Publication

Metrics

AI Quick Summary

This paper examines overlooked data-generating processes for factors in return differences in time-series asset pricing, finding that traditional methods significantly underestimate market returns. It argues that Fama-French three-factor models may be misspecified and proposes using non-difference compound returns for a more accurate analysis.

Paper Preview

Abstract

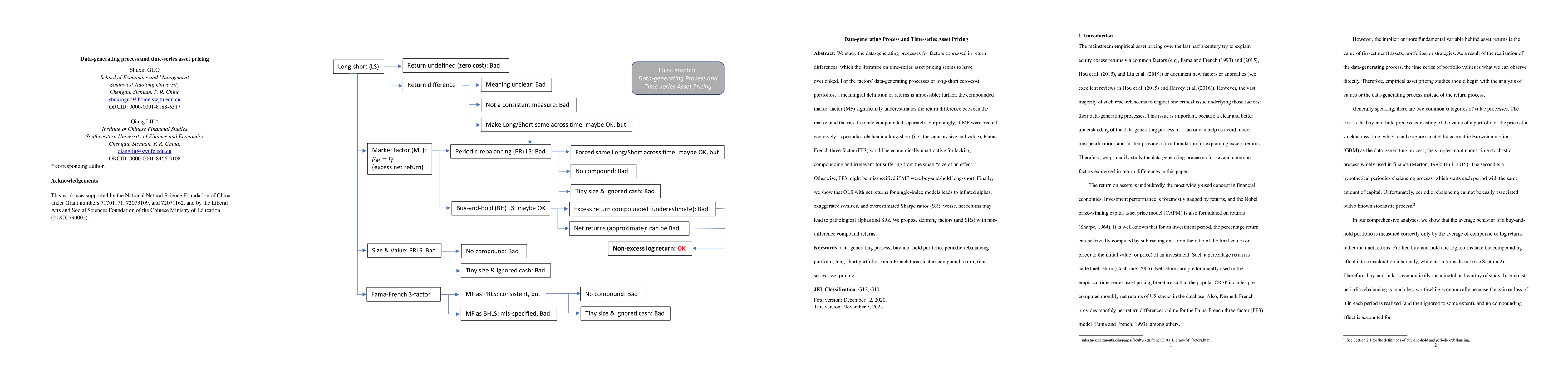

We study the data-generating processes for factors expressed in return differences, which the literature on time-series asset pricing seems to have overlooked. For the factors' data-generating processes or long-short zero-cost portfolios, a meaningful definition of returns is impossible; further, the compounded market factor (MF) significantly underestimates the return difference between the market and the risk-free rate compounded separately. Surprisingly, if MF were treated coercively as periodic-rebalancing long-short (i.e., the same as size and value), Fama-French three-factor (FF3) would be economically unattractive for lacking compounding and irrelevant for suffering from the small "size of an effect." Otherwise, FF3 might be misspecified if MF were buy-and-hold long-short. Finally, we show that OLS with net returns for single-index models leads to inflated alphas, exaggerated t-values, and overestimated Sharpe ratios (SR); worse, net returns may lead to pathological alphas and SRs. We propose defining factors (and SRs) with non-difference compound returns.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Paper Details

Authors

PDF Preview

Key Terms

Related Papers

No references found for this paper.

Discussion 0