Day-Ahead Electricity Price Forecasting Using Merit-Order Curves Time Series

Publication

Metrics

Paper Preview

Abstract

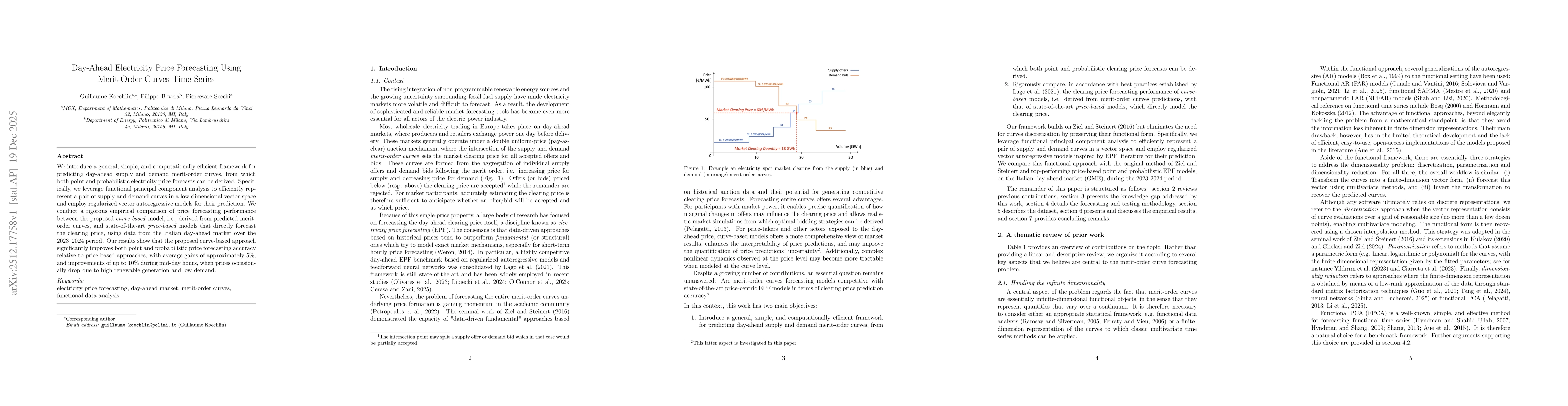

We introduce a general, simple, and computationally efficient framework for predicting day-ahead supply and demand merit-order curves, from which both point and probabilistic electricity price forecasts can be derived. Specifically, we leverage functional principal component analysis to efficiently represent a pair of supply and demand curves in a low-dimensional vector space and employ regularized vector autoregressive models for their prediction. We conduct a rigorous empirical comparison of price forecasting performance between the proposed curve-based model, i.e., derived from predicted merit-order curves, and state-of-the-art price-based models that directly forecast the clearing price, using data from the Italian day-ahead market over the 2023-2024 period. Our results show that the proposed curve-based approach significantly improves both point and probabilistic price forecasting accuracy relative to price-based approaches, with average gains of approximately 5%, and improvements of up to 10% during mid-day hours, when prices occasionally drop due to high renewable generation and low demand.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0