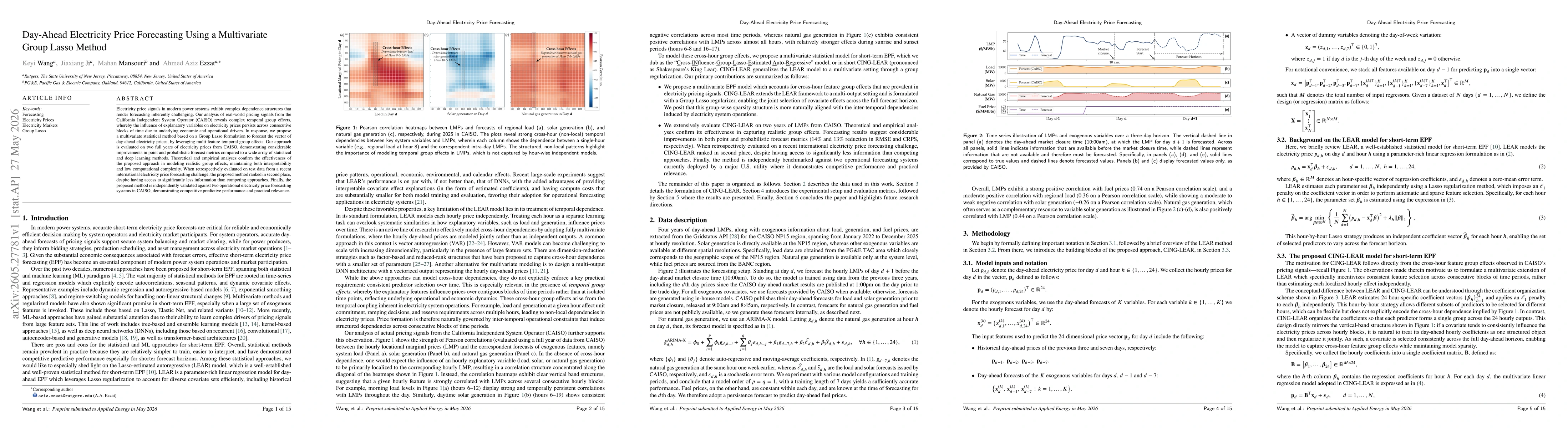

Electricity price signals in modern power systems exhibit complex dependence structures that render forecasting inherently challenging. Our analysis of real-world pricing signals from the California Independent System Operator (CAISO) reveals complex temporal group effects, whereby the influence of explanatory variables on electricity prices persists across consecutive blocks of time due to underlying economic and operational drivers. In response, we propose a multivariate statistical method based on a Group Lasso formulation to forecast the vector of day-ahead electricity prices, by leveraging multi-feature temporal group effects. Our approach is evaluated on two full years of electricity prices from CAISO, demonstrating considerable improvements in point and probabilistic forecast metrics compared to a wide array of statistical and deep learning methods. Theoretical and empirical analyses confirm the effectiveness of the proposed approach in modeling realistic group effects, maintaining both interpretability and low computational complexity. When retrospectively evaluated on test data from a recent international electricity price forecasting challenge, the proposed method ranked in second place, despite having access to significantly less information than competing approaches. Finally, the proposed method is independently validated against two operational electricity price forecasting systems in CAISO, demonstrating competitive predictive performance and practical relevance.

Discussion 0