Copula-Based Time Series for Non-Gaussian and Non-Markovian Stationary Processes

Publication

Metrics

Paper Preview

Abstract

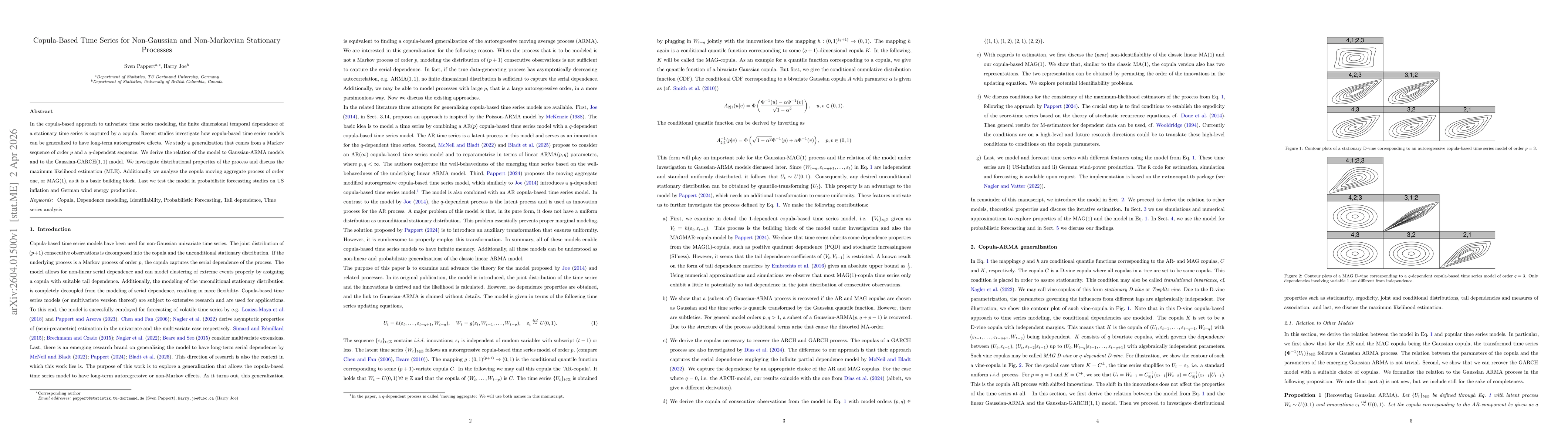

In the copula-based approach to univariate time series modeling, the finite dimensional temporal dependence of a stationary time series is captured by a copula. Recent studies investigate how copula-based time series models can be generalized to have long-term autoregressive effects. We study a generalization that comes from a Markov sequence of order p and a q-dependent sequence. We derive the relation of the model to Gaussian-ARMA models and to the Gaussian-GARCH(1,1) model. We investigate distributional properties of the process and discuss the maximum likelihood estimation (MLE). Additionally we analyze the copula moving aggregate process of order one, or MAG(1), as it is a basic building block. Last we test the model in probabilistic forecasting studies on US inflation and German wind energy production.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0