Complex network analysis of cryptocurrency market during crashes

Publication

Metrics

AI Quick Summary

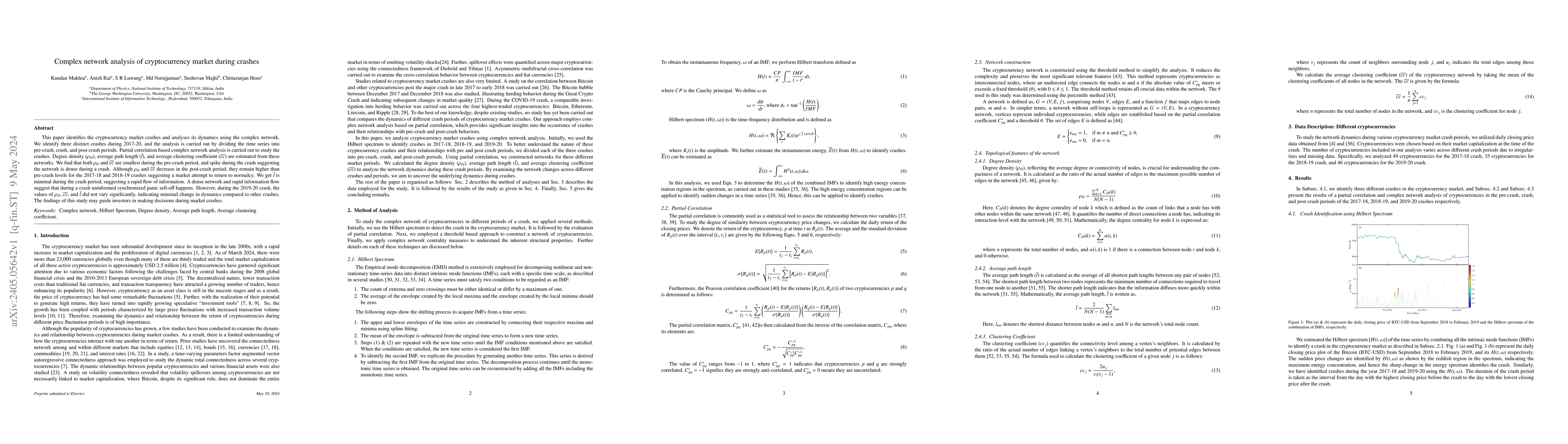

This study employs complex network analysis to examine cryptocurrency market crashes between 2017-20, revealing dense network conditions during crashes and a rapid information flow, while suggesting that investors can use these insights for better decision-making during market downturns. The 2019-20 crash showed minimal network dynamics changes compared to previous crashes.

Paper Preview

Abstract

This paper identifies the cryptocurrency market crashes and analyses its dynamics using the complex network. We identify three distinct crashes during 2017-20, and the analysis is carried out by dividing the time series into pre-crash, crash, and post-crash periods. Partial correlation based complex network analysis is carried out to study the crashes. Degree density ($\rho_D$), average path length ($\bar{l}$), and average clustering coefficient ($\overline{cc}$) are estimated from these networks. We find that both $\rho_D$ and $\overline{cc}$ are smallest during the pre-crash period, and spike during the crash suggesting the network is dense during a crash. Although $\rho_D$ and $\overline{cc}$ decrease in the post-crash period, they remain higher than pre-crash levels for the 2017-18 and 2018-19 crashes suggesting a market attempt to return to normalcy. We get $\bar{l}$ is minimal during the crash period, suggesting a rapid flow of information. A dense network and rapid information flow suggest that during a crash uninformed synchronized panic sell-off happens. However, during the 2019-20 crash, the values of $\rho_D$, $\overline{cc}$, and $\bar{l}$ did not vary significantly, indicating minimal change in dynamics compared to other crashes. The findings of this study may guide investors in making decisions during market crashes.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0