Copula Averaging for Tail Dependence in Insurance Claims Data

Publication

Metrics

AI Quick Summary

This paper proposes a Bayesian model averaging method for estimating tail dependence in insurance claims data using copulas. It demonstrates the approach through various copula models and both simulated and real insurance loss datasets to provide a unified estimate of tail dependence.

Paper Preview

Abstract

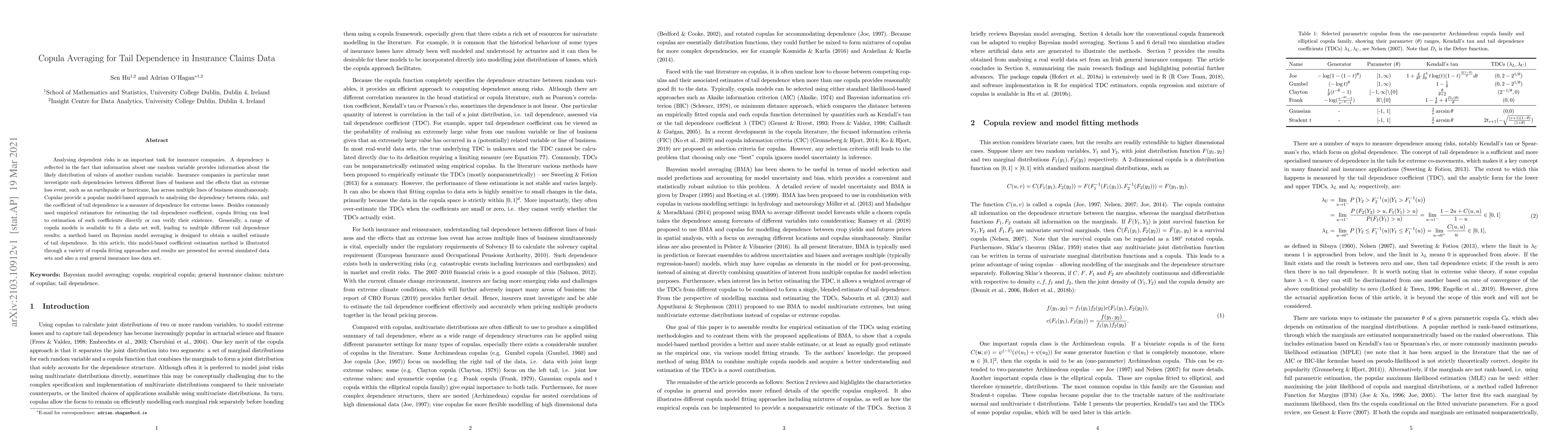

Analysing dependent risks is an important task for insurance companies. A dependency is reflected in the fact that information about one random variable provides information about the likely distribution of values of another random variable. Insurance companies in particular must investigate such dependencies between different lines of business and the effects that an extreme loss event, such as an earthquake or hurricane, has across multiple lines of business simultaneously. Copulas provide a popular model-based approach to analysing the dependency between risks, and the coefficient of tail dependence is a measure of dependence for extreme losses. Besides commonly used empirical estimators for estimating the tail dependence coefficient, copula fitting can lead to estimation of such coefficients directly or can verify their existence. Generally, a range of copula models is available to fit a data set well, leading to multiple different tail dependence results; a method based on Bayesian model averaging is designed to obtain a unified estimate of tail dependence. In this article, this model-based coefficient estimation method is illustrated through a variety of copula fitting approaches and results are presented for several simulated data sets and also a real general insurance loss data set.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0