depend in an arbitrary way on a selected categorical feature that takes $K$ values, and depend linearly on the other $n$ features. Laplacian regularization with respect to a graph ...

We consider the problem of learning a linear control policy for a linear dynamical system, from demonstrations of an expert regulating the system. The standard approach to this problem is policy fit...

Many control policies used in various applications determine the input or action by solving a convex optimization problem that depends on the current state and some parameters. Common examples of su...

Recent work has shown how to embed differentiable optimization problems (that is, problems whose solutions can be backpropagated through) as layers within deep learning architectures. This method pr...

We consider the problem of minimizing a sum of clipped convex functions; applications include clipped empirical risk minimization and clipped control. While the problem of minimizing the sum of clip...

This paper considers the problem of fitting the parameters of a Kalman smoother to data. We formulate the Kalman smoothing problem with missing measurements as a constrained least squares problem an...

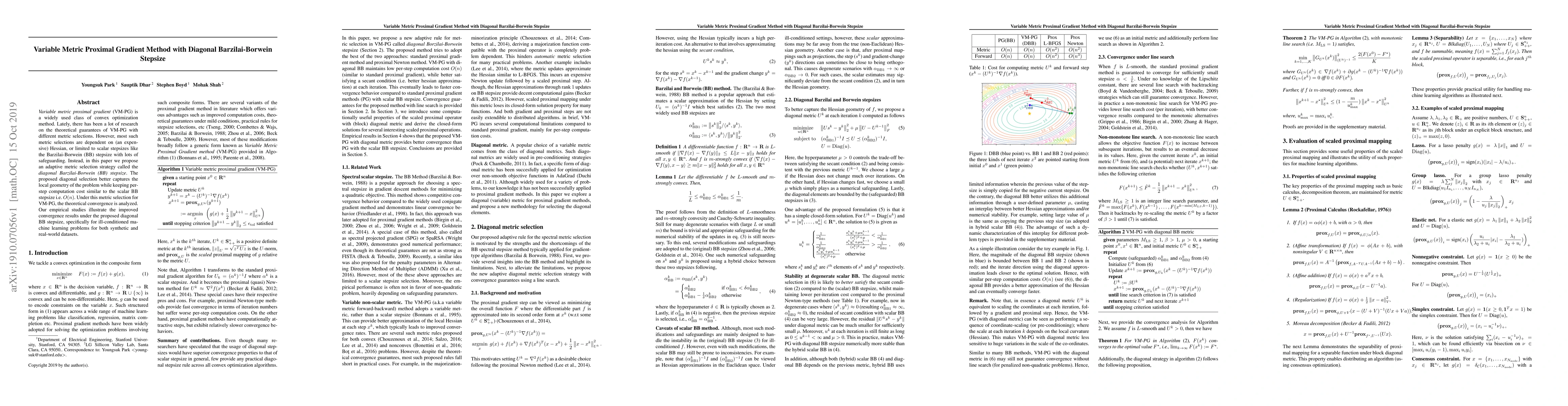

Variable metric proximal gradient (VM-PG) is a widely used class of convex optimization method. Lately, there has been a lot of research on the theoretical guarantees of VM-PG with different metric ...

We consider the problem of non-smooth convex optimization with linear equality constraints, where the objective function is only accessible through its proximal operator. This problem arises in many...

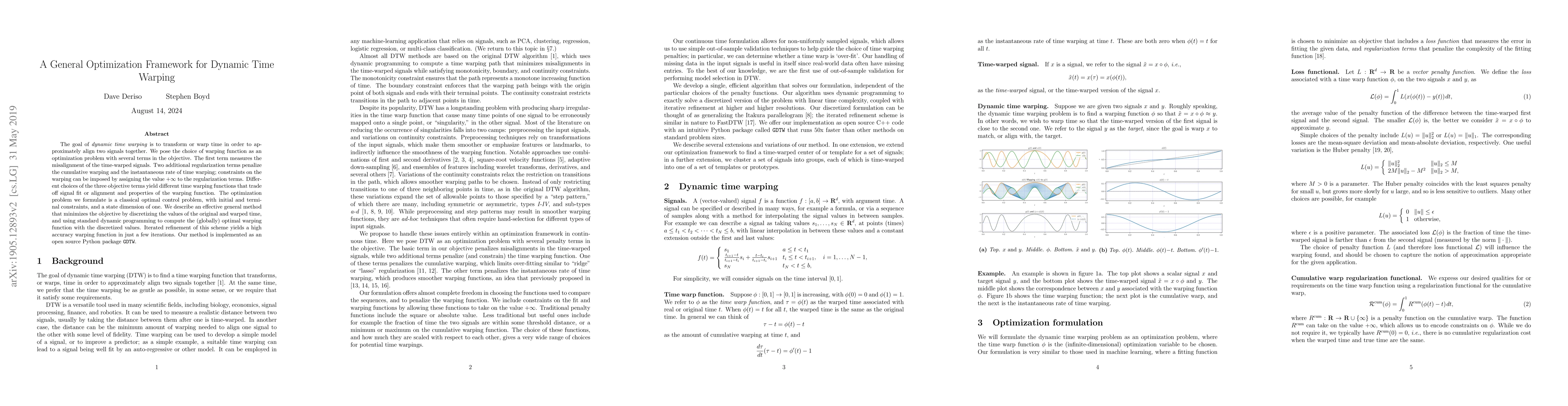

The goal of dynamic time warping is to transform or warp time in order to approximately align two signals together. We pose the choice of warping function as an optimization problem with several ter...

We present a composition rule involving quasiconvex functions that generalizes the classical composition rule for convex functions. This rule complements well-known rules for the curvature of quasic...

Stratified models are models that depend in an arbitrary way on a set of selected categorical features, and depend linearly on the other features. In a basic and traditional formulation a separate m...

We consider the problem of efficiently computing the derivative of the solution map of a convex cone program, when it exists. We do this by implicitly differentiating the residual map for its homoge...

Physical design problems, such as photonic inverse design, are typically solved using local optimization methods. These methods often produce what appear to be good or very good designs when compare...

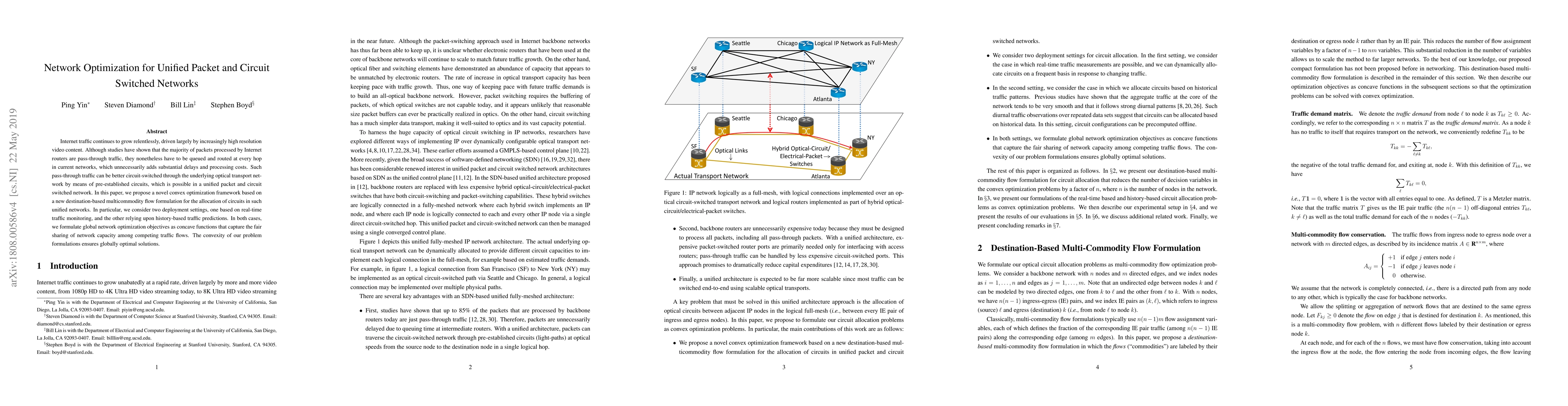

Internet traffic continues to grow relentlessly, driven largely by increasingly high resolution video content. Although studies have shown that the majority of packets processed by Internet routers ...

We present a general-purpose solver for convex quadratic programs based on the alternating direction method of multipliers, employing a novel operator splitting technique that requires the solution ...

CVXR is an R package that provides an object-oriented modeling language for convex optimization, similar to CVX, CVXPY, YALMIP, and Convex.jl. It allows the user to formulate convex optimization pro...

We examine a special case of the multilevel factor model, with covariance given by multilevel low rank (MLR) matrix~\cite{parshakova2023factor}. We develop a novel, fast implementation of the expectat...

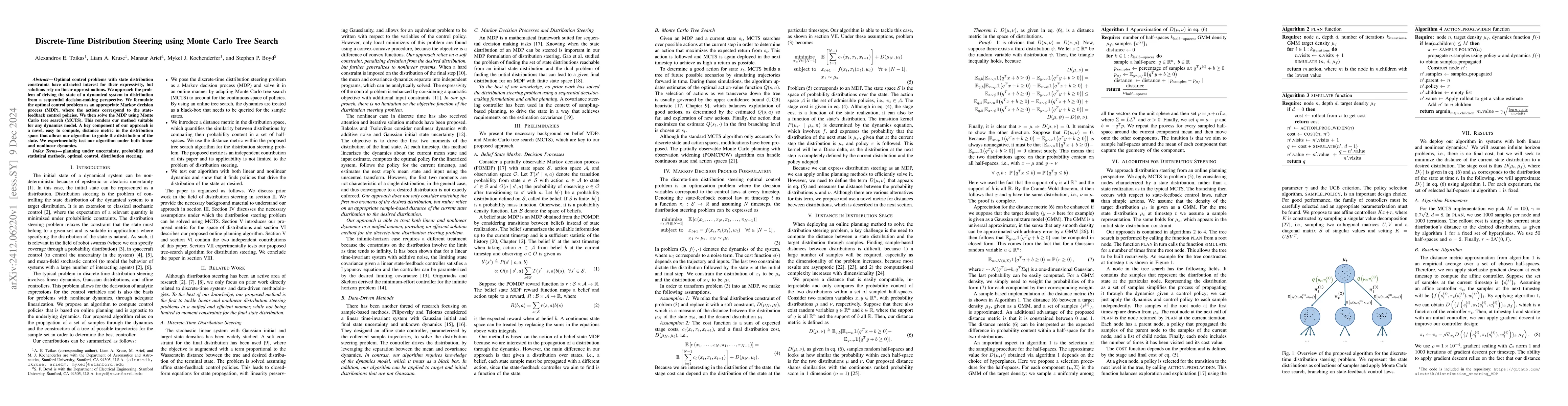

Optimal control problems with state distribution constraints have attracted interest for their expressivity, but solutions rely on linear approximations. We approach the problem of driving the state o...

We consider the problem of managing a portfolio of moving-band statistical arbitrages (MBSAs), inspired by the Markowitz optimization framework. We show how to manage a dynamic basket of MBSAs, and il...

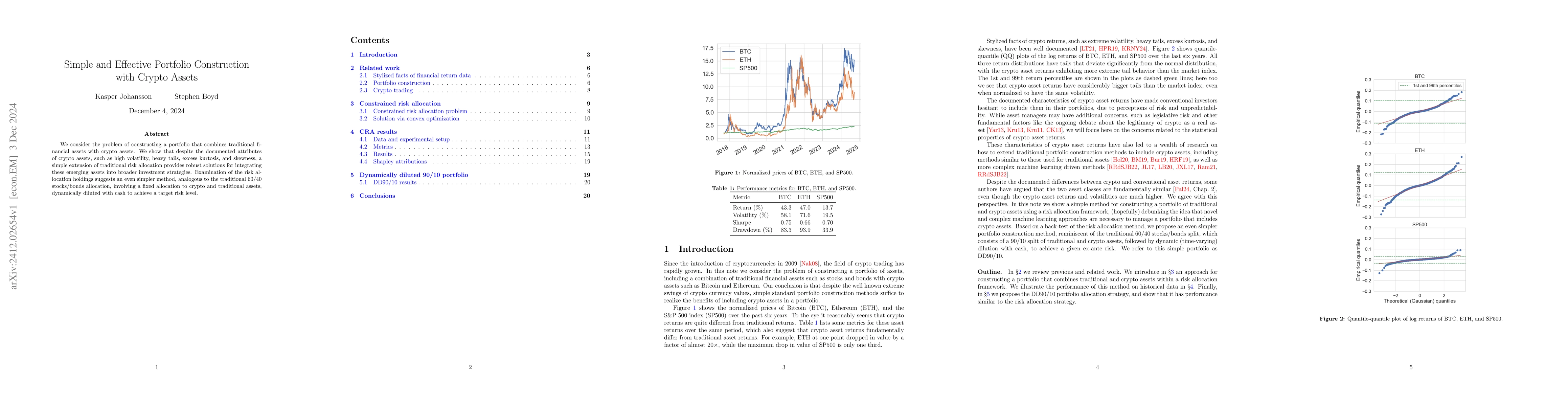

We consider the problem of constructing a portfolio that combines traditional financial assets with crypto assets. We show that despite the documented attributes of crypto assets, such as high volatil...

We propose a bit-flip descent method for optimizing binary spreading codes with large family sizes and long lengths, addressing the challenges of large-scale code design in GNSS and emerging PNT appli...

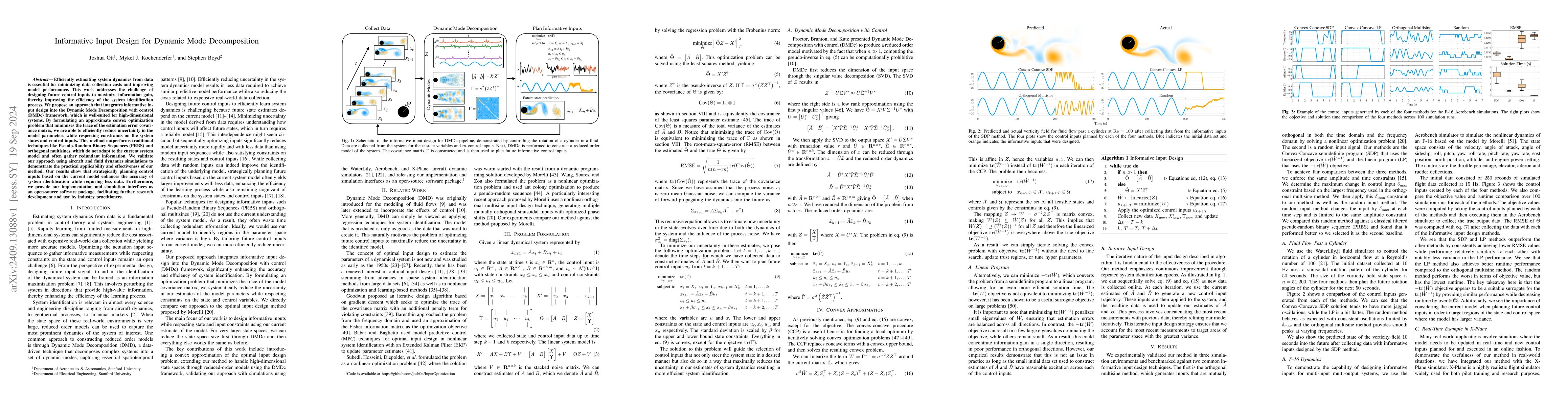

Efficiently estimating system dynamics from data is essential for minimizing data collection costs and improving model performance. This work addresses the challenge of designing future control inputs...

We present the GPU implementation of the general-purpose interior-point solver Clarabel for convex optimization problems with conic constraints. We introduce a mixed parallel computing strategy that p...

We consider the all-pairs multicommodity network flow problem on a network with capacitated edges. The usual treatment keeps track of a separate flow for each source-destination pair on each edge; we ...

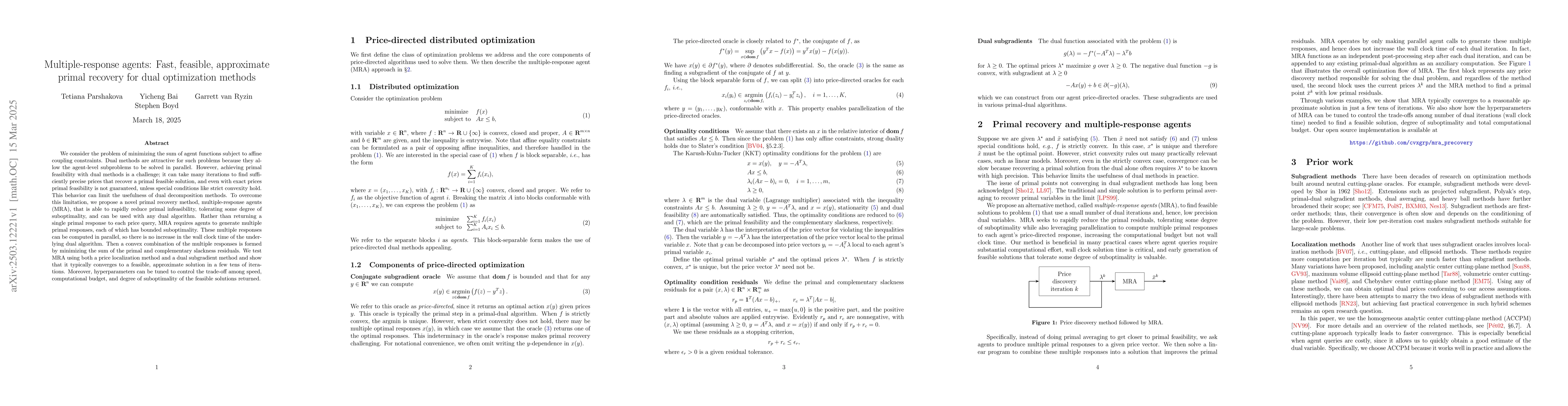

We consider the problem of minimizing the sum of agent functions subject to affine coupling constraints. Dual methods are attractive for such problems because they allow the agent-level subproblems to...

We introduce a fast and scalable method for solving quadratic programs with conditional value-at-risk (CVaR) constraints. While these problems can be formulated as standard quadratic programs, the num...

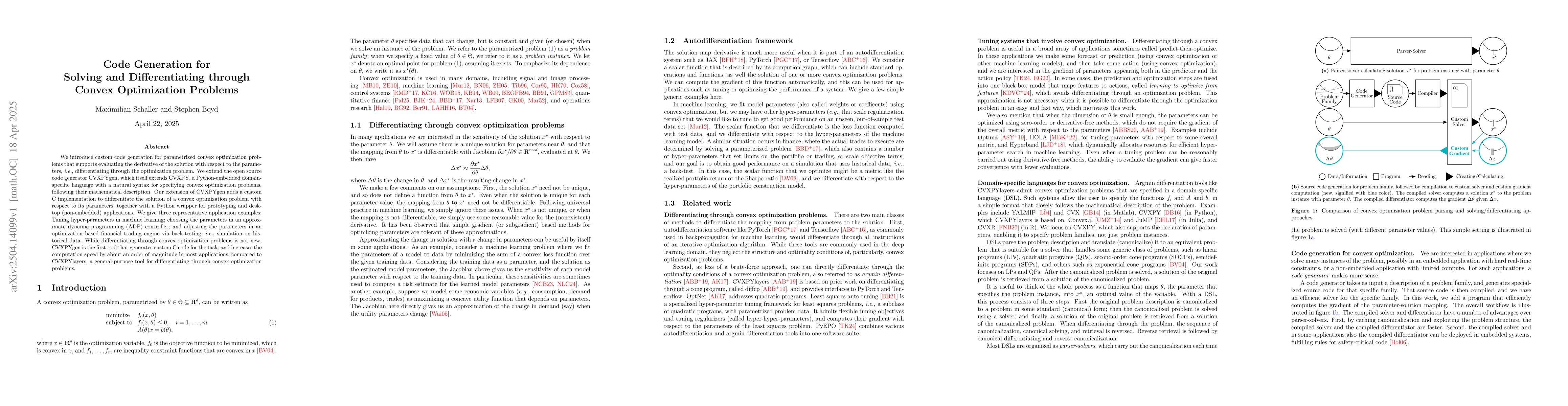

We introduce custom code generation for parametrized convex optimization problems that supports evaluating the derivative of the solution with respect to the parameters, i.e., differentiating through ...

We consider the task of controlling a battery while balancing two competing objectives that evolve over different time scales. The short-term objective, such as arbitrage or load smoothing, improves w...

A parametrized convex function depends on a variable and a parameter, and is convex in the variable for any valid value of the parameter. Such functions can be used to specify parametrized convex opti...

We consider a family of convex quadratic programs in which the coefficients of the linear objective term and the righthand side of the constraints are affine functions of a parameter. It is well known...

The Kalman filter (KF) provides optimal recursive state estimates for linear-Gaussian systems and underpins applications in control, signal processing, and others. However, it is vulnerable to outlier...

The retirement funding problem addresses the question of how to manage a retiree's savings to provide her with a constant post-tax inflation adjusted consumption throughout her lifetime. This consists...

This paper proposes a simulation-based framework for assessing and improving the performance of a pension fund management scheme. This framework is modular and allows the definition of customized perf...

Quadratic cone programs are rapidly becoming the standard canonical form for convex optimization problems. In this paper we address the question of differentiating the solution map for such problems, ...

We consider the problem of choosing prices of a set of products so as to maximize profit, taking into account self-elasticity and cross-elasticity, subject to constraints on the prices. We show that t...

Semidefinite programming is a fundamental problem class in convex optimization, but despite recent advances in solvers, solving large-scale semidefinite programs remains challenging. Generally the mat...

This paper introduces methodologies for constructing an index composed of a risky asset and a risk-free asset that achieves a fixed target volatility. We propose a simple proportional-control-based ap...

Funds at large portfolio management firms may consist of many portfolio managers (PMs), each managing a portion of the fund and optimizing a distinct objective. Although the PMs determine their trades...

The relationship between demand and prices of a set of products can be modeled as a linear mapping from logarithmic price changes to logarithmic changes in demand. We consider the problem of estimatin...

Recent research has focused on developing GPU-accelerated first-order solvers for linear programming (LP). This line of work, however, has largely overlooked the role of presolving, and thus prior res...

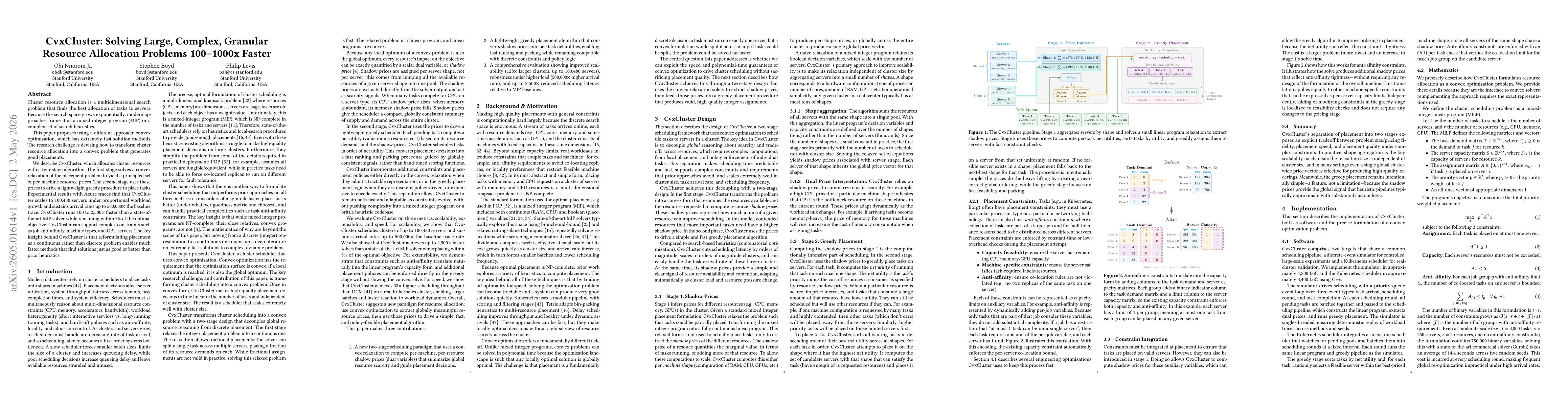

Cluster resource allocation is a multidimensional search problem that finds the best allocation of tasks to servers. Because the search space grows exponentially, modern approaches frame it as a mixed...

We introduce disciplined nonlinear programming (DNLP), a syntax for specifying nonlinear programming problems. DNLP is inspired by disciplined convex programming (DCP) and allows smooth functions to b...