Credit Risk Meets Random Matrices: Coping with Non-Stationary Asset Correlations

Publication

Metrics

AI Quick Summary

This paper reviews advancements in credit risk modeling for correlated assets, using random matrices to account for non-stationary asset correlations. The approach significantly reduces parameter dependence and highlights the prevalence of heavy tails in loss distribution, even with small correlations, calibrated with market data and demonstrated through numerical simulations.

Paper Preview

Abstract

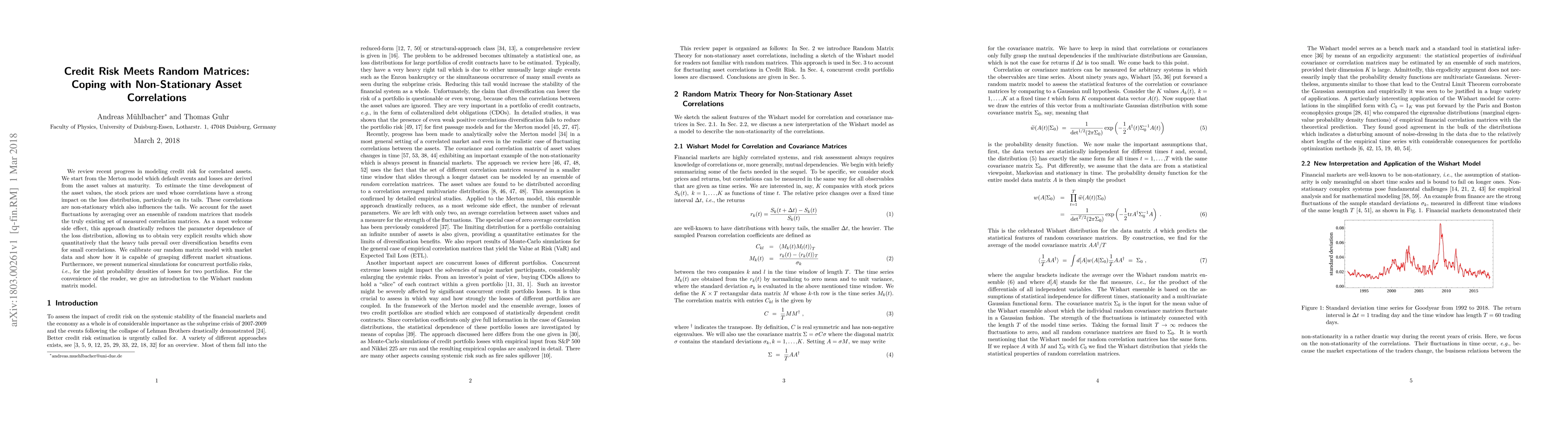

We review recent progress in modeling credit risk for correlated assets. We start from the Merton model which default events and losses are derived from the asset values at maturity. To estimate the time development of the asset values, the stock prices are used whose correlations have a strong impact on the loss distribution, particularly on its tails. These correlations are non-stationary which also influences the tails. We account for the asset fluctuations by averaging over an ensemble of random matrices that models the truly existing set of measured correlation matrices. As a most welcome side effect, this approach drastically reduces the parameter dependence of the loss distribution, allowing us to obtain very explicit results which show quantitatively that the heavy tails prevail over diversification benefits even for small correlations. We calibrate our random matrix model with market data and show how it is capable of grasping different market situations. Furthermore, we present numerical simulations for concurrent portfolio risks, i.e., for the joint probability densities of losses for two portfolios. For the convenience of the reader, we give an introduction to the Wishart random matrix model.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0