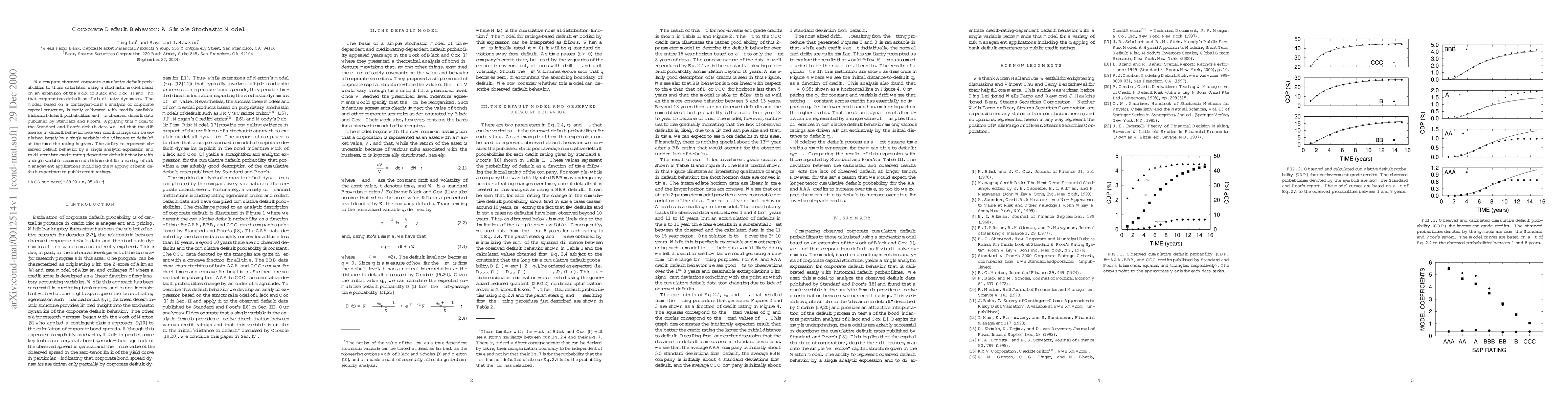

We compare observed corporate cumulative default probabilities to those

calculated using a stochastic model based on an extension of the work of Black

and Cox and find that corporations default as if via diffusive dynamics. The

model, based on a contingent-claims analysis of corporate capital structure, is

easily calibrated with readily available historical default probabilities and

fits observed default data published by Standard and Poor's. Applying this

model to the Standard and Poor's default data we find that the difference in

default behavior between credit ratings can be explained largely by a single

variable: the "distance to default" at the time the rating is given. The

ability to represent observed default behavior by a single analytic expression

and to differentiate credit-rating-dependent default behavior with a single

variable recommends this model for a variety of risk management applications

including the mapping of bank default experience to public credit ratings.

Discussion 0