Academic Profile

Statistics

Similar Authors

Papers on arXiv

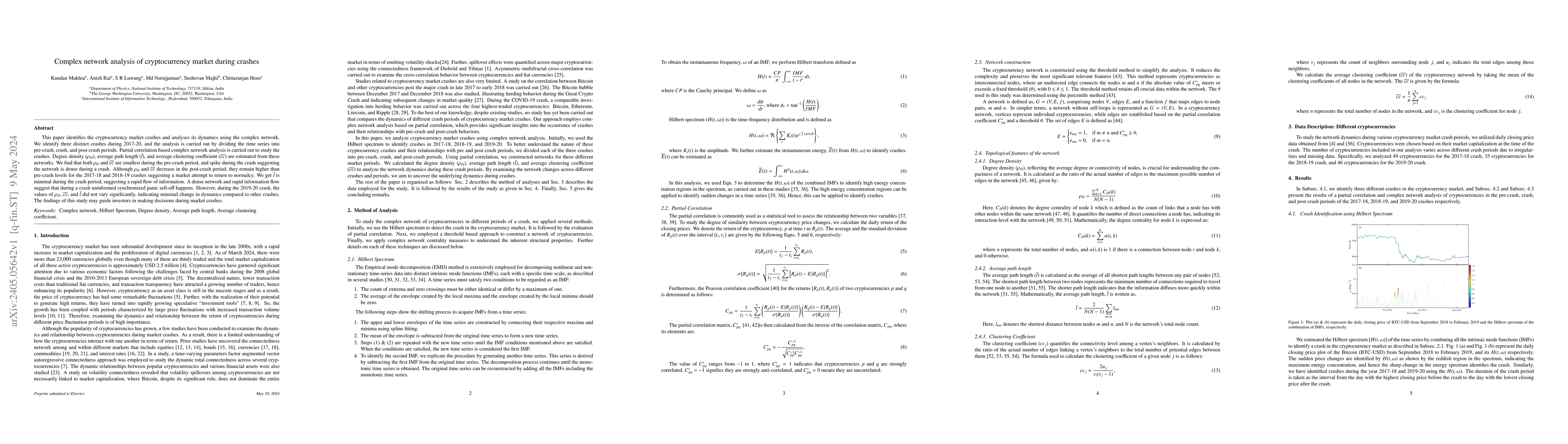

This paper identifies the cryptocurrency market crashes and analyses its dynamics using the complex network. We identify three distinct crashes during 2017-20, and the analysis is carried out by div...

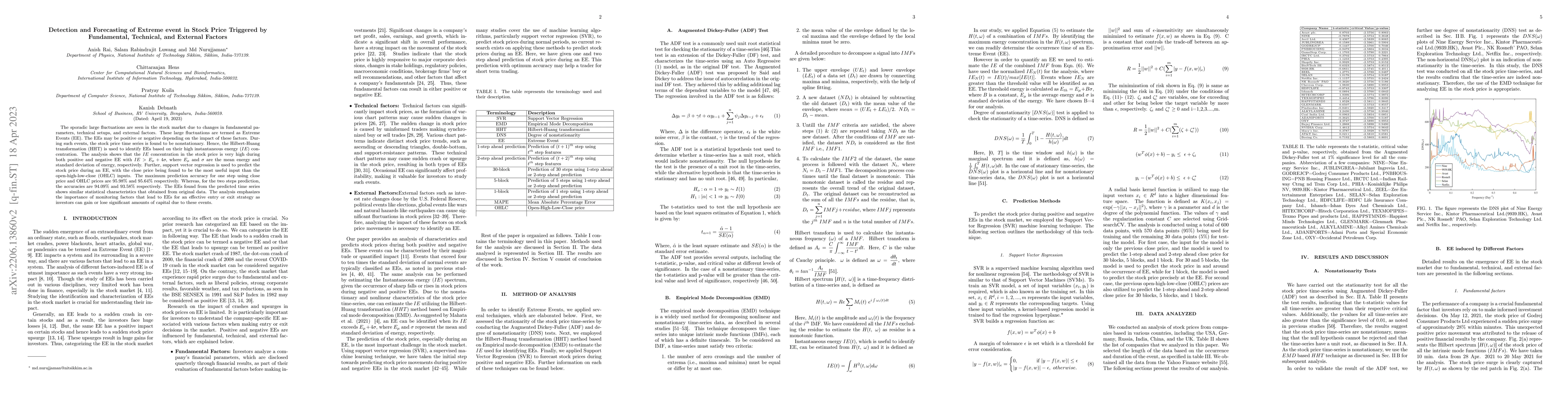

The sporadic large fluctuations are seen in the stock market due to changes in fundamental parameters, technical setups, and external factors. These large fluctuations are termed as Extreme Events (...

The paper presents the comparative study of the nature of stock markets in short-term and long-term time scales with and without structural break in the stock data. Structural break point has been i...

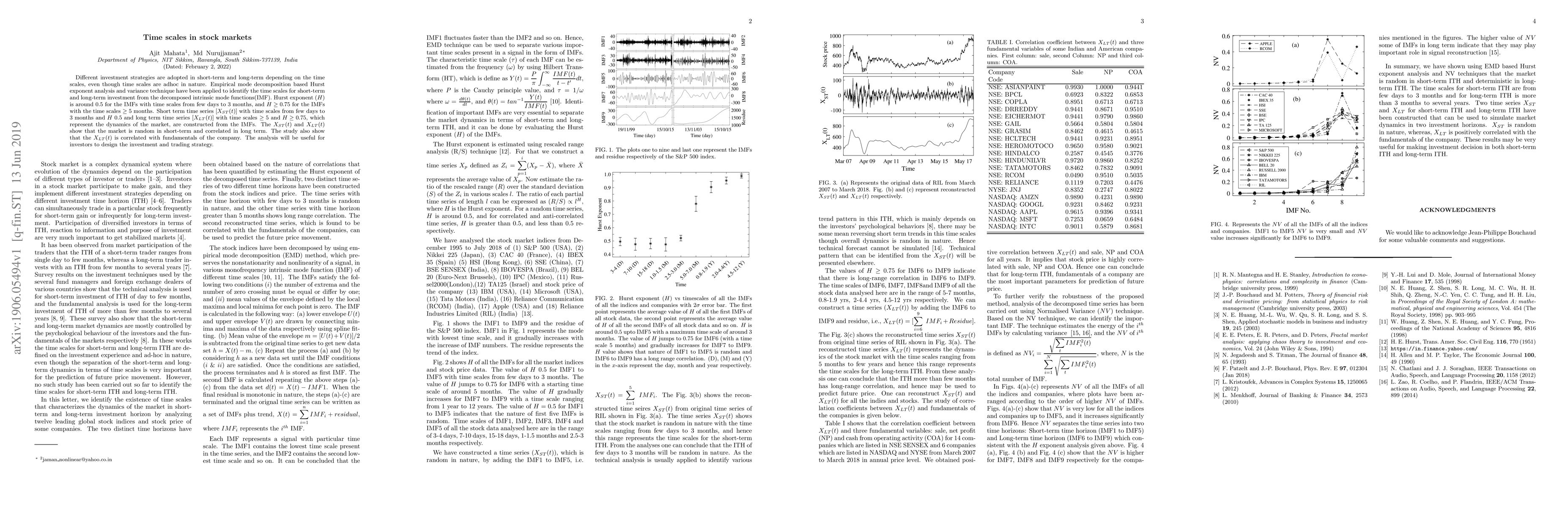

Different investment strategies are adopted in short-term and long-term depending on the time scales, even though time scales are adhoc in nature. Empirical mode decomposition based Hurst exponent a...

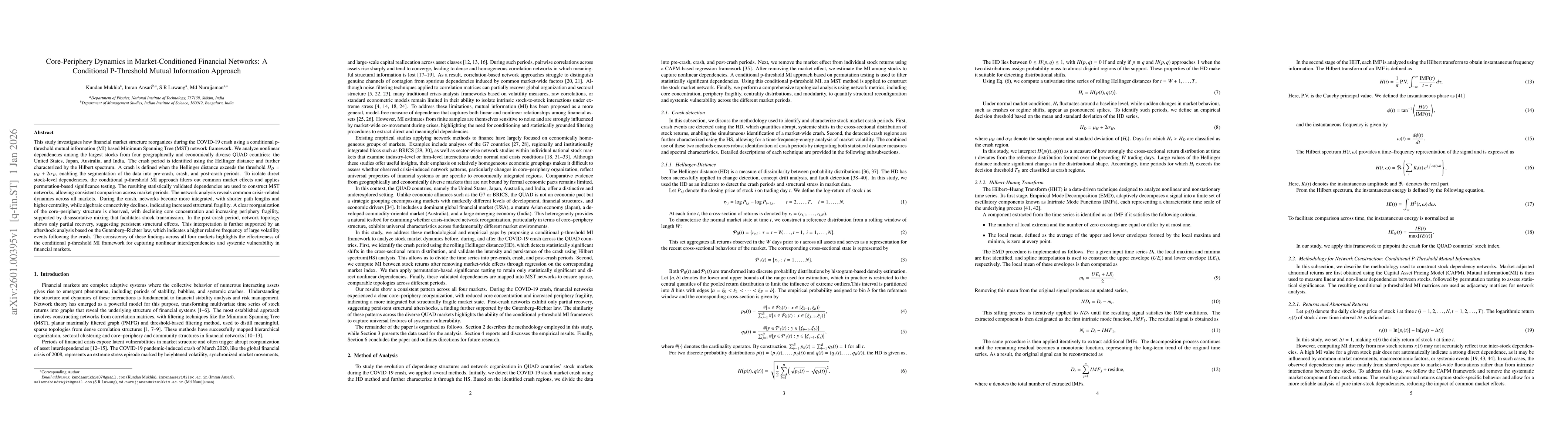

This study investigates how financial market structure reorganizes during the COVID-19 crash using a conditional p-threshold mutual information (MI) based Minimum Spanning Tree (MST) framework. We ana...

We develop a framework for detecting regime transitions in dynamical systems using the Mixup Euler Characteristic Profile (Mixup ECP) -- the Euler characteristic of the geometric intersection of ball ...