Combining supervised and unsupervised learning methods to predict financial market movements

Publication

Metrics

AI Quick Summary

This paper combines supervised and unsupervised learning methods to predict financial market movements using novel features extracted from Bitcoin, Pepecoin, and Nasdaq markets. The study shows that Gaussian Mixture Models and machine learning strategies like Random Forests and K-Nearest Neighbours yield higher returns compared to a naive random approach.

Paper Preview

Abstract

The decisions traders make to buy or sell an asset depend on various analyses, with expertise required to identify patterns that can be exploited for profit. In this paper we identify novel features extracted from emergent and well-established financial markets using linear models and Gaussian Mixture Models (GMM) with the aim of finding profitable opportunities. We used approximately six months of data consisting of minute candles from the Bitcoin, Pepecoin, and Nasdaq markets to derive and compare the proposed novel features with commonly used ones. These features were extracted based on the previous 59 minutes for each market and used to identify predictions for the hour ahead. We explored the performance of various machine learning strategies, such as Random Forests (RF) and K-Nearest Neighbours (KNN) to classify market movements. A naive random approach to selecting trading decisions was used as a benchmark, with outcomes assumed to be equally likely. We used a temporal cross-validation approach using test sets of 40%, 30% and 20% of total hours to evaluate the learning algorithms' performances. Our results showed that filtering the time series facilitates algorithms' generalisation. The GMM filtering approach revealed that the KNN and RF algorithms produced higher average returns than the random algorithm.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

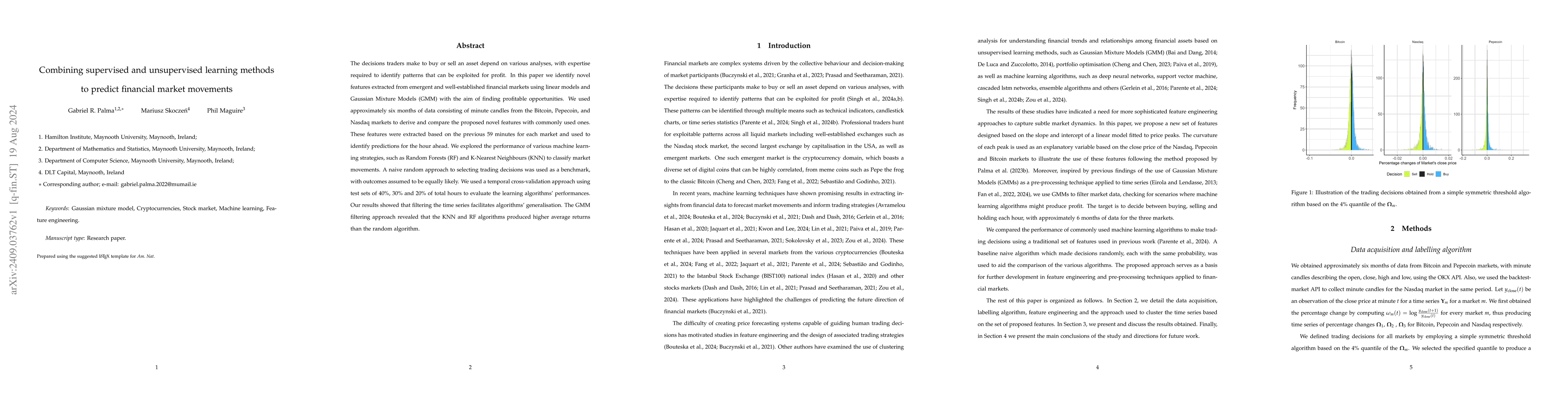

Discussion 0