Publication

Metrics

AI Quick Summary

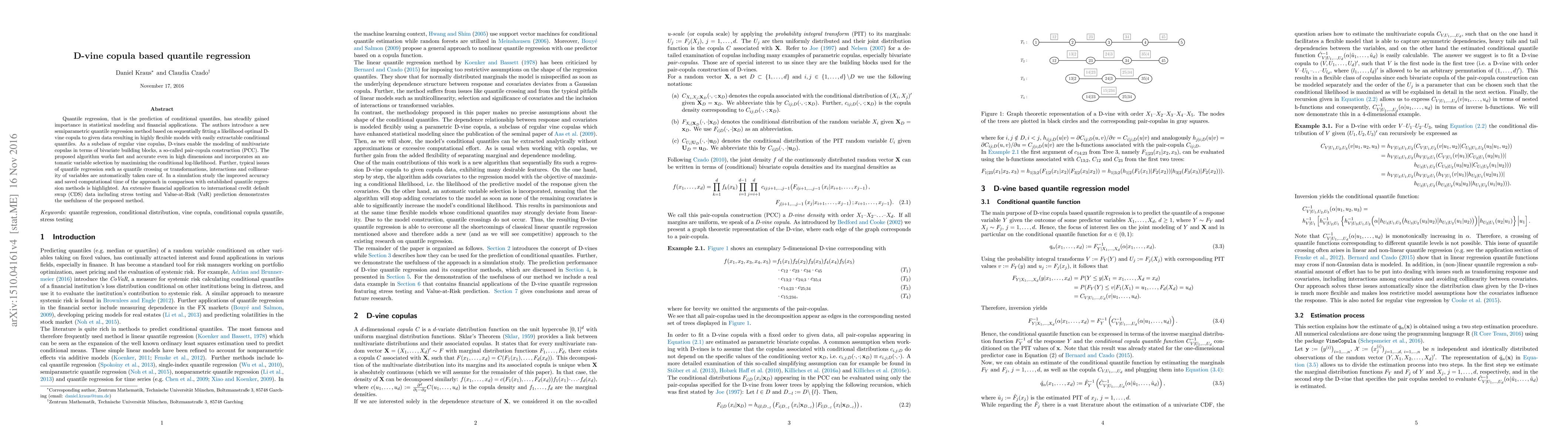

The paper proposes a new semiparametric quantile regression method using D-vine copulas for flexible, high-dimensional modeling, addressing issues like quantile crossing and collinearity. The method shows improved accuracy and computational efficiency in simulations and financial applications, such as predicting Value-at-Risk for international credit default swaps.

Paper Preview

Abstract

Quantile regression, that is the prediction of conditional quantiles, has steadily gained importance in statistical modeling and financial applications. The authors introduce a new semiparametric quantile regression method based on sequentially fitting a likelihood optimal D-vine copula to given data resulting in highly flexible models with easily extractable conditional quantiles. As a subclass of regular vine copulas, D-vines enable the modeling of multivariate copulas in terms of bivariate building blocks, a so-called pair-copula construction (PCC). The proposed algorithm works fast and accurate even in high dimensions and incorporates an automatic variable selection by maximizing the conditional log-likelihood. Further, typical issues of quantile regression such as quantile crossing or transformations, interactions and collinearity of variables are automatically taken care of. In a simulation study the improved accuracy and saved computational time of the approach in comparison with established quantile regression methods is highlighted. An extensive financial application to international credit default swap (CDS) data including stress testing and Value-at-Risk (VaR) prediction demonstrates the usefulness of the proposed method.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0